Advertisement

- United States

- /

- Transportation

- /

- NasdaqGS:CSX

How A US$40 Million Derailment Hit At CSX (CSX) Has Changed Its Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- CSX recently disclosed that its fourth-quarter earnings will be reduced by about US$40 million after an October coal train derailment and unrelated aluminum plant fires curtailed coal and automotive shipments, even as intermodal volumes held up.

- This setback highlights how concentrated exposure to bulk commodities can pressure results even when other parts of the rail network are performing well.

- We’ll now examine how the expected US$40 million earnings impact reshapes CSX’s investment narrative and risk-reward balance for investors.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

CSX Investment Narrative Recap

To own CSX, you need to believe in the long term value of its core Eastern U.S. rail network and its ability to translate volume stability into solid cash generation. The roughly US$40 million fourth quarter earnings hit from the derailment and fires looks material at the quarter level but does not, in itself, change the central near term catalyst of improving network efficiency or the key risk around exposure to volatile bulk commodities.

Against this setback, CSX’s role in the Alexandria Fourth Track Project stands out as directly linked to its efficiency and service quality catalyst. Adding capacity on a congested corridor that serves both freight and passengers can support more reliable operations over time, which matters if investors are focused on whether recent disruptions are one off events or symptoms of deeper operational constraints.

Yet, despite these positives, investors still need to be aware that CSX’s dependence on volatile coal markets...

Read the full narrative on CSX (it's free!)

CSX's narrative projects $15.7 billion revenue and $3.9 billion earnings by 2028. This requires 3.6% yearly revenue growth and about an $0.8 billion earnings increase from $3.1 billion today.

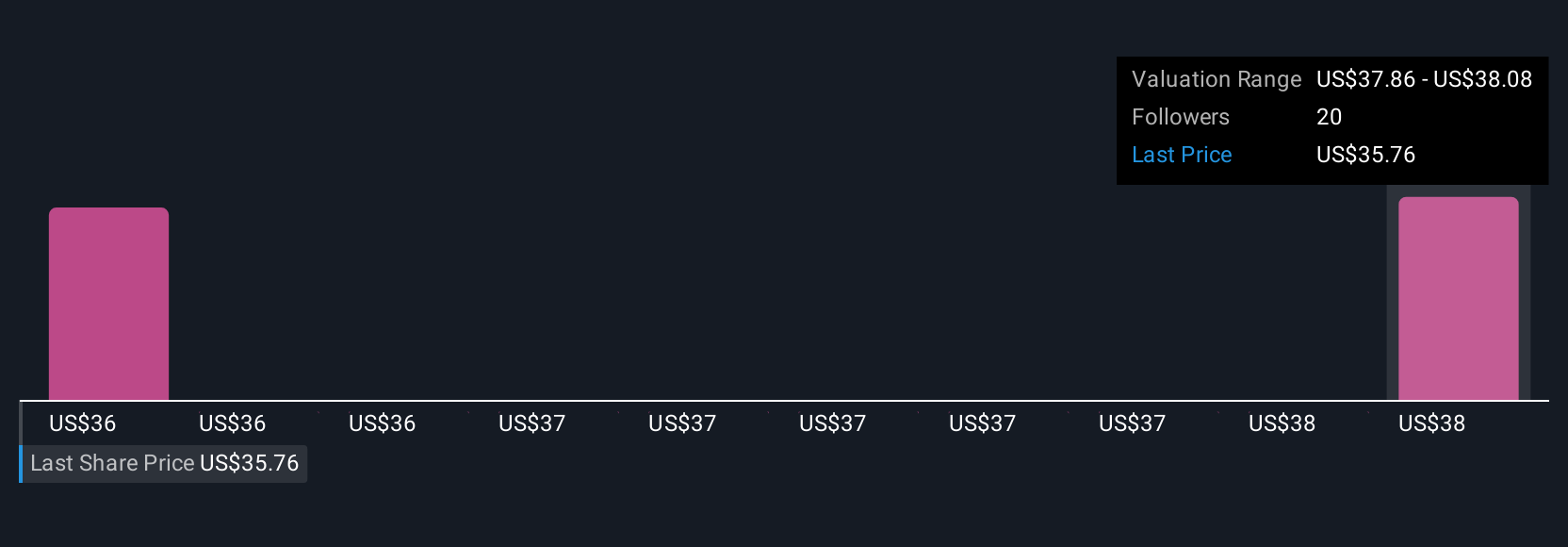

Uncover how CSX's forecasts yield a $39.29 fair value, a 9% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community span roughly US$36 to US$39 per share, underlining how differently individual investors can view the same cash flow outlook. Set against that, the recent derailment driven US$40 million earnings impact is a reminder that operational shocks tied to bulk commodities can quickly influence how you think about CSX’s near term performance and risk profile.

Explore 2 other fair value estimates on CSX - why the stock might be worth just $35.95!

Build Your Own CSX Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CSX research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free CSX research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CSX's overall financial health at a glance.

Looking For Alternative Opportunities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CSX

CSX

Provides rail-based freight transportation services in the United States and Canada.

Average dividend payer with limited growth.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.8% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.71.9% undervalued

1341 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative