Advertisement

- United States

- /

- Communications

- /

- NasdaqGS:CSCO

Dividend Analysis: Why Cisco (NASDAQ:CSCO) is Still a Reliable Income Stock with Potential to Revitalize Growth

Summary:

- Cisco continues to sell network products, and their internet for the future (data/network infrastructure) is showing indications of high growth.

- The company pays a solid 3% dividend yield, and constantly engages in share buybacks.

- The dividends are affordable, but don't leave much additional cash as a margin of safety, and the company may need to take on debt if it plans additional projects.

With a 3% dividend yield, Cisco Systems, Inc. (NASDAQ:CSCO) is back in the focus for income investors. Historically, the company had solid performance, however we need to reevaluate their dividend paying qualities in order to see if Cisco is still appealing.

In order to be a good income stock, a company should satisfy some criteria:

- Pay a solid dividend above the risk for investing in the stock

- Financial stability and affordability of future dividends

- Demonstrate an ability to gradually grow the payout to investors

In this article, we will conduct our dividend analysis for Cisco Systems and see the potential risks for investors that want to be involved in the stock.

Business Overview

Companies change over time, so it is good to remind ourselves what business they are in, and how has the landscape changed in the past few years.

Cisco makes and sells networking hardware. Product sales accounted for 74% of last quarter's revenue, this includes products for routing, wireless, hybrid work devices, network security, optical networking, 5G networking. Most of these components have a software counterpart and are offered as a system solution for clients.

The company is also working on a cloud-first software offering for clients, which makes up 1.4% of revenues.

Services, in addition to product bundles, make up some 26.5% of revenues.

We can see that Cisco is overwhelmingly a network hardware & systems company, that offers solutions primarily for enterprise clients. Most segments noted an increase in the last six months, except the hybrid work segment, which declined by 8%.

It seems that Cisco is maintaining a stable revenue growth from their standard network systems, while their "Internet for the future" (networking infrastructure) is showing promising signs of being a high contributing segment.

Cisco Dividend Analysis

Yield

Starting with the yield, it seems that investors that buy the stock around the US$50 price point will get an annual yield of around 3%. This is close to the market top yielding companies of 3.9% but right at the average within the Communications industry.

Risk

When looking at the yield of a dividend stock, we should also ask what is the risk of this stock, and in quantitative terms we can use a Beta to measure this. For Cisco, our bottom up beta comes up at 0.988, which is about as risky as the market (1.0). Considering that the market (as measured by the S&P 500) yields 1.37%, we can see that investors are gaining 2.23 times more yield per unit of risk.

Payout

The payout refers to the % of free cash flow returned to shareholders. Classically, the payout is computed as the proportion of cash paid out vs what is retained in the company. Considering that companies are heavily engaged in buybacks, we should also account for that and see how much Cisco spent on dividends plus buybacks.

Cisco Systems paid out 45% of its free cash flow as dividends last year, amounting to about US$6.165b. The company also returned around 3.2% (US$8.5b) of its market capitalization to shareholders in the form of stock buybacks.

Summing up the cash dividends plus the estimated buybacks for 2022, we can infer that Cisco returned a total of US$14.6b, slightly above the estimated US$13.7b of free cash flows. This indicates that the company has an adjusted payout ratio of 107%, slightly above what it can afford.

---

Love details?

This could be a bid to re-capitalize in order to reduce the total cost of capital by making the cost of equity cheaper. Considering what they paid out, their effective cost of equity for 2021 is 5.5%. Calculated as US$14.6b / US$265b (Adjusted payout / End of year market cap).

---

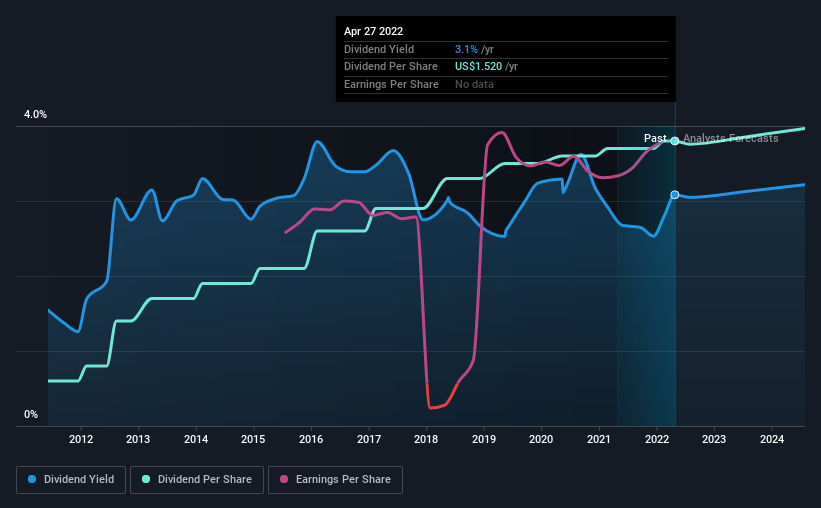

In the chart below, we can see the relationship between EPS, dividends per share and dividend yields.

Explore this interactive chart for our latest analysis on Cisco Systems!

Consider getting our latest analysis on Cisco Systems' financial position here.

Dividend Volatility

During the past 10-year period, the first annual payment was US$0.2 in 2012, compared to US$1.5 last year. This works out to be a compound annual growth rate (CAGR) of approximately 20% a year over that time.

It's rare to find a company that has grown its dividends rapidly over 10 years and not had any notable cuts, but Cisco Systems has done it, which is a great historical record.

Dividend Growth Potential

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) were growing, as this is essential to maintaining the dividend's purchasing power over the long term.

Cisco Systems has grown its earnings per share at 7.8% per annum over the past five years. Earnings per share are growing at an acceptable rate. Future growth in earnings is expected to decelerate to 6.7% on an annual basis, based on the projections of analysts following the company.

Conclusion

While Cisco is a mature company with low revenue growth, it has the opportunity to revitalize with its "Internet for the future" (networking infrastructure) segment, which noted a 44% growth in the last 6 months.

Income investors can probably rely on the company to deliver stable dividends and buybacks, but dividend growth may decelerate in the future.

An important part of Cisco which we did not cover in this analysis is the company's financial health, debt financing and management discipline. Investors can find details on these in our financial health and management sections.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:CSCO

Cisco Systems

Designs, develops, and sells technologies that help to power, secure, and draw insights from the internet in the Americas, Europe, the Middle East, Africa, the Asia Pacific, Japan, and China.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2552.0% undervalued

139 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0332.5% undervalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.528.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.725.6% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RC

rcb9 on DocuSign ·

Strip The Tax Benefit And Earnings Grew 36%

Fair Value:US$60.999.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RC

rcb9 on Boeing ·

The Operations Turned Profitable, The Balance Sheet Has Not

Fair Value:US$160.0145.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6814.9% undervalued

81 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.2% undervalued

246 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9116.1% overvalued

114 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$202.6284.3% overvalued

130 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

4

|0

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0