- United States

- /

- Communications

- /

- NasdaqGS:VSAT

Viasat (VSAT) Valuation in Focus Following Defense Wins, Space Force Contracts, and ViaSat-3 F2 Launch Momentum

Reviewed by Simply Wall St

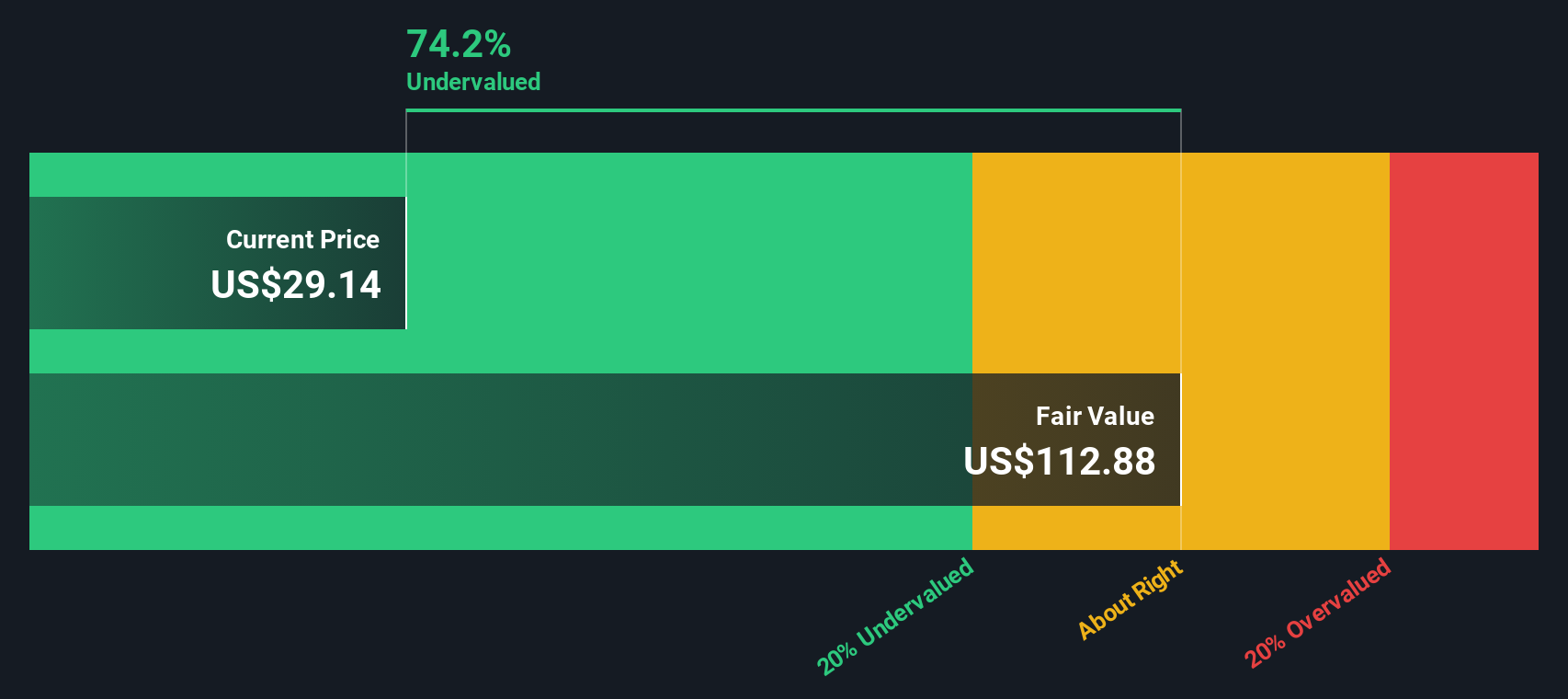

Most Popular Narrative: 24% Overvalued

The most popular narrative in the market today suggests that Viasat is trading above its fair value estimate, with a consensus view projecting the stock to be nearly a quarter overvalued compared to underlying earnings growth assumptions.

Expanding secure connectivity and advanced satellite networks positions Viasat for broader market access, higher pricing power, and sustained top-line growth. Strategic integration, operational efficiency, and heightened demand for digital inclusion support improved cash flow, reduced debt, and better earnings quality.

What is behind this attention-grabbing fair value? Analysts are betting on a game-changing financial turnaround, driven by a set of bold forecasts that could put Viasat in a new league. But which future numbers hold the key to justifying this target, and could this scenario reshape how investors value the stock for years to come? The answers may change your view of what is possible for Viasat’s growth story.

Result: Fair Value of $24.29 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, ongoing heavy capital expenditures and declining U.S. broadband subscribers could quickly derail the expected growth path that supports the bullish outlook.

Find out about the key risks to this Viasat narrative.Another View: Discounted Cash Flow Perspective

Looking from a different angle, our DCF model paints a sharply different picture for Viasat. This analysis suggests the shares may actually be undervalued. Does this new calculation upend the prevailing market narrative, or does it simply add another wrinkle?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Viasat Narrative

If you see things differently or want to dig into the numbers on your own, you can build your own view of Viasat’s story in under three minutes with our tools. Do it your way.

A great starting point for your Viasat research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Act now to build a smarter portfolio and spot tomorrow’s winners before everyone else. With Simply Wall Street’s screeners, you can uncover fresh opportunities tailored to your goals.

- Unlock fast-growing potential by targeting penny stocks with robust financials and momentum using our penny stocks with strong financials.

- Capture strong income streams by uncovering companies offering dividend yields higher than 3 percent through our exclusive dividend stocks with yields > 3%.

- Harness breakthrough innovation by pinpointing healthcare companies leading the AI transformation with the powerful healthcare AI stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:VSAT

Viasat

Provides broadband and communications products and services in the United States and internationally.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)