- United States

- /

- Tech Hardware

- /

- NYSE:IONQ

Analysts Have Been Trimming Their IonQ, Inc. (NYSE:IONQ) Price Target After Its Latest Report

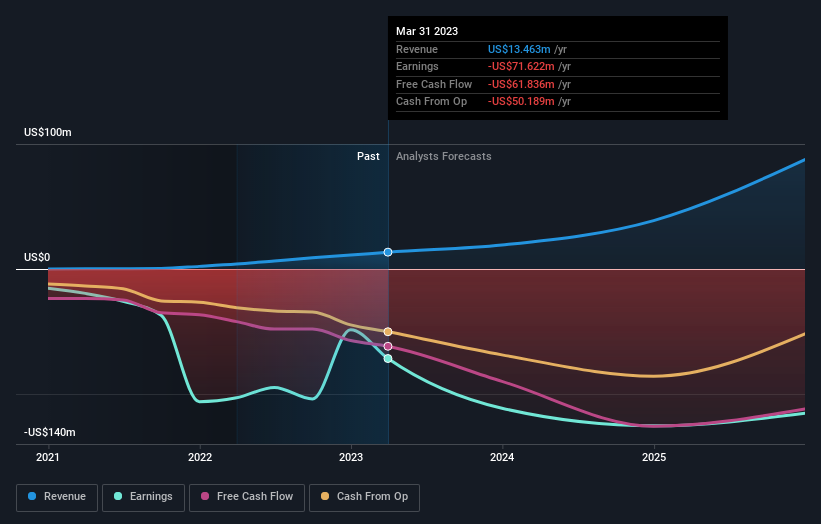

Investors in IonQ, Inc. (NYSE:IONQ) had a good week, as its shares rose 7.6% to close at US$6.35 following the release of its quarterly results. IonQ beat revenue forecasts by a solid 13%, hitting US$4.3m. Statutory losses also blew out, with the loss per share reaching US$0.14, some 31% bigger than the analysts expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Check out our latest analysis for IonQ

Taking into account the latest results, the current consensus from IonQ's five analysts is for revenues of US$19.2m in 2023, which would reflect a sizeable 42% increase on its sales over the past 12 months. Losses are forecast to balloon 45% to US$0.52 per share. Yet prior to the latest earnings, the analysts had been forecasting revenues of US$18.6m and losses of US$0.48 per share in 2023. So it's pretty clear consensus is mixed on IonQ after the new consensus numbers; while the analysts lifted revenue numbers, they also administered a moderate increase in per-share loss expectations.

Spiting the revenue upgrading, the average price target fell 20% to US$8.40, clearly signalling that higher forecast losses are a valuation concern. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values IonQ at US$9.00 per share, while the most bearish prices it at US$7.00. This is a very narrow spread of estimates, implying either that IonQ is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that IonQ's revenue growth is expected to slow, with the forecast 60% annualised growth rate until the end of 2023 being well below the historical 243% growth over the last year. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 6.5% per year. So it's pretty clear that, while IonQ's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

With that in mind, we wouldn't be too quick to come to a conclusion on IonQ. Long-term earnings power is much more important than next year's profits. We have forecasts for IonQ going out to 2025, and you can see them free on our platform here.

Even so, be aware that IonQ is showing 2 warning signs in our investment analysis , you should know about...

If you're looking to trade IonQ, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:IONQ

Excellent balance sheet with limited growth.