Advertisement

- United States

- /

- Software

- /

- NYSE:U

Unity Software Valuation Check After Surprise Profit And New AI And Coda Growth Push

Why Unity Software (U) is back on investors’ radar

Unity Software (U) has jumped back into focus after a surprise profitable Q3 2025, driven by its AI-powered Vector ad platform, along with a new Coda partnership for streamlined global in-app purchasing.

See our latest analysis for Unity Software.

Unity’s recent Coda integration and the profitable Q3 2025 have arrived during a choppy period, with a 30 day share price return of a 10.85% decline and a 90 day share price return of 11.15%. The 1 year total shareholder return of 75.07% points to strong longer term momentum despite mixed options activity and insider selling.

If you are watching how AI centric platforms like Unity are being priced, it could be a good moment to scan other high growth tech and AI names through high growth tech and AI stocks.

With Unity posting a surprise profit, a 1 year total return of 75.07% and the stock still trading below one estimate of intrinsic value, the key question is whether there is still a buying opportunity here or if markets already price in future growth.

Most Popular Narrative: 12% Undervalued

Unity Software’s most followed narrative pegs fair value at about $45.63 versus the last close of $40.16, putting a modest valuation gap in focus.

The expansion of Unity's client base and deepened partnerships with top-tier global gaming and enterprise players (e.g., Tencent, Scopely, Nintendo, BMW), along with unique cross-platform capabilities (including leading presence in China), are unlocking new long-term customer pipelines and diversified revenue streams, supporting both top-line growth and improved earnings stability.

Curious what kind of revenue growth, margin path, and future earnings multiple need to line up to support that valuation gap? The full narrative lays out a detailed financial roadmap that ties together Unity’s AI tools, subscriptions, and ecosystem partnerships into one coherent pricing story.

Result: Fair Value of $45.63 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still real pressure points here, including heavy AI spending that could keep Unity in a loss position, and tough competition from rival game engines and in house tools.

Find out about the key risks to this Unity Software narrative.

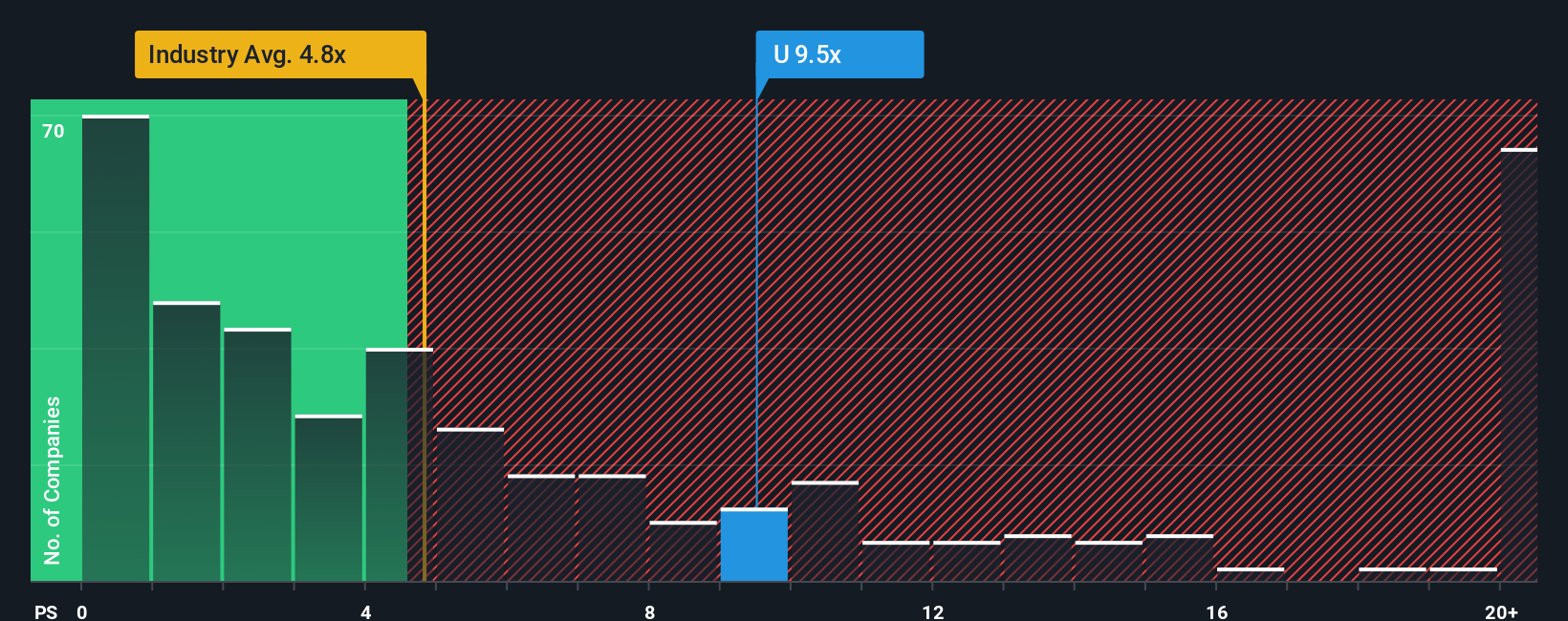

Another View: Rich Sales Multiple Versus “Undervalued” Tag

The SWS DCF model suggests Unity is trading about 29.3% below an estimate of future cash flow value at $56.81, which supports the undervalued label. However, the P/S of 9.5x is well above the US Software average of 4.6x, the peer average of 6.3x, and even the 8.5x fair ratio. This points to a full price for each dollar of current revenue.

With cash flows indicating “room to run” and sales multiples indicating “already expensive,” which signal do you place more weight on for your own thesis?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Unity Software Narrative

If you look at the numbers and come to a different conclusion, or simply want to test your own assumptions, you can build a custom thesis that fits your view in just a few minutes using Do it your way.

A great starting point for your Unity Software research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Unity has your attention, do not stop there. Use the Simply Wall St Screener to spot other opportunities that could fit your portfolio before others do.

- Spot early stage potential by checking out these 3515 penny stocks with strong financials that already back their stories with solid financials.

- Target fast growing themes by scanning these 24 AI penny stocks that are tied to the build out of artificial intelligence across industries.

- Focus on price discipline by reviewing these 876 undervalued stocks based on cash flows that are flagged as trading below estimated cash flow value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:U

Unity Software

Operates a platform to develop, deploy, and grow games and interactive experiences for mobile phones, PCs, consoles, and extended reality devices in the United States, China, Hong Kong, Taiwan, Europe, the Middle East, Africa, the Asia Pacific, Canada, and Latin America.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7056.5% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.225.0% undervalued

19 followersusers have followed this narrative

6 commentsusers have commented on this narrative

7 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0539.8% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15120.6% undervalued

82 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.885.3% undervalued

87 followersusers have followed this narrative

7 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on Retail Food Group ·

Retail Food Group (ASX: RFG) — Deep-Value Thesis

Fair Value:AU$1.250.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

Bakullizta on Indofood CBP Sukses Makmur ·

Blindly Bullish on Indofood CBP Sukses Makmur's 5.3% Revenue Growth

Fair Value:Rp9.05k30.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.8% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.4% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.6% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0