Advertisement

- United States

- /

- Transportation

- /

- NYSE:UBER

Uber Technologies (UBER) Margin Compression Tests Bullish Valuation Narrative After FY 2025 Results

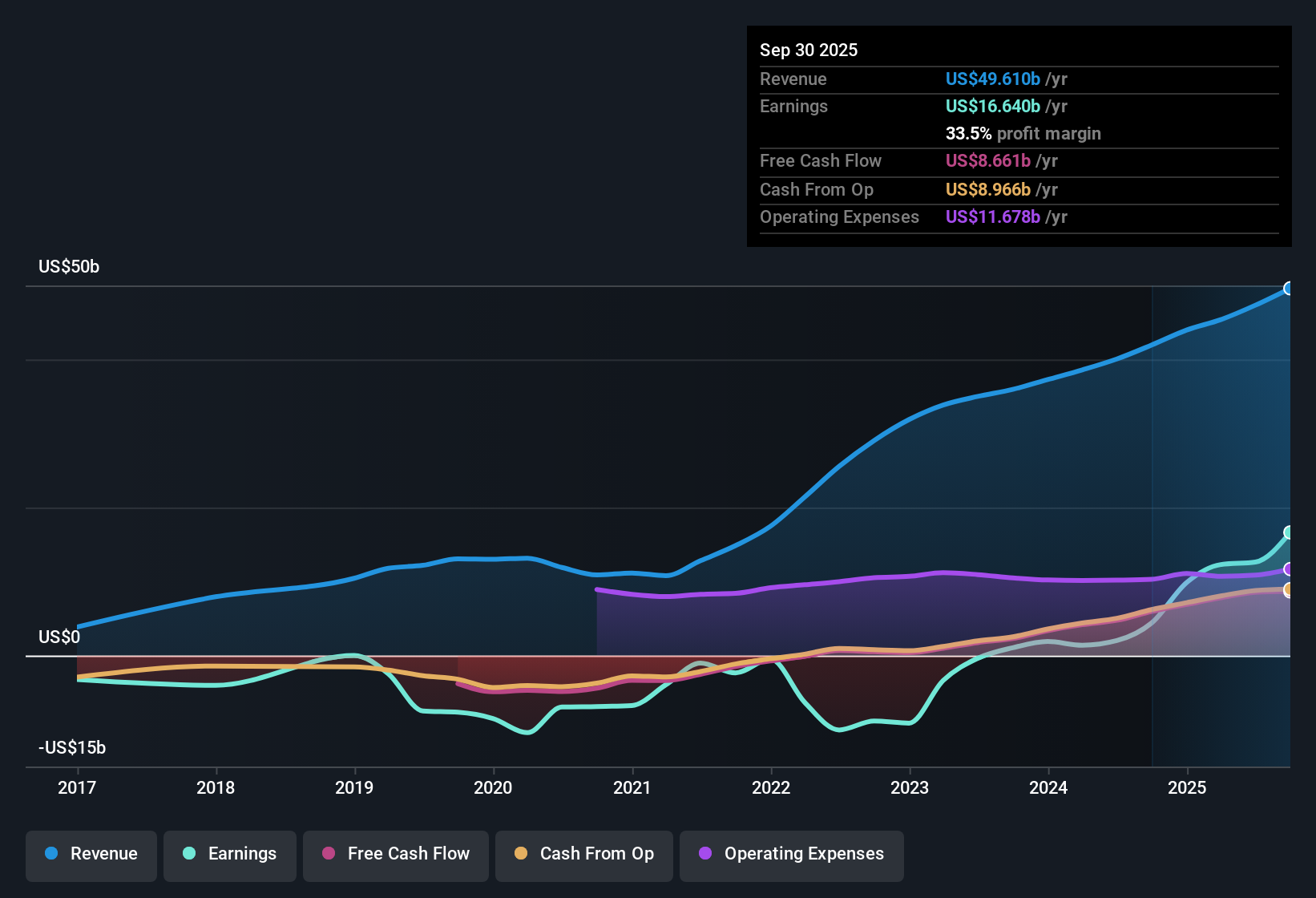

Uber Technologies (UBER) closed out FY 2025 with Q4 revenue of US$14.4b and basic EPS of US$0.14, alongside net income of US$296m, capping a year where trailing twelve month revenue reached US$52.0b and EPS came in at US$4.82. Over recent quarters, the company has seen revenue move from US$11.5b in Q1 2025 to US$13.5b in Q3 and then US$14.4b in Q4. Quarterly EPS shifted from US$0.85 in Q1 to US$3.18 in Q3 before landing at US$0.14 in the latest period, setting up a results season that puts the focus squarely on how sustainably Uber can defend its margins.

See our full analysis for Uber Technologies.With the latest numbers on the table, the next step is to see how they line up against the dominant stories around Uber's growth, profitability and risk profile that investors have been trading on over the past year.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Ease Back From 22.4% To 19.3%

- Over the last 12 months, Uber's net margin sat at 19.3%, compared with 22.4% in the prior year, alongside trailing revenue of US$52.0b and net income of US$10.1b.

- Bears often focus on profitability pressure, and the margin step down to 19.3% gives that concern a concrete data point, yet:

- Trailing earnings still grew 2% with net income of about US$10.1b, which shows profits remain positive even with lower margins.

- Quarterly net income in FY 2025 ranged from US$296m in Q4 to US$6.6b in Q3, underlining how results can swing while the full year still ends solidly profitable.

Revenue Forecast At 10.7% Versus Market 10.2%

- Revenue is forecast to grow about 10.7% per year, which is slightly above the 10.2% forecast for the broader US market, set against trailing 12 month revenue of around US$52.0b.

- Supporters of a bullish view point to these growth numbers, and the figures largely back that up but with some nuance:

- Earnings are forecast to grow at roughly 6.8% per year, which is below the 15.6% forecast for US market earnings, so revenue strength does not automatically translate into faster profit growth.

- Over the last year, earnings growth of 2% and the margin move from 22.4% to 19.3% show that profit expansion has been more modest than the multi year trend of 68.7% per year.

P/E Of 15.5x Versus 40.8x Industry

- At a share price of US$75.21, the stock trades on a P/E of 15.5x, compared with 40.8x for the US Transportation industry and 56.9x for peers, alongside a DCF fair value of about US$194.00 and an average analyst price target of US$106.32.

- What really stands out for bullish investors is how these valuation markers stack against the fundamentals:

- The gap between the US$75.21 share price and the DCF fair value of roughly US$194.00, plus the analyst target of US$106.32, aligns with the data showing a 41.4% implied upside from analysts.

- At the same time, margins easing to 19.3% and forecast earnings growth of 6.8% mean that any value case has to be weighed against slower profit expansion than the wider market forecast of 15.6% earnings growth.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Uber Technologies's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Uber's easing net margins and slower forecast earnings growth compared to the broader US market highlight that profit momentum is not keeping pace with revenue expectations.

If that gap between revenue strength and profit growth makes you cautious, check out our 81 resilient stocks with low risk scores to focus on companies where earnings quality and stability take center stage right away.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UBER

Uber Technologies

Develops and operates proprietary technology applications in the United States, Canada, Latin America, Europe, the Middle East, Africa, and the Asia Pacific.

Very undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0776.1% undervalued

211 followersusers have followed this narrative

1 commentusers have commented on this narrative

30 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.6% undervalued

53 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0719.6% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3814.1% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on INTLOOP ·

Renewed focus on business investment

Fair Value:JP¥4.17k56.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GO

GoranLagea on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d. future looks bright with a profit margin change of 38%

Fair Value:€36036.7% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Fibromat (M) Berhad ·

Fibromat: More than just a niche player, with clearer earnings visibility from order book and project wins

Fair Value:RM 1.0519.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.6% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

36 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.5% undervalued

1349 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0