Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqCM:INVE

Companies Like Identiv (NASDAQ:INVE) Are In A Position To Invest In Growth

Just because a business does not make any money, does not mean that the stock will go down. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So, the natural question for Identiv (NASDAQ:INVE) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. Let's start with an examination of the business' cash, relative to its cash burn.

See our latest analysis for Identiv

How Long Is Identiv's Cash Runway?

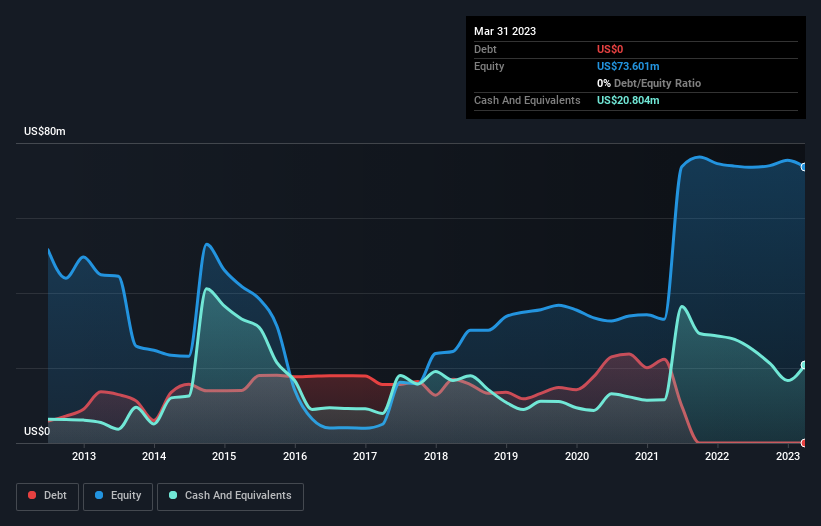

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. In March 2023, Identiv had US$21m in cash, and was debt-free. In the last year, its cash burn was US$17m. Therefore, from March 2023 it had roughly 15 months of cash runway. While that cash runway isn't too concerning, sensible holders would be peering into the distance, and considering what happens if the company runs out of cash. The image below shows how its cash balance has been changing over the last few years.

Is Identiv's Revenue Growing?

We're hesitant to extrapolate on the recent trend to assess its cash burn, because Identiv actually had positive free cash flow last year, so operating revenue growth is probably our best bet to measure, right now. While it's not that amazing, we still think that the 6.7% increase in revenue from operations was a positive. Clearly, however, the crucial factor is whether the company will grow its business going forward. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can Identiv Raise More Cash Easily?

Notwithstanding Identiv's revenue growth, it is still important to consider how it could raise more money, if it needs to. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of US$197m, Identiv's US$17m in cash burn equates to about 8.7% of its market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

Is Identiv's Cash Burn A Worry?

The good news is that in our view Identiv's cash burn situation gives shareholders real reason for optimism. Not only was its revenue growth quite good, but its cash burn relative to its market cap was a real positive. Cash burning companies are always on the riskier side of things, but after considering all of the factors discussed in this short piece, we're not too worried about its rate of cash burn. Taking a deeper dive, we've spotted 3 warning signs for Identiv you should be aware of, and 1 of them is significant.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:INVE

Identiv

Develops, manufactures, and supplies specialty IoT products in the United States, Europe, the Middle East, and the Asia-Pacific.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

18 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.8% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k13.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Procter & Gamble ·

Insiders Sell, Investors Watch: What’s Going On at PG?

Fair Value:US$1506.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CW

Cwburton on Verano Holdings ·

Waiting for the Inevitable

Fair Value:CA$5.5278.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.6% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8684.3% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Trending Discussion

OI

OilStates on Oil States International ·

This article is overall well written. However, to correct a few points and to highlight a few additional points: -The shift towards more stable long-cycle offshore and international projects does not increase volatility or exposure to short-cycle markets, quite the opposite. Offshore projects have a much longer investment cycle, duration, and low volatility given these are multi-decade assets. -The article notes a lack of exposure to renewables. Oil States has applied decades of experience in technologies for traditional oil & gas technologies into the renewables sector including transfer of fixed and floating offshore platform technologies into offshore wind, downhole perforating and well completions technologies into geothermal, along with over 50+ renewables projects completed. We are supportive of a broad energy mix, yet to meet growing global energy demand requires both traditional as well as lower carbon resources. Both elements as well as other industrial product orders continue to contribute to Oil States decade-high backlog, which provides significant future revenue visibility. -One of the main storylines not captured here is cash flow generation. 75% of Company revenues (up from 51% in 2022) now come from offshore and international work, which provides good margins. With the strength of the Offshore Manufactured Products business segment, the high-grading of U.S. domestic land activities to focus on higher margin business lines, free cash flow (a non-GAAP metric) has grown significantly ($70 million in free cash flow on a TTM basis as of Sept. 30, 2025). This is quite high for a Company at this market cap, which results in a higher free cash flow yield vs. peers. -Free cash is being used to repurchase shares, to pay down debt (nearing net-debt zero), and to increase returns to stockholders. More detail can be found in our latest investor presentation here: https://ir.oilstatesintl.com/events-and-presentations/default.aspx

0

|0