You Might Like Methode Electronics, Inc. (NYSE:MEI) But Do You Like Its Debt?

While small-cap stocks, such as Methode Electronics, Inc. (NYSE:MEI) with its market cap of US$1.1b, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Understanding the company's financial health becomes crucial, as mismanagement of capital can lead to bankruptcies, which occur at a higher rate for small-caps. Let's work through some financial health checks you may wish to consider if you're interested in this stock. Nevertheless, this is just a partial view of the stock, and I recommend you dig deeper yourself into MEI here.

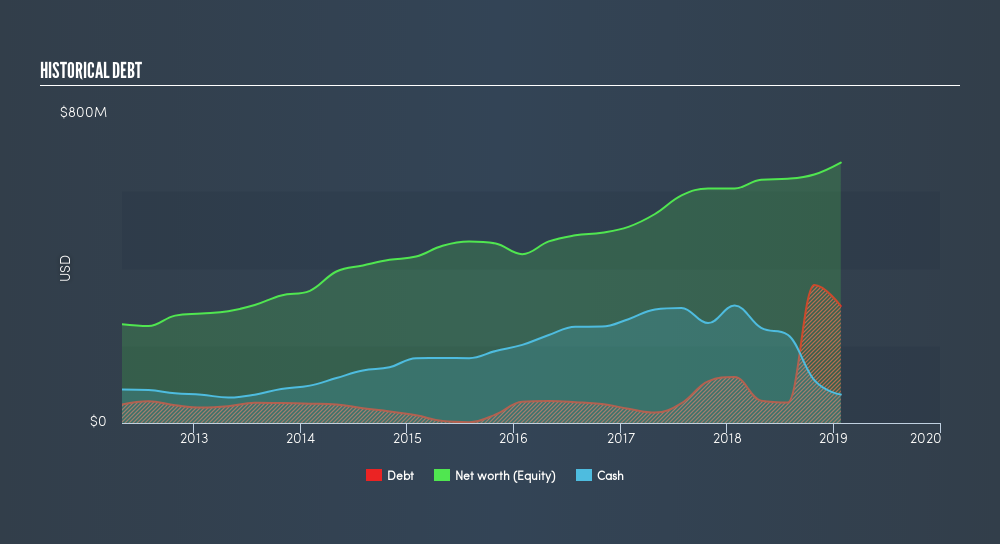

Does MEI Produce Much Cash Relative To Its Debt?

MEI has built up its total debt levels in the last twelve months, from US$119m to US$303m – this includes long-term debt. With this increase in debt, MEI currently has US$74m remaining in cash and short-term investments , ready to be used for running the business. On top of this, MEI has produced US$95m in operating cash flow in the last twelve months, resulting in an operating cash to total debt ratio of 31%, signalling that MEI’s operating cash is sufficient to cover its debt.

Does MEI’s liquid assets cover its short-term commitments?

With current liabilities at US$176m, it appears that the company has been able to meet these obligations given the level of current assets of US$446m, with a current ratio of 2.53x. The current ratio is the number you get when you divide current assets by current liabilities. Generally, for Electronic companies, this is a reasonable ratio since there's a sufficient cash cushion without leaving too much capital idle or in low-earning investments.

Is MEI’s debt level acceptable?

MEI is a relatively highly levered company with a debt-to-equity of 45%. This is a bit unusual for a small-cap stock, since they generally have a harder time borrowing than large more established companies. No matter how high the company’s debt, if it can easily cover the interest payments, it’s considered to be efficient with its use of excess leverage. A company generating earnings before interest and tax (EBIT) at least three times its net interest payments is considered financially sound. In MEI's case, the ratio of 21.84x suggests that interest is comfortably covered, which means that debtors may be willing to loan the company more money, giving MEI ample headroom to grow its debt facilities.

Next Steps:

Although MEI’s debt level is towards the higher end of the spectrum, its cash flow coverage seems adequate to meet obligations which means its debt is being efficiently utilised. This may mean this is an optimal capital structure for the business, given that it is also meeting its short-term commitment. This is only a rough assessment of financial health, and I'm sure MEI has company-specific issues impacting its capital structure decisions. I recommend you continue to research Methode Electronics to get a more holistic view of the small-cap by looking at:

- Future Outlook: What are well-informed industry analysts predicting for MEI’s future growth? Take a look at our free research report of analyst consensus for MEI’s outlook.

- Valuation: What is MEI worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether MEI is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:MEI

Methode Electronics

Designs, engineers, produces, and sells mechatronic products internationally.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)