Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:FLEX

How Investors May Respond To Flex (FLEX) Expanding Data Center Partnerships Amid AI Infrastructure Boom

Reviewed by Sasha Jovanovic

- In the past week, Flex and LG Electronics announced a partnership to develop integrated modular cooling solutions for AI data centers, while Flex also revealed ongoing collaborations with NVIDIA and expanded its data center infrastructure operations in North America and Europe.

- These moves highlight Flex's commitment to addressing rapid growth in high-performance computing and position the company as a key supplier amid surging demand for scalable, energy-efficient data center solutions.

- We'll explore how Flex's alliances and data center focus strengthen its investment narrative in the context of accelerating AI infrastructure demand.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Flex Investment Narrative Recap

To invest in Flex, shareholders must have confidence in sustained demand for AI and data center infrastructure, and trust Flex's ability to secure major hyperscaler customers as they expand these high-growth verticals. The latest partnerships with LG Electronics and NVIDIA reinforce Flex's position as a supplier of scalable, energy-efficient solutions, which may support revenue growth but do not materially reduce exposure to customer concentration risk, the most important short-term catalyst remains continued hyperscaler contract wins, while the main risk still centers on customer insourcing and pricing pressures.

Among Flex's recent announcements, the company's revised full-year 2026 revenue guidance, now set between US$26.7 billion and US$27.3 billion, stands out, driven by strong data center demand. This upward adjustment is closely linked to the short-term catalyst created by Flex’s new high-value partnerships and product launches, suggesting the company’s expanding presence in the AI infrastructure market is translating directly into higher expectations for top-line performance.

However, despite current momentum, investors should be aware that if major customers decide to bring more manufacturing or key component production in-house, then...

Read the full narrative on Flex (it's free!)

Flex's outlook forecasts $29.1 billion in revenue and $1.3 billion in earnings by 2028. This assumes annual revenue growth of 3.7% and an earnings increase of about $409 million from the current $891.0 million.

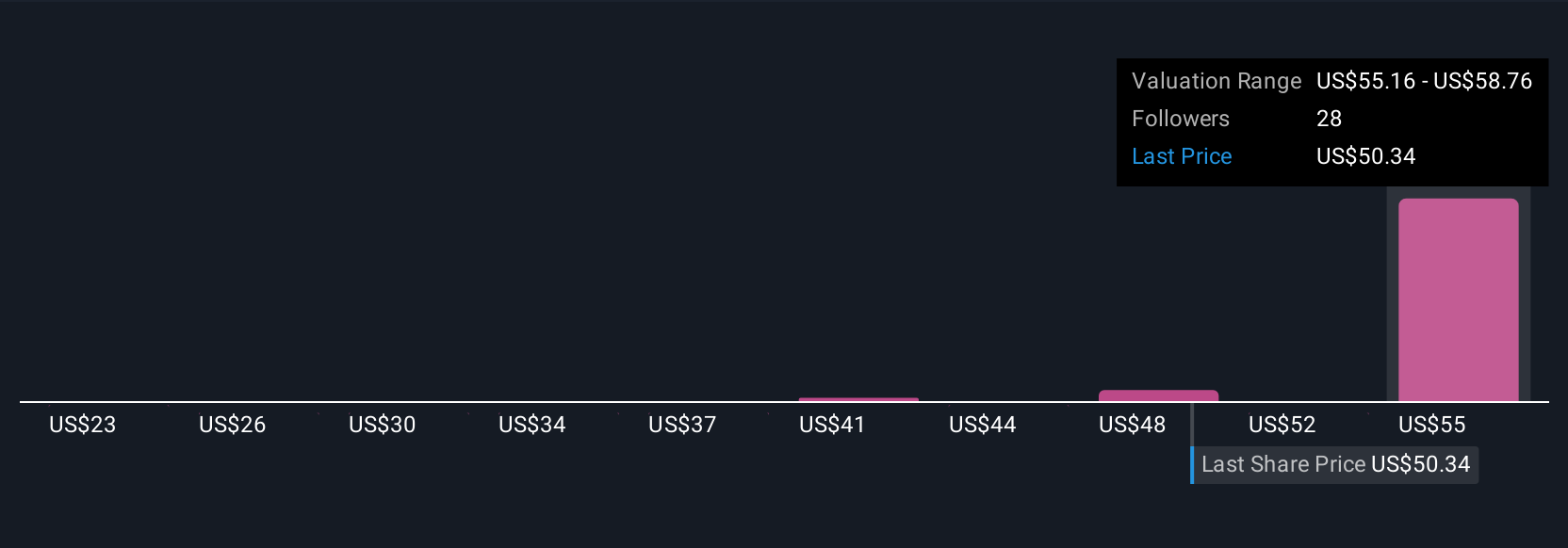

Uncover how Flex's forecasts yield a $74.37 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Five private investors from the Simply Wall St Community estimate Flex’s fair value between US$45 and US$74.37 per share. Supply chain diversification, identified as a key catalyst, continues to shape future revenue opportunities and competitive positioning, explore how your own viewpoint compares.

Explore 5 other fair value estimates on Flex - why the stock might be worth 28% less than the current price!

Build Your Own Flex Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Flex research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Flex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Flex's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FLEX

Flex

Provides technology innovation, supply chain, and manufacturing solutions to data center, communications, enterprise, consumer, automotive, industrial, healthcare, industrial, and power industries in the Americas, Asia, and Europe.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3076.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.167.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Lagenda Properties Berhad ·

Lagenda Continues To Offer Earnings Visibility Backed By Strong Sales Pipeline

Fair Value:RM 2.0330.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative