- United States

- /

- Tech Hardware

- /

- NasdaqGS:WDC

Western Digital (WDC): Evaluating Valuation After Bullish Analyst Calls and Earnings Beat Driven by AI Demand

Reviewed by Simply Wall St

When Western Digital (WDC) dropped its latest earnings report, the market sat up and took notice. The company not only beat Wall Street’s expectations but also issued a growth outlook that topped consensus estimates. This sent a clear signal that AI and cloud infrastructure demand is seriously moving the needle. Investors were quick to react as major analysts like Morgan Stanley weighed in with positive endorsements, including a ‘Top Pick’ label, building momentum in the days that followed. All of this has put Western Digital at the center of fresh conversations around technology leadership and future earnings power, even as some voices continue to flag risks tied to customer concentration and evolving storage technology.

These developments feed into an already strong run for Western Digital this year. Over the past month alone, the stock surged nearly 24%, and it’s up 98% in the past year. That puts it ahead of many peers in the tech hardware space at a time when companies linked to AI demand are regularly making headlines. On top of solid financial performance, Western Digital’s strategic partnerships and focus on debt reduction have helped strengthen its recovery. Market perception has grown increasingly optimistic in the wake of these results. Still, questions about valuation keep surfacing, with some suggesting that a lot of the good news may already be priced in.

After such a fast climb and a series of bullish signals, some are considering whether there is still room to buy Western Digital at a bargain, or if the market is a step ahead in pricing future growth.

Most Popular Narrative: 4.7% Overvalued

The most widely followed narrative suggests Western Digital is slightly overvalued based on projected future growth and profitability, measured against a calculated fair value.

"Higher adoption of Western Digital's larger capacity, high-value ePMR and UltraSMR drives, with rapid qualification and ramp cycles, demonstrates customer trust and enables both pricing power and favorable product mix. This leads to structurally higher gross margins and improved net margins over time."

Curious about what’s fueling this ambitious price outlook? The answer lies in bold growth assumptions, aggressive margin targets, and future market share plays. If you want to know what profit trajectory is being used to set this valuation, discover which surprising metrics analysts are betting on. There may be numbers behind this narrative that could shock even seasoned tech investors.

Result: Fair Value of $89.14 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, heavy reliance on a handful of large cloud customers and ongoing trade uncertainty could quickly change Western Digital’s growth trajectory.

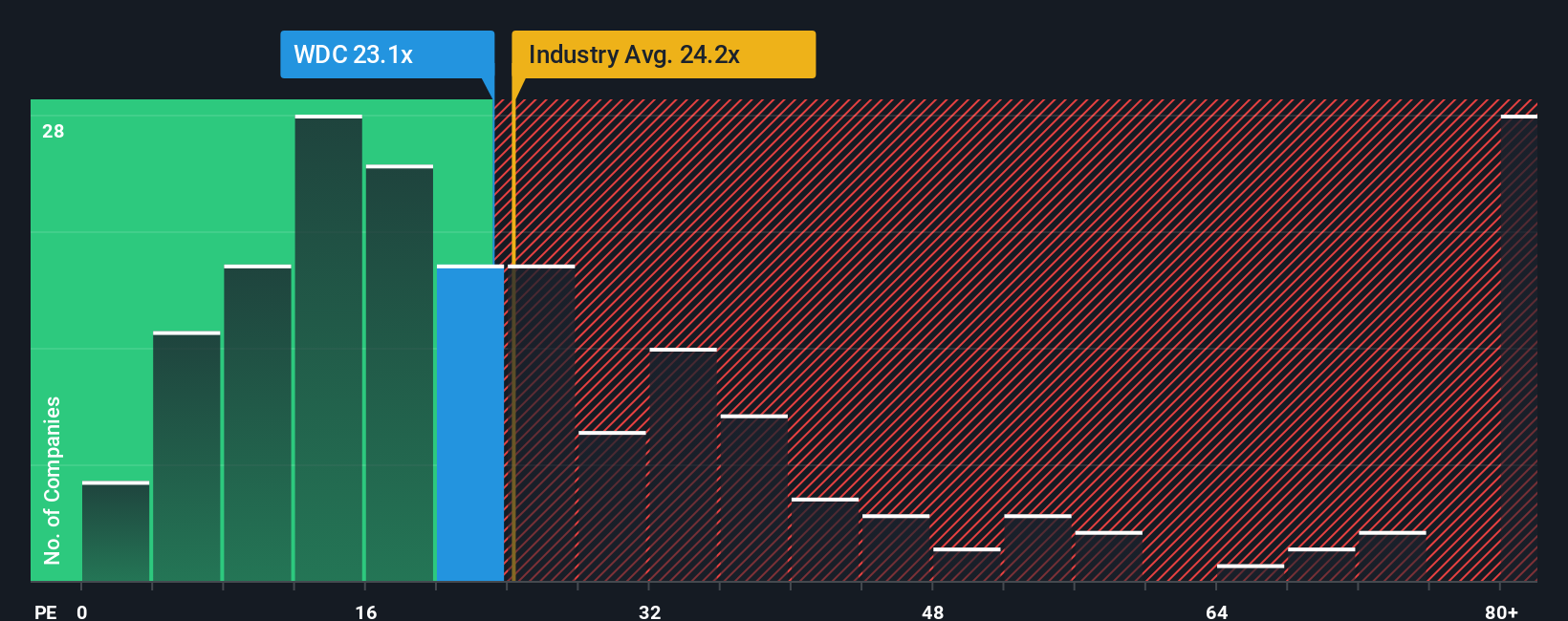

Find out about the key risks to this Western Digital narrative.Another View: What Do Standard Valuation Metrics Say?

While some analysts focus on detailed future projections, a straightforward comparison to the broader tech industry tells a different story. By this common method, Western Digital’s shares are actually trading at a lower valuation. Could this suggest the market is underestimating Western Digital, or is there a catch hidden in the details?

See what the numbers say about this price — find out in our valuation breakdown.

Stay updated when valuation signals shift by adding Western Digital to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Western Digital Narrative

If you see the story differently, or want to dig into the numbers yourself, it takes just a few minutes to craft your own take. Do it your way.

A great starting point for your Western Digital research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

If you want to spot the next big move before others catch on, use the Simply Wall Street Screener to uncover unique opportunities that match your investment style. Don’t let great potential slip away. Powerful screeners could be what sets your portfolio apart.

- Tap into the rising wave of artificial intelligence by targeting next-generation leaders through our curated list of AI penny stocks.

- Seize the chance for stable long-term growth with stocks offering exceptional yields, handpicked in the dividend stocks with yields > 3% selection.

- Get ahead of the curve by seeking out tomorrow’s industry disruptors with ultra-low market valuations found in our undervalued stocks based on cash flows tool.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Western Digital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:WDC

Western Digital

Develops, manufactures, and sells data storage devices and solutions based on hard disk drive (HDD) technology in the United States, Asia, Europe, the Middle East, and Africa.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)