Analysts Are Updating Their Teledyne Technologies Incorporated (NYSE:TDY) Estimates After Its First-Quarter Results

Teledyne Technologies Incorporated (NYSE:TDY) missed earnings with its latest quarterly results, disappointing overly-optimistic forecasters. Results look to have been somewhat negative - revenue fell 3.1% short of analyst estimates at US$1.4b, and statutory earnings of US$3.72 per share missed forecasts by 2.9%. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

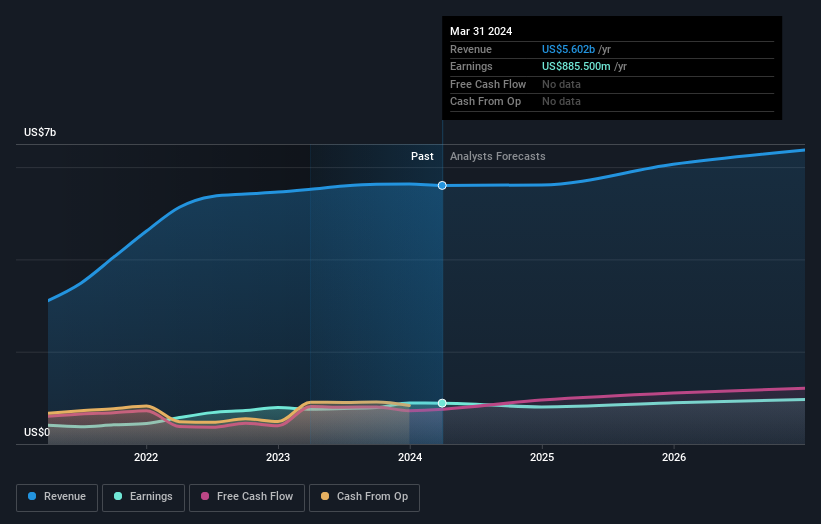

See our latest analysis for Teledyne Technologies

Taking into account the latest results, Teledyne Technologies' eight analysts currently expect revenues in 2024 to be US$5.61b, approximately in line with the last 12 months. Statutory earnings per share are forecast to sink 10% to US$16.74 in the same period. Before this earnings report, the analysts had been forecasting revenues of US$5.87b and earnings per share (EPS) of US$17.42 in 2024. The analysts are less bullish than they were before these results, given the reduced revenue forecasts and the minor downgrade to earnings per share expectations.

Despite the cuts to forecast earnings, there was no real change to the US$486 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Teledyne Technologies at US$510 per share, while the most bearish prices it at US$450. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that Teledyne Technologies' revenue growth is expected to slow, with the forecast 0.2% annualised growth rate until the end of 2024 being well below the historical 16% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 5.7% annually. Factoring in the forecast slowdown in growth, it seems obvious that Teledyne Technologies is also expected to grow slower than other industry participants.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Teledyne Technologies. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. The consensus price target held steady at US$486, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Teledyne Technologies. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for Teledyne Technologies going out to 2026, and you can see them free on our platform here..

It might also be worth considering whether Teledyne Technologies' debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Teledyne Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:TDY

Teledyne Technologies

Provides enabling technologies for industrial growth markets in the United States, Europe, Asia, and internationally.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)