Advertisement

- United States

- /

- Communications

- /

- NasdaqGS:CSCO

Cisco Systems (NASDAQ:CSCO) has Stabilized their Balance Sheet and can Focus on the Future

The Balance Sheet is a crucial point of review for investors, because it gives insight for the flexibility and structural integrity of an organization. That is why we are going to assess Cisco Systems, Inc. (NASDAQ:CSCO) financial health, and see if they are running effective operations.

Check out our latest analysis for Cisco Systems

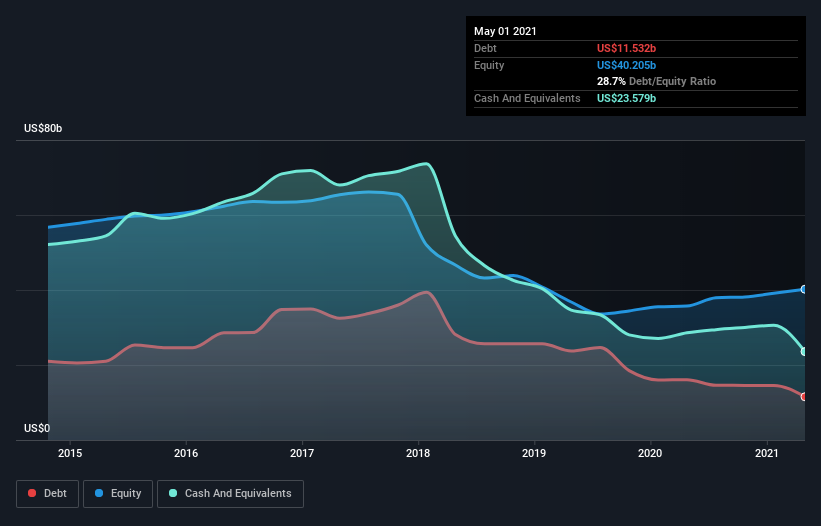

What Is Cisco Systems's Debt?

As you can see below, Cisco Systems had US$11.5b of debt at May 2021, down from US$16.1b a year prior. But it also has US$23.6b in cash to offset that, meaning it has US$12.0b net cash.

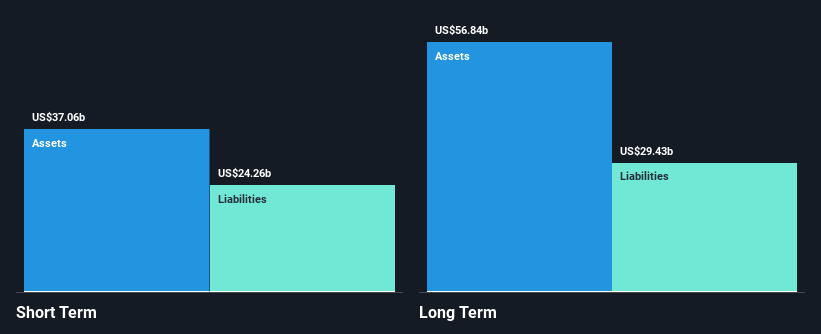

A Look At Cisco Systems' Liabilities

Zooming in on the latest balance sheet data, we can see that Cisco Systems had liabilities of US$24.3b due within 12 months and liabilities of US$29.4b due beyond that. On the other hand, it had cash of US$23.6b and US$9.34b worth of receivables due within a year. So, its liabilities total US$20.8b more than the combination of its cash and short-term receivables. Offsetting this are Cisco's long term assets, amounting to US$56.8b.

A complete picture can be seen in the chart below:

Of course, Cisco Systems has a large market capitalization of US$234.4b, so these liabilities are probably manageable.

Despite its noteworthy liabilities, Cisco Systems boasts net cash, so it's fair to say it does not have a heavy debt load!

But the other side of the story is that Cisco Systems saw its EBIT decline by 6.3% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle.

The balance sheet is clearly the area to focus on when you are analyzing debt. But ultimately, the future profitability of the business will decide if Cisco Systems can strengthen its balance sheet over time.

So if you're focused on the future, you can check out this free report showing analyst profit forecasts.

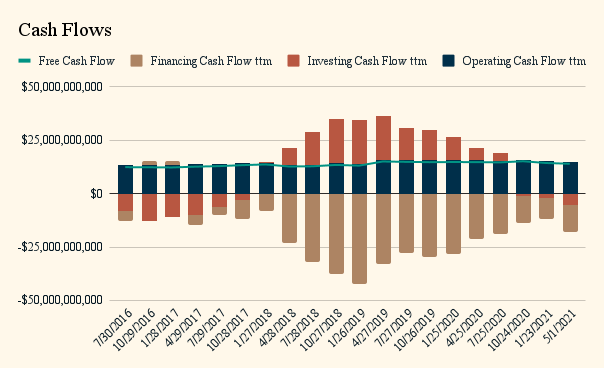

Finally, a business needs free cash flow to pay off debt. The difference between profits and free cash flow is that the first is in the books, and the second is in the bank. Investors should mostly be concerned with cash, because accountants have a lot of freedom to dance around profits.

Over the last three years, Cisco Systems actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces. Now, let's see how Cisco is handling its cash flows:

It seems that in the previous period, the largest cash outflows were, from financing - which mostly consist of debt repayments. That is why, at the beginning of our analysis, we say the debt balance slowly go down for Cisco. Cash from operating activities is quite constant, which indicates that the business has not improved both with regard to growth or efficiency of operations. The business is also returning cash to shareholders via their dividend, which currently has a 2.66% yield.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Cisco Systems has US$12.0b in net cash.

It impressed us with free cash flow of US$14b, being 105% of its EBIT.

The company is stabilizing its debt balance and has become more secure and stable. They can look towards the future and work on providing growth or maximizing value for shareholders. Overall, it looks like they have a healthy balance sheet.

So is Cisco Systems's debt a risk? It doesn't seem so to us. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Cisco Systems insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:CSCO

Cisco Systems

Designs, develops, and sells technologies that help to power, secure, and draw insights from the internet in the Americas, Europe, the Middle East, Africa, the Asia Pacific, Japan, and China.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.524.7% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.719.3% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on STLLR Gold ·

STLLR Gold, Eric Sprott + Agnico Backed: Massive Canadian Gold Developer at Junior Prices

Fair Value:CA$102.2298.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

PE

peter_4mgsy on Rhythm Pharmaceuticals ·

High-Growth Emerging Commercial Stage Biotech

Fair Value:US$13413.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on FreightCar America ·

ALL ABOARD THE VALUE TRAIN: WHY $RAIL MIGHT BE HEADED NORTH - FREIGHTCAR AMERICA - Long term price target of $25

Fair Value:US$2568.4% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

288 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

153 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

173 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

R2

R2R on Fonterra Shareholders Fund ·

SIMPLY WALL STREET please delete this Ai slop nonsense article.

0

|0