Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:NSSC

Is It Too Late To Consider Napco Security Technologies (NSSC) After A 93% One Year Rally?

Reviewed by Bailey Pemberton

- If you are wondering whether Napco Security Technologies' current share price reflects its true worth, you are not alone. Many investors are trying to work out if the recent run still leaves room for value.

- The stock closed at US$46.61, with returns of 1.6% over the last 7 days, 26.3% over 30 days, 12.6% year to date and 92.9% over 1 year. The 3 year and 5 year returns stand at 47.4% and 182.8% respectively.

- Recent news coverage has largely focused on Napco Security Technologies as a specialist in security products, with investors paying attention to how its positioning in that space could relate to long term demand for its solutions. That backdrop helps frame the recent share price moves as the market reacts to evolving expectations about the business.

- On our checks, Napco Security Technologies scores 1 out of 6 for being undervalued. The next step is to look at how different valuation approaches line up on the stock and then consider an even richer way to think about valuation at the end of this article.

Napco Security Technologies scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Napco Security Technologies Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company could be worth by projecting its future cash flows and then discounting them back to today in $ terms.

For Napco Security Technologies, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $52.45 million. Analysts provide explicit forecasts out to 2027, with free cash flow of $49.10 million in 2026 and $50.45 million in 2027. Beyond that, Simply Wall St extrapolates further cash flows, with projections reaching about $61.14 million in 2035.

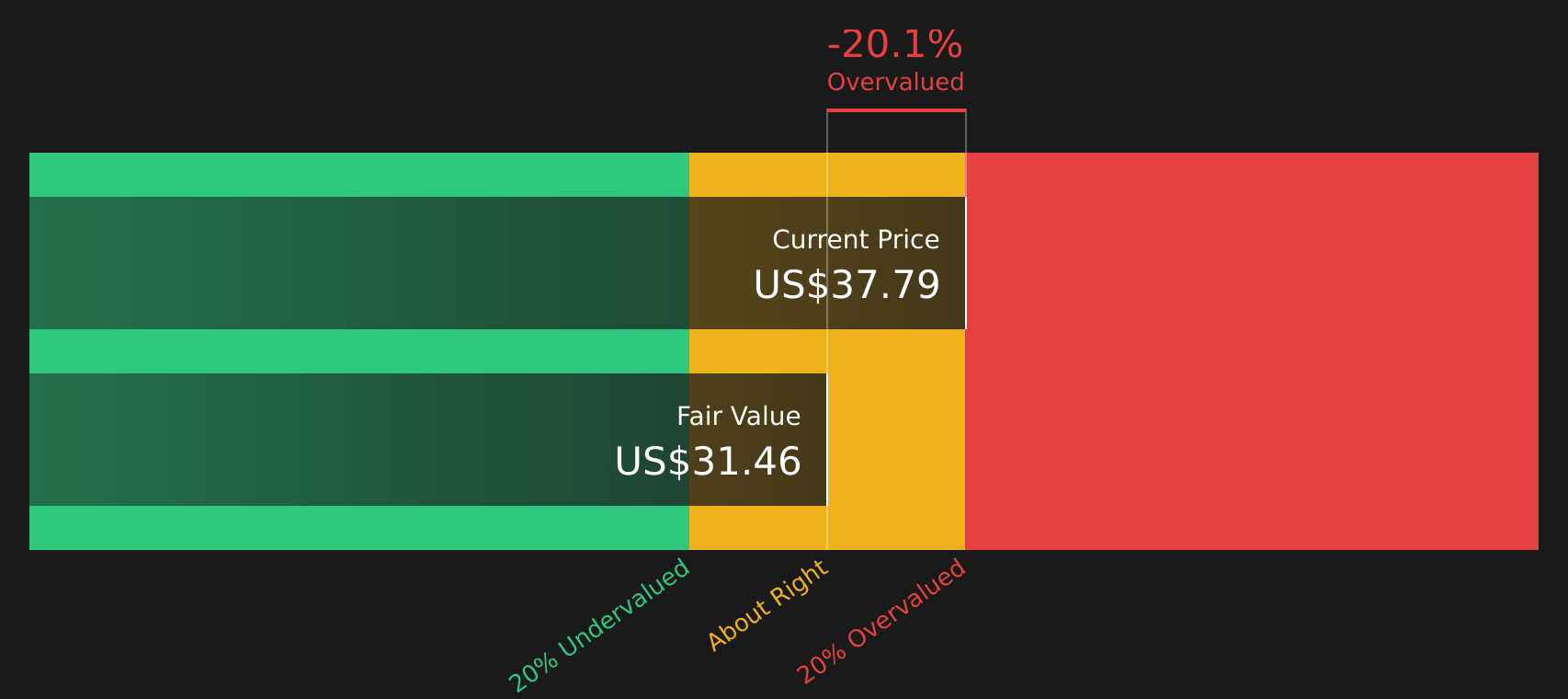

When all those projected cash flows are discounted back, the model arrives at an estimated intrinsic value of $25.88 per share. Compared with the recent share price of $46.61, the DCF output suggests the stock is about 80.1% overvalued on this measure.

This is only one lens on value. However, on this cash flow view, Napco Security Technologies does not screen as cheap today.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Napco Security Technologies may be overvalued by 80.1%. Discover 46 high quality undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Napco Security Technologies Price vs Earnings (P/E)

For profitable companies, the P/E ratio is a useful shortcut because it links what you pay for the stock directly to the earnings the business is producing today. Investors usually accept higher P/E ratios when they expect stronger growth or see lower risk, and tend to look for lower P/E ratios when growth prospects are more modest or risks feel higher.

Napco Security Technologies currently trades on a P/E of 35.1x. That sits above the Electronic industry average P/E of about 27.2x, yet below the peer group average of 78.5x. As a result, the market is assigning it a premium to the wider industry but not to the most highly priced peers.

Simply Wall St also calculates a proprietary “Fair Ratio” for each stock. For Napco Security Technologies, this Fair Ratio is 22.0x, which reflects factors such as its earnings growth profile, industry, profit margins, market cap and specific risks. This is more tailored than a simple comparison with peers or the broad industry because it adjusts for the company’s own characteristics rather than assuming one size fits all. On this measure, Napco Security Technologies’ current P/E of 35.1x sits above the 22.0x Fair Ratio. This points to the shares looking expensive on an earnings multiple basis.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Napco Security Technologies Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St’s Community page you can use Narratives, where you write the story you believe about Napco Security Technologies, link that story to specific revenue, earnings and margin forecasts, see the fair value that falls out of those numbers, then compare that Fair Value to today’s price to help decide whether the stock looks attractive or expensive. The Narrative updates automatically as new news or earnings arrive. One investor might build a cautious Napco view closer to the US$36.00 bear case, while another leans toward the US$52.00 bull case. Both can clearly see how their different assumptions, not just the latest P/E or DCF output, lead to different fair values and potential actions.

For Napco Security Technologies however we'll make it really easy for you with previews of two leading Napco Security Technologies Narratives:

🐂 Napco Security Technologies Bull Case

Fair value: US$49.67

Pricing gap vs fair value: the current price of US$46.61 is about 6.2% below this narrative fair value.

Assumed revenue growth: 10.14% a year

- Analysts tying this view together are assuming mid single digit to low double digit annual revenue growth, slightly higher profit margins over time and a higher future P/E multiple than the broader US Electronic industry.

- The story leans on growing high margin recurring service revenue, ongoing product and platform development, and the use of a strong balance sheet to fund dividends, buybacks and potential acquisitions.

- Key watchpoints in this view include hardware demand, dependence on specific recurring revenue products, tariff and cost pressures and confidence in financial reporting. All of these could affect how close reality comes to these assumptions.

🐻 Napco Security Technologies Bear Case

Fair value: US$36.00

Pricing gap vs fair value: the current price of US$46.61 is about 29.5% above this narrative fair value.

Assumed revenue growth: 7.16% a year

- The more cautious narrative assumes slower revenue growth, slightly thinner profit margins and a future P/E multiple that still sits above the current US Electronic industry level. Together these factors point to a lower fair value estimate.

- It highlights risks from higher compliance costs, wage and talent pressures, potential commoditisation of hardware and a tilt in spending toward other security solutions that could weigh on margins and growth.

- Supportive factors that could challenge this bear view include recurring revenue from StarLink radios, new SaaS and IoT style offerings, tariff related manufacturing advantages and a cash rich, debt free balance sheet.

If you want to go beyond these previews and see the full set of assumptions, price targets and risk checks that other investors are using for Napco Security Technologies, it is worth reading both narratives in full, starting with Curious how numbers become stories that shape markets? Explore Community Narratives.

Do you think there's more to the story for Napco Security Technologies? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Napco Security Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NSSC

Napco Security Technologies

Engages in the development, manufacturing, and sale of electronic security systems for commercial, residential, institutional, industrial, and governmental applications in the United States and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.167.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Lagenda Properties Berhad ·

Lagenda Continues To Offer Earnings Visibility Backed By Strong Sales Pipeline

Fair Value:RM 2.0330.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3223.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative