- United States

- /

- Software

- /

- NYSE:WK

Workiva (NYSE:WK) Sees 19% Revenue Growth in Q3 2024 Amidst ESG Expansion and Market Challenges

Reviewed by Simply Wall St

Workiva (NYSE:WK) continues to demonstrate a strong growth trajectory, with Q3 2024 results showing a 19% increase in subscription revenue and a 17% rise in total revenue, driven by its integrated reporting platform and leadership in sustainability solutions. Challenges such as rising losses and strategic shifts impacting service revenue exist, but the company is well-positioned to capitalize on emerging opportunities like the CSRD regulation and its enhanced ESG offerings. The report will cover key areas such as financial performance, market opportunities, regulatory challenges, and the strategic initiatives shaping Workiva's future.

Take a closer look at Workiva's potential here.

Core Advantages Driving Sustained Success for Workiva

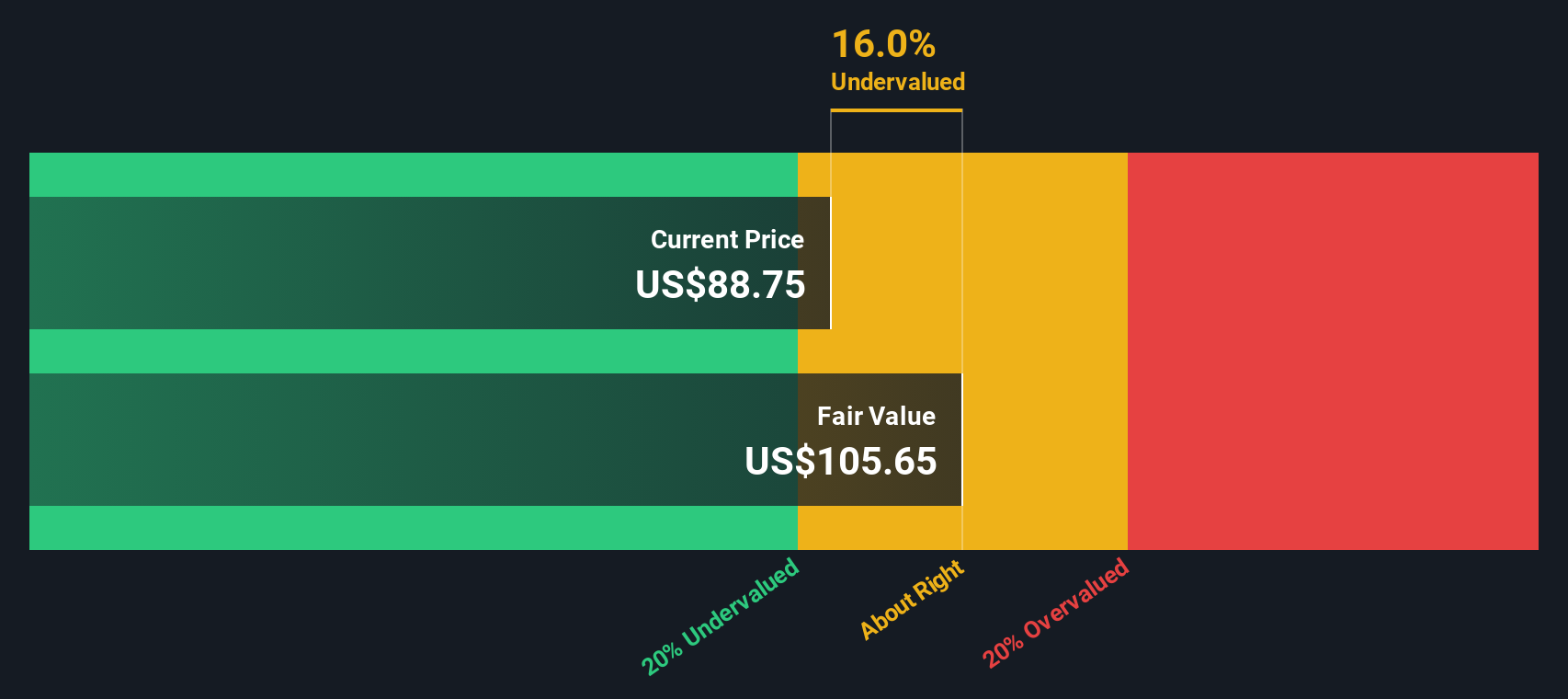

Workiva's financial performance in Q3 2024 underscores its growth trajectory, with subscription revenue increasing by 19% and total revenue by 17%. This growth is complemented by a 170 basis point rise in gross margin and a 70 basis point improvement in operating margin, reflecting effective internal execution and heightened customer demand. CEO Julie Iskow noted, "We delivered solid Q3 performance with subscription revenue growing at 19% and total revenue growing at 17%." The company has also achieved significant customer wins across diverse industries, highlighting the success of its integrated reporting platform. Furthermore, Workiva's leadership in sustainability and ESG solutions, driven by regulatory requirements like the EU CSRD, positions it well for future demand. The company's valuation, trading at a Price-To-Sales Ratio of 8x, aligns with its peers, though it remains below the SWS fair value estimate of $141.95, indicating its strong market positioning.

Challenges Constraining Workiva's Potential

The company remains unprofitable, with losses increasing over the past five years at a rate of 19.9% annually. CFO Jill Klindt reported a slight decline in professional services revenue, attributed to the strategic shift of setup and consulting services to partners, which could impact service revenue stability. Additionally, the reliance on partner-driven sales, particularly in Europe, introduces risks if these relationships are not effectively managed. The company's negative shareholder equity further complicates its financial health assessment, while shareholder dilution, with shares outstanding growing by 2.5%, adds to the financial strain.

Emerging Markets Or Trends for Workiva

Opportunities abound for Workiva, particularly with the upcoming CSRD regulation, which presents a significant chance to expand its European market presence. Julie Iskow highlighted the CSRD as a "game changer" for the company. The acquisition of Sustain.Life and the launch of Workiva Carbon enhance its ESG offerings, positioning Workiva to capture more market share in sustainability reporting. Furthermore, ERP upgrades and finance transformation projects offer valuable opportunities to attract new customers and sell additional solutions, bolstering Workiva's market position and driving performance.

Regulatory Challenges Facing Workiva

Workiva must navigate several external threats, including regulatory and political uncertainties in the U.S. that could affect its growth trajectory. The outcome of the U.S. presidential election and potential changes in SEC mandates create areas of uncertainty. Moreover, increasing competition in the ESG reporting space poses a challenge, as more companies enter the market with specialized solutions. As Julie Iskow stated, "The competitive environment is increasing, but we have a very differentiated platform." Significant insider selling over the past three months also raises concerns about insider confidence, which could impact investor sentiment.

Conclusion

Workiva's strong growth in subscription and total revenue, coupled with improvements in margins, reflects its effective execution and growing customer demand, positioning it well for future expansion, particularly in the ESG and sustainability sectors. However, challenges such as ongoing unprofitability, reliance on partner-driven sales, and negative shareholder equity pose risks that need careful management. The company's current trading at a Price-To-Sales Ratio of 8x, while aligned with peers, suggests it is well-positioned in the market but still trading below its estimated fair value of $141.95, indicating potential for future appreciation if it successfully capitalizes on emerging opportunities and navigates regulatory uncertainties. This balance of strengths and challenges will be crucial in determining Workiva's ability to enhance its market position and achieve sustained success.

Make It Happen

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

```Valuation is complex, but we're here to simplify it.

Discover if Workiva might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WK

Workiva

Provides cloud-based reporting solutions in the Americas and internationally.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Community Narratives