Advertisement

- United States

- /

- Marine and Shipping

- /

- NYSE:MATX

Matson’s (MATX) Earnings Slide Raises Questions About Its Long-Term Growth Narrative

Simply Wall St

Reviewed by Sasha Jovanovic

- Matson, Inc. recently reported that despite a strong earnings gain, its three-year earnings per share have declined significantly and analysts now project further negative earnings growth.

- This has heightened investor caution, with ongoing concerns about Matson’s limited prospects for reversing its earnings trend amid challenging industry conditions.

- We’ll consider how concerns over Matson’s persistent earnings decline may alter the company’s long-term investment outlook and growth narrative.

Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

Matson Investment Narrative Recap

To be a shareholder in Matson right now, you need to believe in the company’s ability to capitalize on its protected Jones Act trade lanes and recover stable earnings despite external pressure on global shipping. The recent news around Chinese shipping companies waiving U.S. port surcharges does not materially affect the central short-term catalyst for Matson, which remains the potential for volume growth out of markets like Vietnam, but it may reinforce the risk of ongoing trade volatility and competitive pricing pressure in key routes.

Among recent company developments, the announcement of new Aloha Class vessel construction stands out, given Matson’s focus on fleet modernization and environmental compliance. While this commitment could enhance operational efficiency and support long-term margins, it comes with considerable capital expenditure requirements at a time when earnings are under pressure and cash flows face competing demands from buybacks and dividends.

However, with intensifying competition from global carriers and uncertainty around future container demand, investors should be aware that even well-defended routes can face unexpected headwinds if...

Read the full narrative on Matson (it's free!)

Matson's narrative projects $3.4 billion in revenue and $289.2 million in earnings by 2028. This requires a 0.3% annual revenue decline and a $204.9 million decrease in earnings from the current $494.1 million.

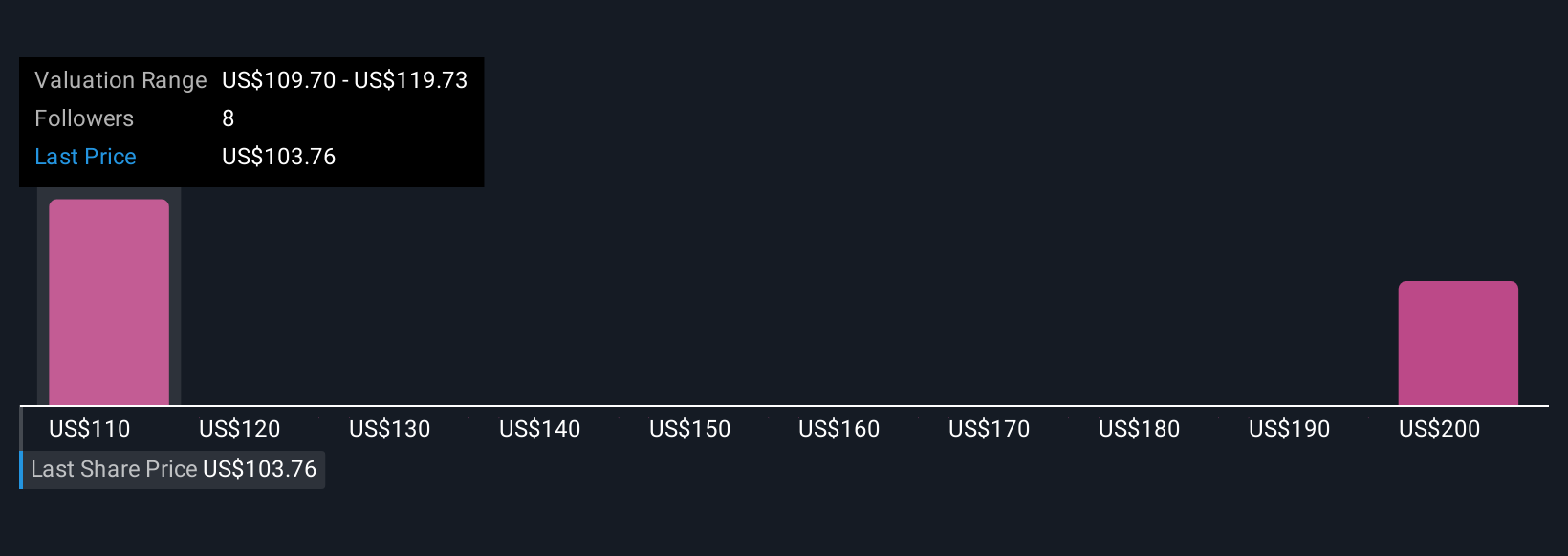

Uncover how Matson's forecasts yield a $110.00 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Seven members of the Simply Wall St Community provided Matson fair value estimates from US$92 to US$210 per share, capturing a broad spectrum of outlooks. As you review these varied views, keep in mind that analysts currently expect Matson’s earnings to trend downward, which may impact how quickly any perceived undervaluation can be realized.

Explore 7 other fair value estimates on Matson - why the stock might be worth just $92.00!

Build Your Own Matson Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Matson research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Matson research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Matson's overall financial health at a glance.

Looking For Alternative Opportunities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MATX

Matson

Engages in the provision of ocean transportation and logistics services.

Undervalued with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor