Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqCM:OSS

One Stop Systems, Inc. (NASDAQ:OSS) Just Released Its First-Quarter Results And Analysts Are Updating Their Estimates

One Stop Systems, Inc. (NASDAQ:OSS) shareholders are probably feeling a little disappointed, since its shares fell 7.8% to US$2.67 in the week after its latest first-quarter results. Revenues of US$13m were in line with expectations, although statutory losses per share were US$0.06, some 11% smaller than was expected. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for One Stop Systems

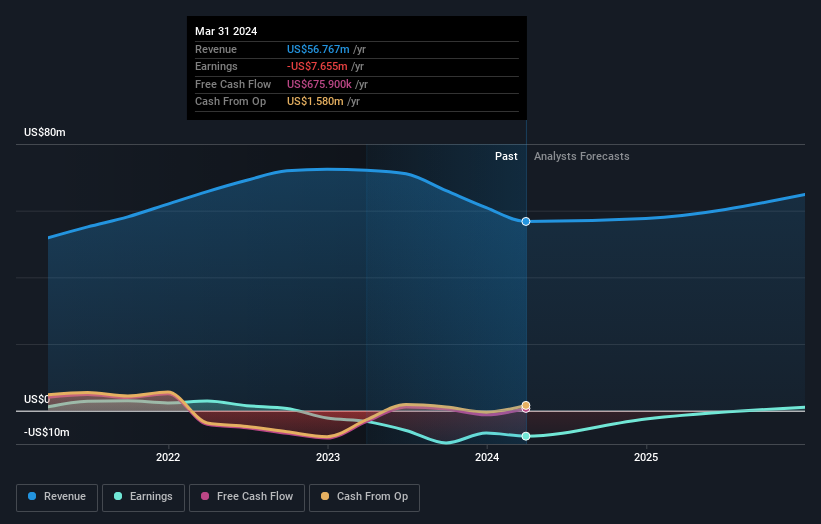

Following last week's earnings report, One Stop Systems' four analysts are forecasting 2024 revenues to be US$57.7m, approximately in line with the last 12 months. Losses are predicted to fall substantially, shrinking 59% to US$0.15. Before this earnings announcement, the analysts had been modelling revenues of US$58.1m and losses of US$0.14 per share in 2024. So it's pretty clear consensus is mixed on One Stop Systems after the new consensus numbers; while the analysts held their revenue numbers steady, they also administered a moderate increase in per-share loss expectations.

The consensus price target held steady at US$3.92, seemingly implying that the higher forecast losses are not expected to have a long term impact on the company's valuation. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic One Stop Systems analyst has a price target of US$5.50 per share, while the most pessimistic values it at US$3.00. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that One Stop Systems' revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 2.1% growth on an annualised basis. This is compared to a historical growth rate of 6.4% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 6.0% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than One Stop Systems.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for One Stop Systems going out to 2025, and you can see them free on our platform here.

It is also worth noting that we have found 4 warning signs for One Stop Systems that you need to take into consideration.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:OSS

One Stop Systems

Designs, manufactures, and markets rugged high-performance compute, high speed switch fabrics, and storage systems for edge applications of artificial intelligence and machine learning, sensor processing, sensor fusion, and autonomy in the United States and internationally.

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7063.2% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.5% undervalued

47 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0539.5% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15121.8% undervalued

91 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Investigator Silver ·

Investigator Silver, Leverage Exposed: $1/oz Move = $42M Cash for This ASX Developer

Fair Value:AU$2.3997.7% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.5% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$907.3239.7% undervalued

37 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.3% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1929.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.9% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative