Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGM:MVIS

A Look At MicroVision (MVIS) Valuation After Nasdaq Minimum Bid Price Deficiency Notice

Nasdaq deficiency notice puts focus on MicroVision’s listing status

MicroVision (MVIS) recently received a deficiency notice from Nasdaq after its shares traded below the US$1 minimum bid price requirement for roughly a month. This has prompted fresh questions around its listing status.

See our latest analysis for MicroVision.

The deficiency notice comes after a weak run for MicroVision, with a 90 day share price return of 29.07% and a 1 year total shareholder return of 50.51%, pointing to fading momentum despite its US$0.8512 share price.

If this kind of volatility has you looking around the market, it could be a good moment to broaden your watchlist with high growth tech and AI stocks.

With the share price around US$0.85 and a 1 year total shareholder return of 50.51% decline, plus revenue of US$2.64m against a net loss of US$88.38m, is MicroVision a beaten down opportunity, or is the market already pricing in its future growth?

Most Popular Narrative: 98.6% Undervalued

MicroVision’s most followed narrative pegs fair value at $60 per share, a huge gap to the recent $0.85 close that instantly grabs attention.

The most misunderstood catalyst is the strategic and deliberate entry into the defense market. The establishment of a D.C.-area office is not a trivial move, it is a clear signal of intent to capture a piece of a newly defined market. The DoD's reclassification of small drones as "consumable commodities" has created a non-cyclical, government-funded Total Addressable Market (TAM) for tactical sensors overnight. This is not a potential market, it is a funded mandate.

Curious how a company with modest current revenue and a large net loss ends up with that kind of price tag in the narrative? According to TheWallstreetKing, the story leans heavily on future revenue mix, margin expansion, and a very optimistic earnings profile. Want to see exactly how those assumptions stack up to reach a $60 fair value?

Result: Fair Value of $60 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on MicroVision winning competitive defense and automotive contracts, and any setback there could quickly challenge the $60 narrative that investors are watching.

Find out about the key risks to this MicroVision narrative.

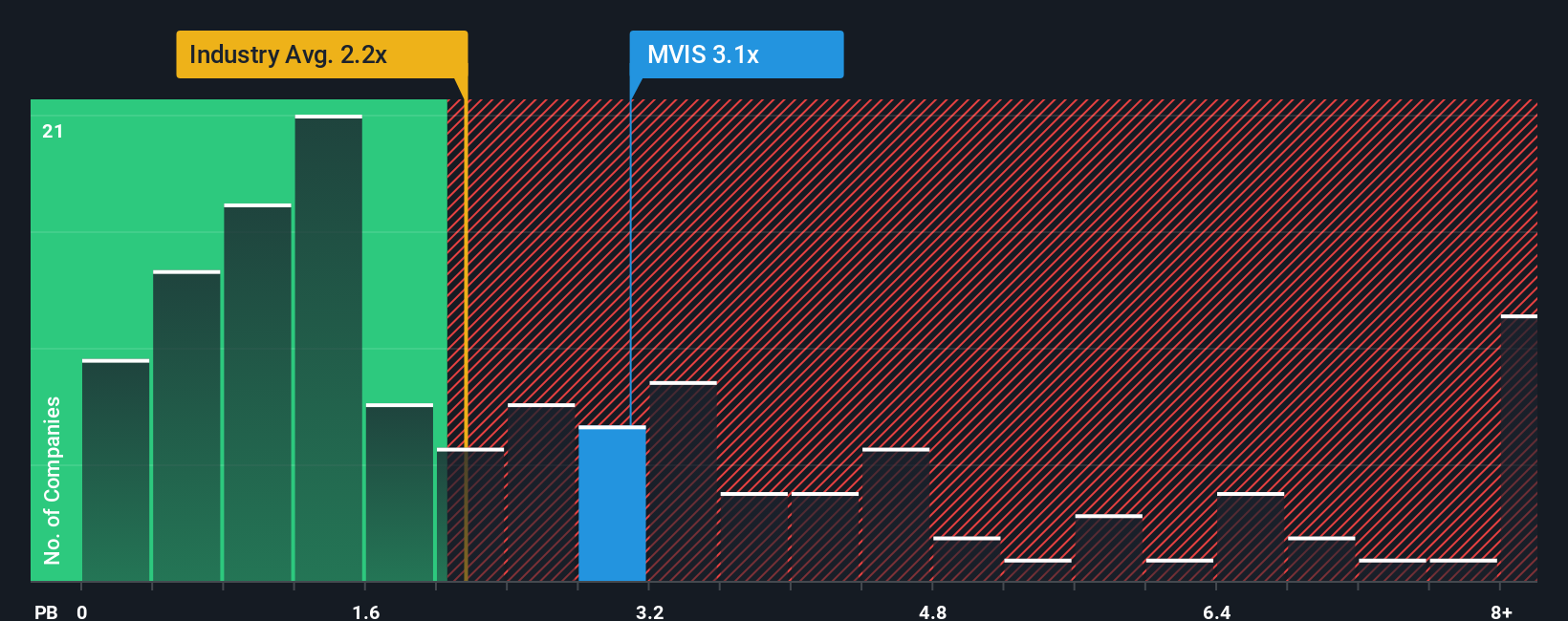

Another View: What The Market Is Paying Today

The $60 fair value narrative sits against a very different message from today’s trading multiples. MicroVision’s P/B of 2.9x is slightly higher than the US Electronic industry at 2.6x, yet below its peer average of 3.7x. That mix hints at more valuation risk than the headline $60 story suggests. Which signal do you take more seriously?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own MicroVision Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a custom thesis in just a few minutes with Do it your way.

A great starting point for your MicroVision research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If MicroVision has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to spot other opportunities that could suit your approach.

- Target potential value opportunities by checking out these 874 undervalued stocks based on cash flows that align with your preferred price and quality filters.

- Explore the growth story in artificial intelligence through these 24 AI penny stocks and see which names fit your convictions.

- Review these 18 cryptocurrency and blockchain stocks to identify crypto-related ideas that match your risk tolerance and objectives.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:MVIS

MicroVision

Develops and commercializes lidar sensors and perception solutions in the United States, Germany, and internationally.

Excellent balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0774.4% undervalued

219 followersusers have followed this narrative

1 commentusers have commented on this narrative

33 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.4% undervalued

55 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0716.3% undervalued

14 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3812.7% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

AV

avt on TROPHY GAMES Development ·

TROPHY GAMES Development Will See Revenue Rise by 22% in the Next 3 Years

Fair Value:DKK 19.0727.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

Thomas_Regrettier on ASML Holding ·

ASML at €725: Geopolitical Risk Priced In, Moat Still Intact

Fair Value:€92038.0% overvalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

CG

CG86 on Bausch + Lomb ·

$BLCO & $COO The Silence BEFORE the AGM: A Retail Investor’s Timeline, Findings, and Opinion on SUSPICIOUS SILENCE!

Fair Value:US$39.2358.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3956.1% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

42 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.1k% overvalued

37 followersusers have followed this narrative

11 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$587.3136.9% undervalued

1352 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

EL

Element1 on Greatland Resources ·

I can’t believe how inaccurate and out of date this site is—and people rely on it. Greatland owns tw...

0

|0

MI

Mikeymike on Auxly Cannabis Group ·

Id like to understand why they believe the profit margin is going decline so dramatically. Is it ene...

0

|0