Advertisement

Arlo Technologies (ARLO): Evaluating Current Valuation Following Recent Share Price Pullback

Arlo Technologies (ARLO) continues to draw attention as investors take stock of its recent performance and long-term growth trajectory. With shares up 35% year to date and annual net income showing strong momentum, the company’s valuation sparks ongoing debate.

See our latest analysis for Arlo Technologies.

After a red-hot run earlier this year, Arlo Technologies’ share price has pulled back sharply in recent sessions, dropping more than 23% over the past week. Even so, the overall momentum story remains impressive, as the stock is still up 35% year to date and boasts a 285% total shareholder return over the past three years. This underscores investors’ confidence in its long-term growth prospects.

If you’re keeping an eye on dynamic tech movers like Arlo, it’s a great moment to broaden your search and discover fast growing stocks with high insider ownership

The real question for investors is whether Arlo Technologies’ recent pullback represents an attractive entry point or if the current price already reflects all of its anticipated growth. Could there be more upside from here, or is the opportunity priced in?

Most Popular Narrative: 36.1% Undervalued

With Arlo Technologies trading well below the narrative’s calculated fair value, the current price leaves plenty of room for future optimism compared to analyst projections. The gap between today’s valuation and the narrative estimate sets the stage for bold growth assumptions.

Continual migration of subscribers to higher-priced AI-driven service tiers (Arlo Secure 6), alongside the corresponding increase in ARPU (now over $15, up 26% y/y), reinforces the long-term shift to recurring, high-margin (85% non-GAAP service margin) subscription revenue. This supports expanding net margins and greater earnings visibility.

What hidden ingredient drives such a bullish fair value? The narrative is betting on breakout growth in earnings and a profit margin uplift more typical of industry giants. Curious which future milestones power this forecast? See the narrative’s full financial math before the market catches on.

Result: Fair Value of $23.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, intensifying competition and persistent international weakness could quickly change Arlo’s outlook and challenge the narrative's optimistic projections.

Find out about the key risks to this Arlo Technologies narrative.

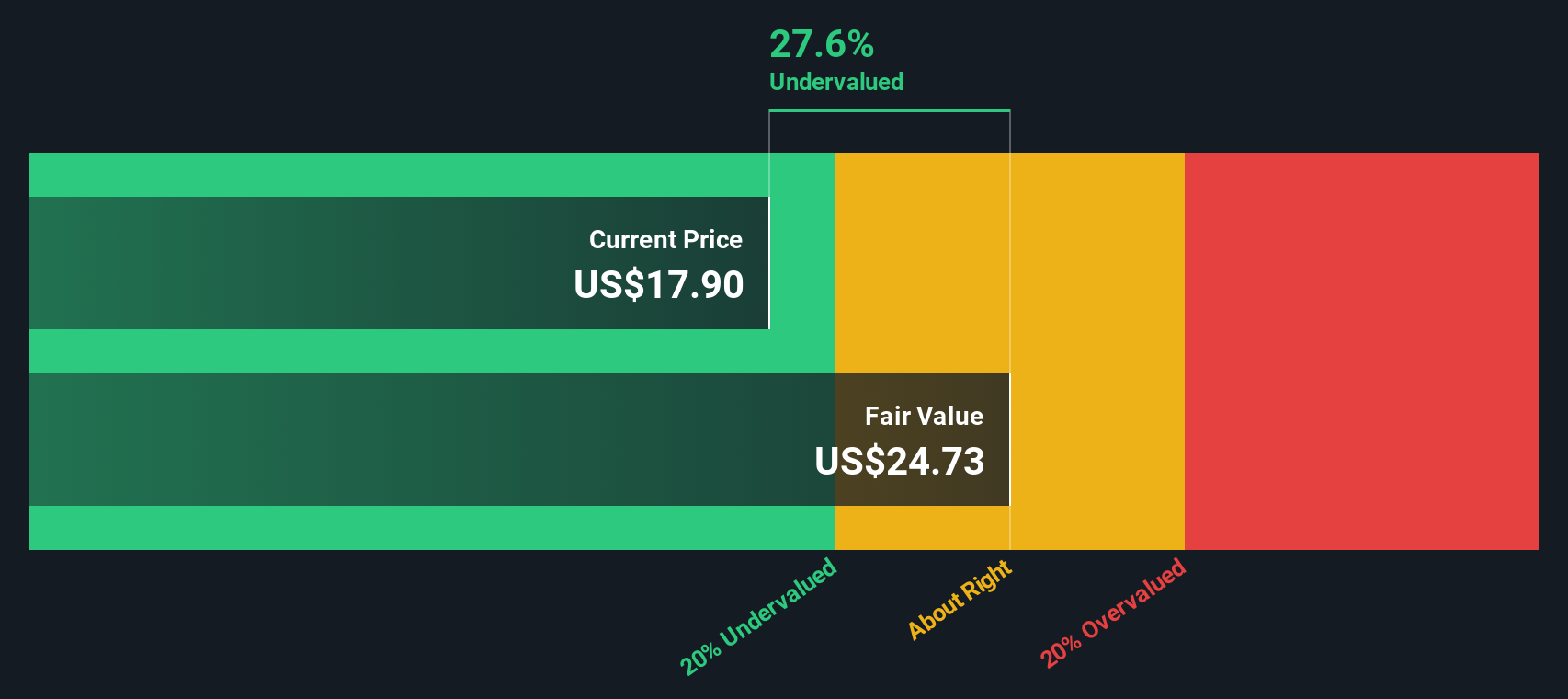

Another View: What Does the SWS DCF Model Say?

While the narrative and analyst consensus see Arlo Technologies as significantly undervalued, the SWS DCF model tells a more cautious story. Our DCF analysis estimates the current price is about 11% below fair value, which hints at a potential bargain but suggests much less upside than some expect. Could this grounded approach point to a lower margin for error, or is the market underestimating future gains?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Arlo Technologies Narrative

If you want a hands-on approach or see things differently, dive into the data and shape your own perspective in just a few minutes with Do it your way.

A great starting point for your Arlo Technologies research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

If you want an edge, steer your portfolio towards the biggest opportunities on Simply Wall Street. Miss out on these now and you could regret it later.

- Capitalize on the momentum of rapid technological change by exploring these 25 AI penny stocks, which are setting the pace in artificial intelligence advancements.

- Capture value the market is missing by checking out these 877 undervalued stocks based on cash flows, where strong cash flows could indicate overlooked upside for savvy investors.

- Get in early on tomorrow’s stars and increase your upside with these 3589 penny stocks with strong financials known for big potential and strong financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ARLO

Arlo Technologies

Provides cloud-based platform services in the Americas, Europe, the Middle East, Africa, and the Asia Pacific regions.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

89 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

JO

Joe222 on Encore Capital Group ·

ECPG is a solid company

Fair Value:US$120.3833.4% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Aftermath Silver ·

Aftermath Silver, A 35% Insider-Aligned Silver Stock With a Giant Critical Metals Twist

Fair Value:CA$30.3797.5% undervalued

5 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

RockeTeller on Selkirk Copper Mines ·

Selkirk Copper, Ex-Teck + 87% Hit Rate Maybe The Highest-Conviction Copper Restart in Canada Now

Fair Value:CA$21.7491.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

115 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1193 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

31 likesusers have liked this narrative