Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:LFUS

Does Strong Q3 Electronics Beat and Resilient Execution Change The Bull Case For Littelfuse (LFUS)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Littelfuse recently reported its third-quarter results, delivering revenue of US$624.6 million, up 10.1% year on year, while meeting overall analyst expectations and surpassing estimates in key areas like Electronics revenue and adjusted operating income.

- Management’s emphasis on solid execution amid mixed market conditions highlights the company’s operational resilience, which may influence how investors view its longer-term earnings potential.

- We’ll now examine how this stronger-than-expected Electronics performance and resilient execution may reshape Littelfuse’s existing investment narrative and outlook.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Littelfuse Investment Narrative Recap

To own Littelfuse, you need to believe it can convert long term electrification and industrial demand into steadily improving earnings, despite exposure to cyclical end markets and power semiconductor softness. The latest quarter’s US$624.6 million in revenue and better than expected Electronics performance support the near term catalyst around margin resilience, while the biggest risk remains that prolonged weakness or disruption in key automotive and industrial segments could still pressure profitability. Overall, this quarter does not materially change that risk balance.

Among recent announcements, the company’s ongoing emphasis on M&A as a core use of capital is most relevant here, because it ties directly into how Littelfuse aims to reinforce its growth and portfolio breadth as demand evolves across EVs, grid infrastructure, and data centers. Successful execution on acquisitions could help offset cyclical volatility and power semiconductor challenges, but missteps or weak integration would amplify the risks investors are already watching.

Yet behind this solid quarter, there is still a meaningful risk that investors should be aware of if power semiconductor weakness...

Read the full narrative on Littelfuse (it's free!)

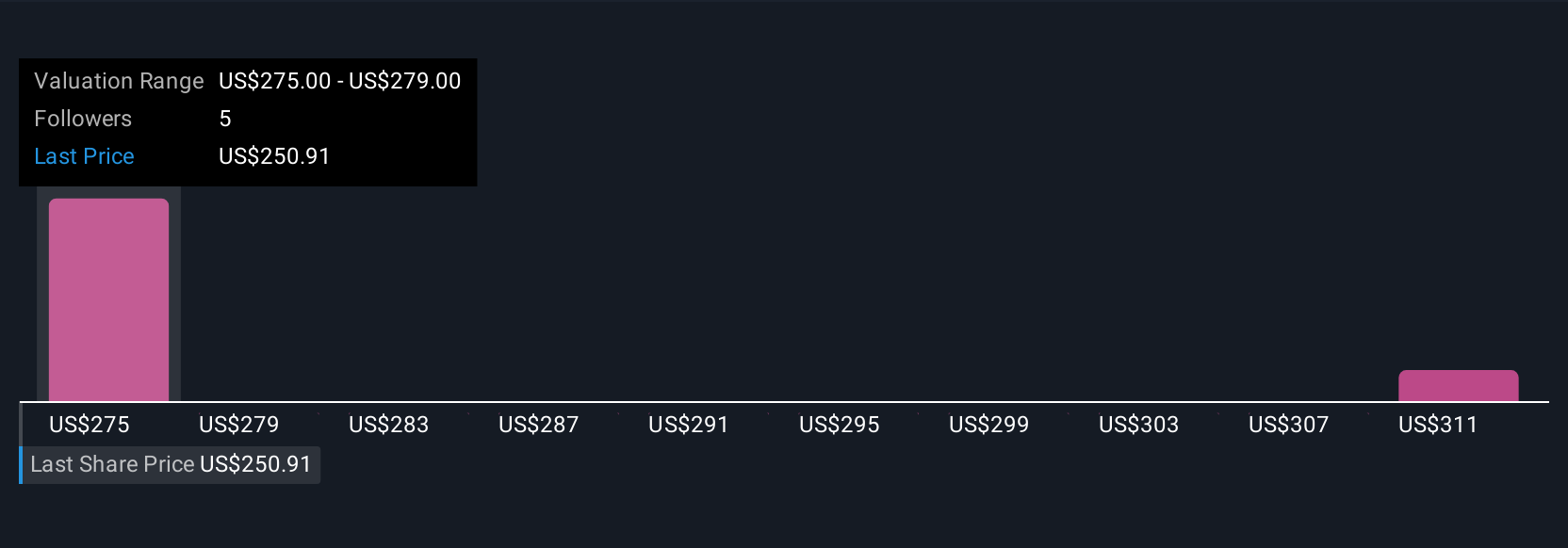

Littelfuse's narrative projects $2.9 billion revenue and $400.8 million earnings by 2028.

Uncover how Littelfuse's forecasts yield a $307.50 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Two fair value estimates from the Simply Wall St Community cluster between US$294.37 and US$307.50, underscoring how differently individual investors can view Littelfuse. Set against the company’s reliance on cyclical automotive and industrial demand, this spread in opinions invites you to compare multiple viewpoints on how resilient those earnings might really be.

Explore 2 other fair value estimates on Littelfuse - why the stock might be worth as much as 18% more than the current price!

Build Your Own Littelfuse Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Littelfuse research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Littelfuse research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Littelfuse's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:LFUS

Littelfuse

Designs, manufactures, and sells electronic components, modules, and subassemblies.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

59 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

59 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative