Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that HyreCar Inc. (NASDAQ:HYRE) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for HyreCar

What Is HyreCar's Net Debt?

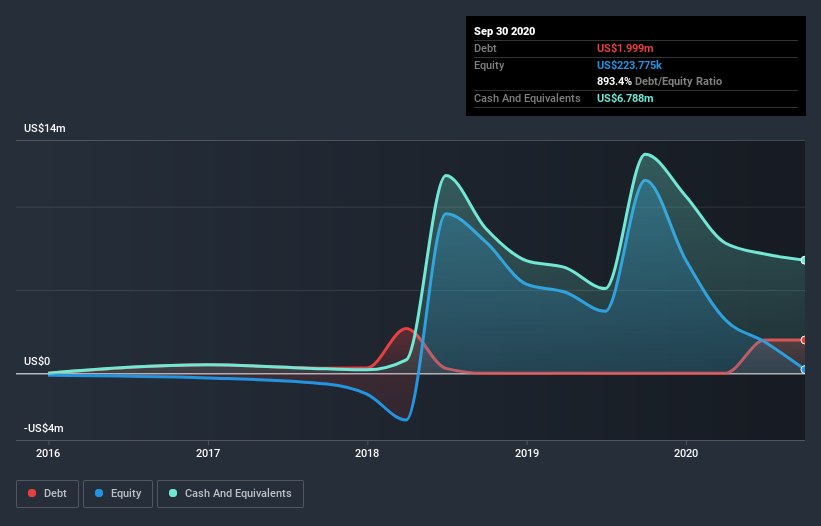

You can click the graphic below for the historical numbers, but it shows that as of September 2020 HyreCar had US$2.00m of debt, an increase on none, over one year. However, it does have US$6.79m in cash offsetting this, leading to net cash of US$4.79m.

How Strong Is HyreCar's Balance Sheet?

According to the last reported balance sheet, HyreCar had liabilities of US$7.24m due within 12 months, and liabilities of US$779.3k due beyond 12 months. On the other hand, it had cash of US$6.79m and US$72.5k worth of receivables due within a year. So its liabilities total US$1.16m more than the combination of its cash and short-term receivables.

This state of affairs indicates that HyreCar's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the US$140.2m company is short on cash, but still worth keeping an eye on the balance sheet. Despite its noteworthy liabilities, HyreCar boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine HyreCar's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, HyreCar reported revenue of US$23m, which is a gain of 63%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

So How Risky Is HyreCar?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months HyreCar lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$8.4m of cash and made a loss of US$15m. With only US$4.79m on the balance sheet, it would appear that its going to need to raise capital again soon. With very solid revenue growth in the last year, HyreCar may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that HyreCar is showing 4 warning signs in our investment analysis , and 1 of those can't be ignored...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading HyreCar or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if HyreCar might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OTCPK:HYRE.Q

HyreCar

HyreCar Inc. operates a car-sharing marketplace in the United States.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives