Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:SMCI

A Look At Super Micro Computer (SMCI) Valuation As AI Expansion And New Credit Facility Support Growth

Super Micro Computer (SMCI) is back in focus after expanding its manufacturing capacity around NVIDIA’s next generation AI processors and securing a new US$2b revolving credit facility to support AI focused inventory and operations.

See our latest analysis for Super Micro Computer.

The recent manufacturing expansion around NVIDIA’s next generation AI chips and the new US$2b credit facility come after a sharp reset, with a 90 day share price return of a 43.21% decline and a relatively flat year to date share price move. At the same time, the 3 year and 5 year total shareholder returns are very large, pointing to long term momentum that contrasts with more cautious recent trading.

If Super Micro’s AI push has your attention, this might be a good moment to see what other names are riding similar trends through high growth tech and AI stocks.

With SMCI down 43.21% over 90 days but still carrying very large multi year returns and trading at a 40.38% intrinsic discount and a 58.18% discount to analyst targets, is this weakness a buying opportunity, or is future growth already priced in?

Most Popular Narrative: 37.9% Undervalued

With Super Micro Computer closing at US$30.16 and the most followed narrative putting fair value around the high US$40s, the gap between price and modelled value is substantial and rooted in very specific growth and margin expectations.

The accelerating global adoption of AI and analytics continues to drive demand for high-performance, scalable server and data center solutions, positioning Super Micro for strong multi-year revenue growth as enterprises and nations build out AI infrastructure directly supporting projected revenue outperformance. The company's launch and rapid expansion of its Data Center Building Block Solution (DCBBS) enables customers to deploy turnkey, energy-efficient, and customized AI data centers faster than traditional solutions, supporting higher-margin product mix and improving gross and operating margins over time.

Want to understand why this model points to a sizeable discount to fair value? The core is aggressive revenue compounding, thicker margins, and a future earnings multiple below current sector norms. Curious how those pieces fit together into that fair value range and what assumptions do the heavy lifting?

Result: Fair Value of $48.53 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on big orders and margin assumptions holding up. Customer concentration or tougher AI server competition could quickly challenge that fair value story.

Find out about the key risks to this Super Micro Computer narrative.

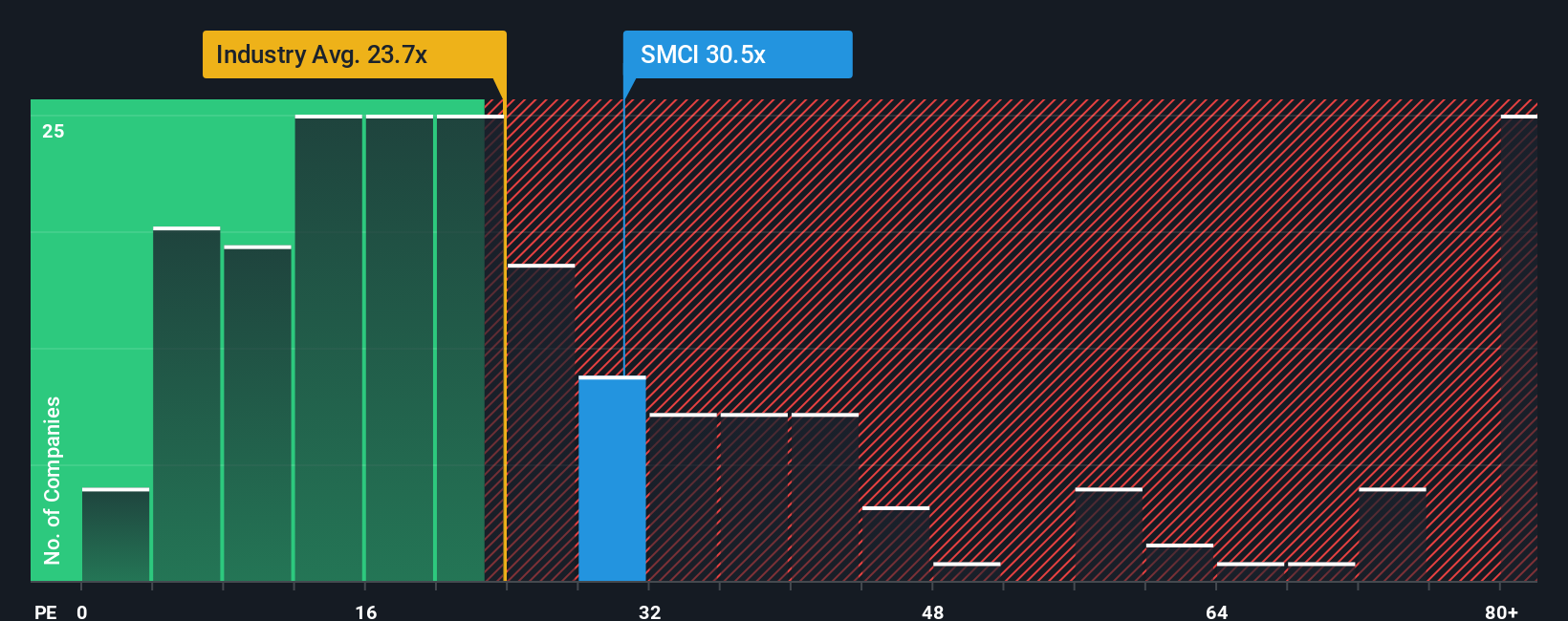

Another View: What The P/E Ratio Is Saying

While the narrative and fair value model point to SMCI trading at a sizeable discount, the P/E ratio tells a more mixed story. At 22.7x earnings, SMCI sits just above the global tech average of 22.3x, yet well below its own fair ratio of 69.5x and a peer average of 58.5x. That can look like value on a relative basis, but it also raises a simple question for you as an investor: is the current P/E a low entry point, or is it the market already baking in execution and margin risks?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Super Micro Computer Narrative

If you see the numbers differently or want to stress test these assumptions against your own view, you can build a custom thesis in minutes with Do it your way.

A great starting point for your Super Micro Computer research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready For More Investment Ideas?

If SMCI has sharpened your focus on where capital goes next, do not stop here. Widen your watchlist with other focused stock ideas before the market moves on.

- Target potential mispricings by screening for these 881 undervalued stocks based on cash flows that may offer a gap between share price and fundamentals.

- Ride the AI infrastructure trend by scanning these 28 AI penny stocks that are closely tied to data, computing power, and automation themes.

- Tap into recurring income potential with these 12 dividend stocks with yields > 3% that might help you build a more dependable cash flow profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SMCI

Super Micro Computer

Develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

89 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

30 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

JO

Joe222 on Encore Capital Group ·

ECPG is a solid company

Fair Value:US$120.3833.4% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Aftermath Silver ·

Aftermath Silver, A 35% Insider-Aligned Silver Stock With a Giant Critical Metals Twist

Fair Value:CA$30.3797.5% undervalued

5 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

RockeTeller on Selkirk Copper Mines ·

Selkirk Copper, Ex-Teck + 87% Hit Rate Maybe The Highest-Conviction Copper Restart in Canada Now

Fair Value:CA$21.7491.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

115 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1193 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

30 likesusers have liked this narrative