Advertisement

- United States

- /

- Communications

- /

- OTCPK:VISL

Vislink Technologies, Inc. (NASDAQ:VISL) Just Reported Earnings, And Analysts Cut Their Target Price

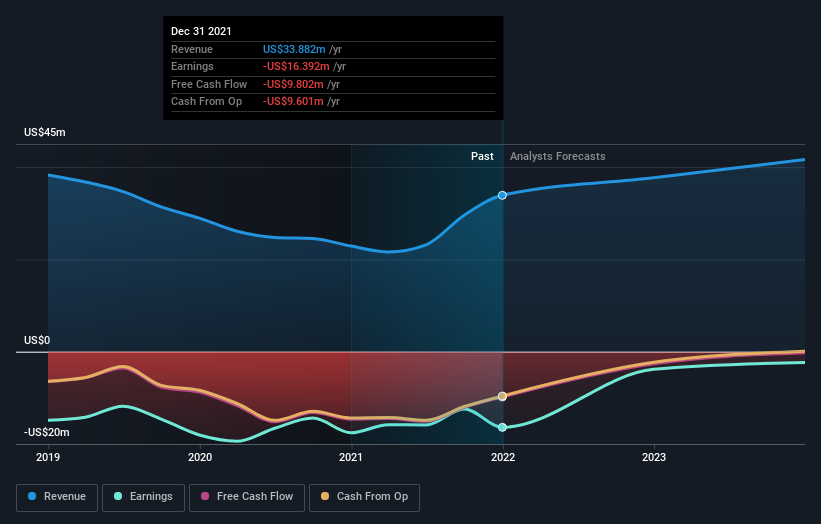

Shareholders might have noticed that Vislink Technologies, Inc. (NASDAQ:VISL) filed its annual result this time last week. The early response was not positive, with shares down 2.7% to US$1.08 in the past week. The results don't look great, especially considering that statutory losses grew 322% toUS$0.38 per share. Revenues of US$34m did beat expectations by 4.3%, but it looks like a bit of a cold comfort. The analyst typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We've gathered the most recent statutory forecasts to see whether the analyst has changed their earnings models, following these results.

See our latest analysis for Vislink Technologies

Taking into account the latest results, the most recent consensus for Vislink Technologies from lone analyst is for revenues of US$37.7m in 2022 which, if met, would be a notable 11% increase on its sales over the past 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 78% to US$0.08. Before this latest report, the consensus had been expecting revenues of US$36.3m and US$0.05 per share in losses. So it's pretty clear the analyst has mixed opinions on Vislink Technologies even after this update; although they upped their revenue numbers, it came at the cost of a very substantial increase in per-share losses.

It will come as no surprise that expanding losses caused the consensus price target to fall 99% to US$2.00with the analyst implicitly ranking ongoing losses as a greater concern than growing revenues.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. One thing stands out from these estimates, which is that Vislink Technologies is forecast to grow faster in the future than it has in the past, with revenues expected to display 11% annualised growth until the end of 2022. If achieved, this would be a much better result than the 2.4% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 6.9% per year. So it looks like Vislink Technologies is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at Vislink Technologies. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. Furthermore, the analyst also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have analyst estimates for Vislink Technologies going out as far as 2023, and you can see them free on our platform here.

You should always think about risks though. Case in point, we've spotted 2 warning signs for Vislink Technologies you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:VISL

Vislink Technologies

Provides solutions for collecting live news, sports, entertainment, and news events for the broadcast, surveillance, and defense markets in North America, South America, Europe, Asia, and internationally.

Adequate balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7060.2% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.226.4% undervalued

35 followersusers have followed this narrative

7 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0542.8% undervalued

37 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15123.9% undervalued

86 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Guanajuato Silver ·

Guanajuanto Silver, Hidden Gem of 1.8M Oz Producer + 75,000m Drilling = Huge Upside

Fair Value:CA$9.8495.2% undervalued

13 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.1621.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WI

Wizkhalifa on PSP Energy Berhad ·

PSP Energy Breaks Key Downtrend, Momentum Building for Further Upside

Fair Value:RM 0.09257.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9724.0% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1935.7% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0