- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:LFUS

Investors Met With Slowing Returns on Capital At Littelfuse (NASDAQ:LFUS)

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. That's why when we briefly looked at Littelfuse's (NASDAQ:LFUS) ROCE trend, we were pretty happy with what we saw.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Littelfuse is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.16 = US$534m ÷ (US$3.9b - US$572m) (Based on the trailing twelve months to December 2022).

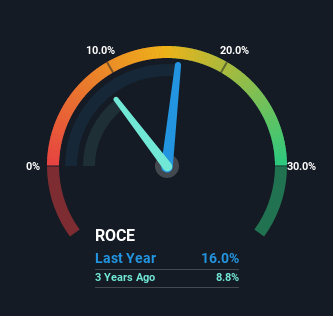

So, Littelfuse has an ROCE of 16%. In absolute terms, that's a satisfactory return, but compared to the Electronic industry average of 13% it's much better.

View our latest analysis for Littelfuse

Above you can see how the current ROCE for Littelfuse compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Littelfuse.

SWOT Analysis for Littelfuse

- Earnings growth over the past year exceeded the industry.

- Debt is not viewed as a risk.

- Dividends are covered by earnings and cash flows.

- Dividend is low compared to the top 25% of dividend payers in the Electronic market.

- Annual earnings are forecast to grow for the next 3 years.

- Good value based on P/E ratio compared to estimated Fair P/E ratio.

- Annual earnings are forecast to grow slower than the American market.

So How Is Littelfuse's ROCE Trending?

While the returns on capital are good, they haven't moved much. The company has consistently earned 16% for the last five years, and the capital employed within the business has risen 119% in that time. Since 16% is a moderate ROCE though, it's good to see a business can continue to reinvest at these decent rates of return. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

The Bottom Line

To sum it up, Littelfuse has simply been reinvesting capital steadily, at those decent rates of return. And given the stock has only risen 27% over the last five years, we'd suspect the market is beginning to recognize these trends. That's why it could be worth your time looking into this stock further to discover if it has more traits of a multi-bagger.

Littelfuse could be trading at an attractive price in other respects, so you might find our free intrinsic value estimation on our platform quite valuable.

While Littelfuse may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you're looking to trade Littelfuse, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:LFUS

Littelfuse

Designs, manufactures, and sells electronic components, modules, and subassemblies worldwide.

Flawless balance sheet average dividend payer.