Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:RELL

Here's Why We're Wary Of Buying Richardson Electronics' (NASDAQ:RELL) For Its Upcoming Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Richardson Electronics, Ltd. (NASDAQ:RELL) is about to trade ex-dividend in the next 4 days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. Meaning, you will need to purchase Richardson Electronics' shares before the 8th of November to receive the dividend, which will be paid on the 27th of November.

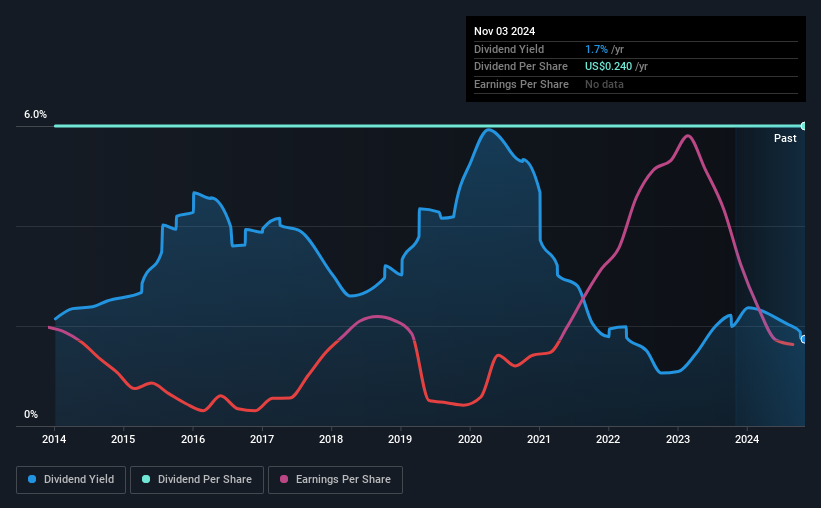

The company's upcoming dividend is US$0.06 a share, following on from the last 12 months, when the company distributed a total of US$0.24 per share to shareholders. Last year's total dividend payments show that Richardson Electronics has a trailing yield of 1.7% on the current share price of US$13.83. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Richardson Electronics can afford its dividend, and if the dividend could grow.

See our latest analysis for Richardson Electronics

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Richardson Electronics's dividend is not well covered by earnings, as the company lost money last year. This is not a sustainable state of affairs, so it would be worth investigating if earnings are expected to recover. Considering the lack of profitability, we also need to check if the company generated enough cash flow to cover the dividend payment. If cash earnings don't cover the dividend, the company would have to pay dividends out of cash in the bank, or by borrowing money, neither of which is long-term sustainable. Richardson Electronics paid out more free cash flow than it generated - 161%, to be precise - last year, which we think is concerningly high. We're curious about why the company paid out more cash than it generated last year, since this can be one of the early signs that a dividend may be unsustainable.

Richardson Electronics does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Richardson Electronics was unprofitable last year, but at least the general trend suggests its earnings have been improving over the past five years. Even so, an unprofitable company whose business does not quickly recover is usually not a good candidate for dividend investors.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. It looks like the Richardson Electronics dividends are largely the same as they were 10 years ago.

Get our latest analysis on Richardson Electronics's balance sheet health here.

Final Takeaway

Has Richardson Electronics got what it takes to maintain its dividend payments? First, it's not great to see the company paying a dividend despite being loss-making over the last year. Second, the dividend was not well covered by cash flow." With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Richardson Electronics.

So if you're still interested in Richardson Electronics despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. For example - Richardson Electronics has 1 warning sign we think you should be aware of.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:RELL

Richardson Electronics

Engages in the provision of engineered solutions, power grid and microwave tube, and related consumables worldwide.

Flawless balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor