- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:SANM

Sanmina (SANM): Revisiting Valuation After a Sharp Pullback in a Strong Multi‑Year Share Price Run

Reviewed by Simply Wall St

Sanmina (SANM) has quietly turned into one of the stronger performers in tech manufacturing, with the stock more than doubling over the past year as revenue and net income growth stay solid.

See our latest analysis for Sanmina.

That pullback to a share price of $160.63 after a 1 day share price return of minus 9.1 percent looks more like a breather than a trend change, given the 90 day share price return of 34.8 percent and five year total shareholder return of 393.6 percent pointing to strong, sustained momentum.

If Sanmina’s run has you wondering what else might be quietly re rating, it is worth exploring fast growing stocks with high insider ownership as a next stop for potential ideas.

With revenue and earnings still climbing and the share price now sitting just below analyst targets, the key question is whether Sanmina remains undervalued or if the market is already pricing in its future growth.

Most Popular Narrative Narrative: 15.5% Undervalued

Compared to the narrative fair value of $190, Sanmina’s last close at $160.63 implies meaningful upside if the long term growth path plays out.

The imminent acquisition of ZT Systems is expected to add $5–6 billion of annual run rate revenue, positioning Sanmina to double its net revenue within three years and capitalize on explosive growth in data center and AI infrastructure investment. This is expected to provide a multi year boost to overall revenue and EPS accretion from synergies and integration.

Curious how this bold revenue surge, margin lift, and future earnings multiple all fit together. The narrative hides a surprisingly aggressive roadmap. Want to see it.

Result: Fair Value of $190 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this roadmap still hinges on smooth ZT Systems integration and on avoiding major revenue shocks from Sanmina’s heavily concentrated top customer base.

Find out about the key risks to this Sanmina narrative.

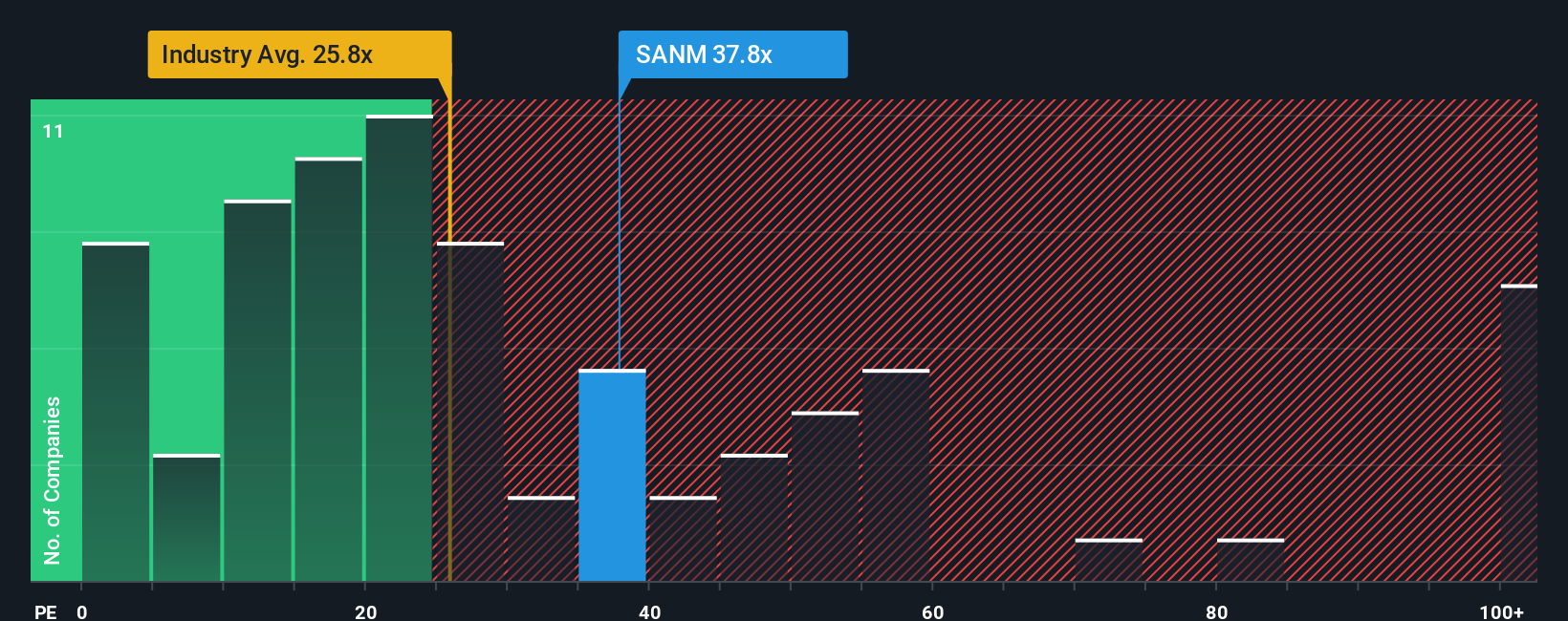

Another Take: Multiples Point to Richer Pricing

While the narrative fair value suggests upside, Sanmina’s 35.6x price to earnings ratio already sits above the US Electronic industry’s 24.8x, even if it is slightly below peer averages and a 38.7x fair ratio. That gap hints at less margin for error than the story implies.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Sanmina Narrative

If you would rather question these assumptions and dig into the numbers yourself, you can build a fresh narrative in just minutes: Do it your way.

A great starting point for your Sanmina research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Sanmina might look compelling, but you will kick yourself later if you ignore other opportunities that match your style, risk tolerance, and return targets.

- Capture early upside in smaller names by scanning these 3612 penny stocks with strong financials that already show robust balance sheets and disciplined capital management.

- Ride structural growth trends by targeting these 30 healthcare AI stocks bringing algorithm driven breakthroughs to diagnostics, treatment decisions, and hospital efficiency.

- Lock in reliable income potential with these 13 dividend stocks with yields > 3% that pair meaningful yields with sustainable payout ratios and resilient cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SANM

Sanmina

Provides integrated manufacturing solutions, components, products and repair, logistics, and after-market services in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)