Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:TTMI

Assessing TTM Technologies (TTMI) Valuation After Analyst Upgrades Highlight AI And Malaysia Growth Potential

What triggered the sharp move in TTM Technologies (TTMI)?

TTM Technologies (TTMI) drew fresh attention after its share price reacted strongly to upbeat analyst commentary. The commentary highlighted the company’s ties to AI demand, its Malaysian production ramp up, and recent earnings and revenue momentum versus sector peers.

See our latest analysis for TTM Technologies.

Those bullish analyst calls came on top of already strong momentum, with a 40.9% 30 day share price return and a 71% 90 day share price return. The 1 year total shareholder return is very large, suggesting that enthusiasm around AI and defense exposure has been building rather than fading.

If TTM Technologies’ surge has you thinking about what else is moving in tech, it could be a good moment to scan high growth tech and AI stocks for other AI linked opportunities.

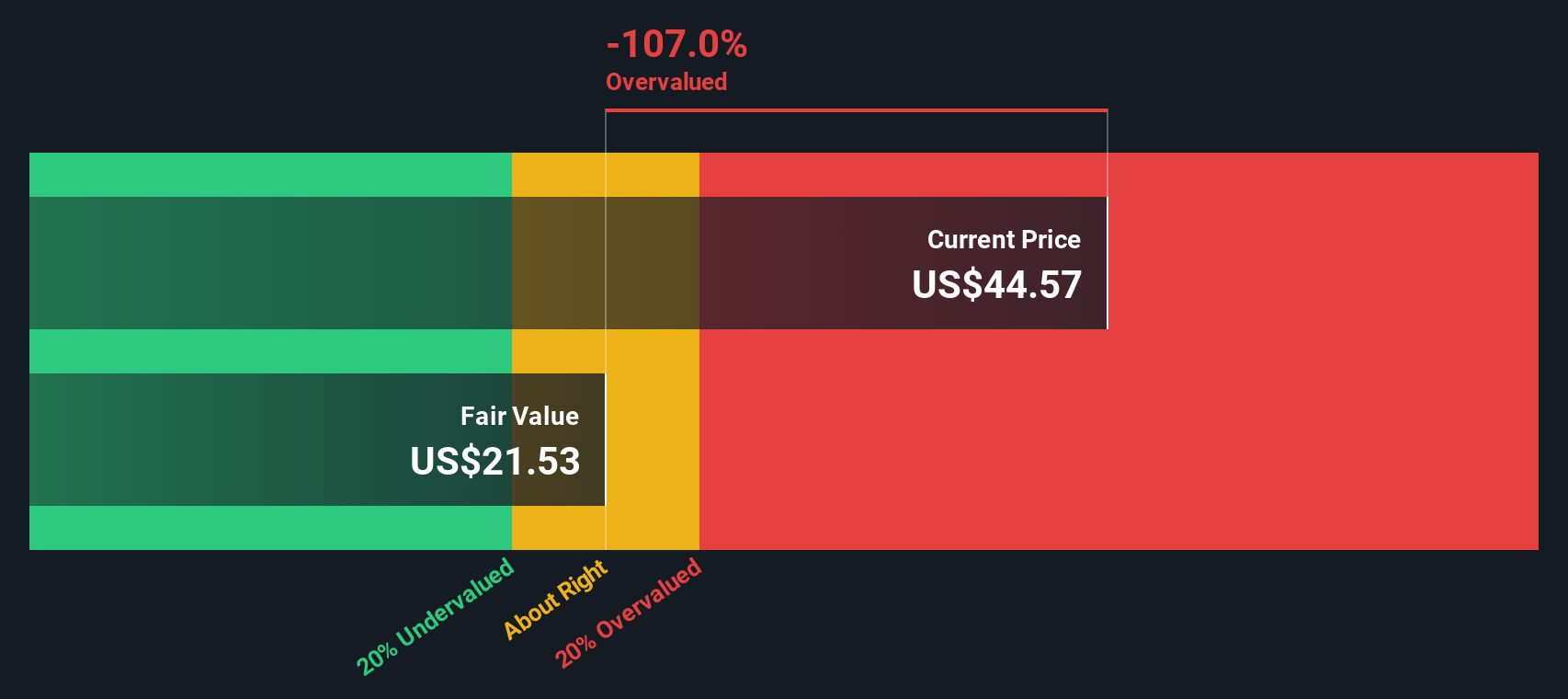

With TTMI now trading around US$99.87 after a very strong run and sitting above an average analyst price target of US$92.75, the key question is whether any upside remains or if the market already reflects expectations for future growth.

Price-to-Earnings of 78.2x: Is it justified?

TTM Technologies currently trades on a P/E of 78.2x, which is well above both peer and industry benchmarks, even after the recent share price jump.

The P/E ratio compares the share price to earnings per share, so a higher multiple usually reflects higher expectations for future profit growth. For a company like TTM Technologies, with exposure to aerospace, defense and AI linked electronics, a rich multiple suggests the market is willing to pay up for that earnings profile.

Here, the premium is sizable. The current 78.2x P/E is far above the US Electronic industry average of 28.1x and also well ahead of the peer average of 36.6x. It also sits meaningfully above an estimated fair P/E of 44.2x, a level the market could move toward if enthusiasm cools or earnings do not keep pace with expectations.

Explore the SWS fair ratio for TTM Technologies

Result: Price-to-Earnings of 78.2x (OVERVALUED)

However, you also need to weigh risks like sentiment cooling on AI and defense exposed names, or earnings growth falling short of what a 78.2x P/E implies.

Find out about the key risks to this TTM Technologies narrative.

Another way of looking at value

On top of the rich 78.2x P/E, our DCF model points to a future cash flow value of US$30.32 per share, well below the current US$99.87 price. That gap suggests expectations baked into the share price are very high. The question is whether you are comfortable paying that kind of premium.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out TTM Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own TTM Technologies Narrative

If you look at this and feel differently, or just prefer to work from your own numbers, you can build a custom view in minutes with Do it your way.

A great starting point for your TTM Technologies research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If TTMI has caught your eye, do not stop here. Broaden your watchlist with other focused ideas that could sharpen how you think about risk and opportunity.

- Spot potential value plays early by checking out these 877 undervalued stocks based on cash flows that line up prices with underlying cash flows.

- Zero in on fast movers in artificial intelligence using these 23 AI penny stocks that concentrate on companies linked to this theme.

- Strengthen your income shortlist by reviewing these 13 dividend stocks with yields > 3% that combine yield above 3% with stock market exposure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TTM Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TTMI

TTM Technologies

Manufactures and sells mission systems, radio frequency (RF) components, RF microwave/microelectronic assemblies, and printed circuit boards (PCBs) and substrates in the United States, Taiwan, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

156 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k10.0% overvalued

16 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9412.5% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87179.9% overvalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AB

Abhishekgarg on Pidilite Industries ·

High quality compounder, but current valuation leaves limited margin of safety.

Fair Value:₹1.31k2.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PA

Paddy_Ho on PaySauce ·

NZ company with gumption aims to provide services to SMEs across The Ditch

Fair Value:NZ$0.3623.6% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JC

JCAPITAL on Security Bank ·

YoY Percentage Growth: +5.8%

Fair Value:₱22169.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

55 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9826.5% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

35 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

38 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0