Advertisement

- United States

- /

- Software

- /

- NYSE:U

Unity Software (U) Valuation Check After Prolonged Share Price Weakness

Unity Software: recent performance snapshot

Unity Software (U) has been under pressure recently, with the stock showing declines over the past week, month, and past 3 months, and a year to date return of around a 44% decline.

Over the past year, the stock has delivered a total return of about an 18% decline, while the 3 year and 5 year total returns sit at roughly 31% and 80% declines. These figures set the backdrop for reviewing Unity’s current fundamentals.

See our latest analysis for Unity Software.

At a share price of US$24.94, Unity’s recent 7 day and 30 day share price returns of 38% and 46% declines suggest momentum has been fading, even as the 1 year total shareholder return is positive.

If Unity’s swings have you reassessing your options in game engines and AI tooling, it could be a good time to broaden your view across high growth tech and AI stocks.

Unity’s shares now sit well below some valuation estimates, even as revenue grows and the business remains loss making. Is the recent weakness setting up a mispriced entry point, or is the market already discounting future growth?

Most Popular Narrative: 35.2% Undervalued

According to the most followed narrative, Unity Software’s fair value sits at $38.48 per share compared with the recent close at $24.94, creating a sizable valuation gap.

Unity Software is in a solid financial position with positive cash flow and no immediate liquidity needs.

The synergy between Unity's Create and Grow solutions could prove to be a key competitive advantage, though the increasing competition in the advertising and gaming markets remains a challenge.

Want to see what is behind that gap between price and fair value? The narrative focuses on revenue expansion, margin improvements, and a richer future earnings multiple. Curious which mix of growth, profitability, and valuation assumptions drive the model toward $38.48 instead of $24.94? The full story connects those moving parts into one clear number.

Result: Fair Value of $38.48 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Unity still faces real pressure from ongoing losses of US$435.529m and tough competition in advertising and gaming, which could challenge this upside story.

Find out about the key risks to this Unity Software narrative.

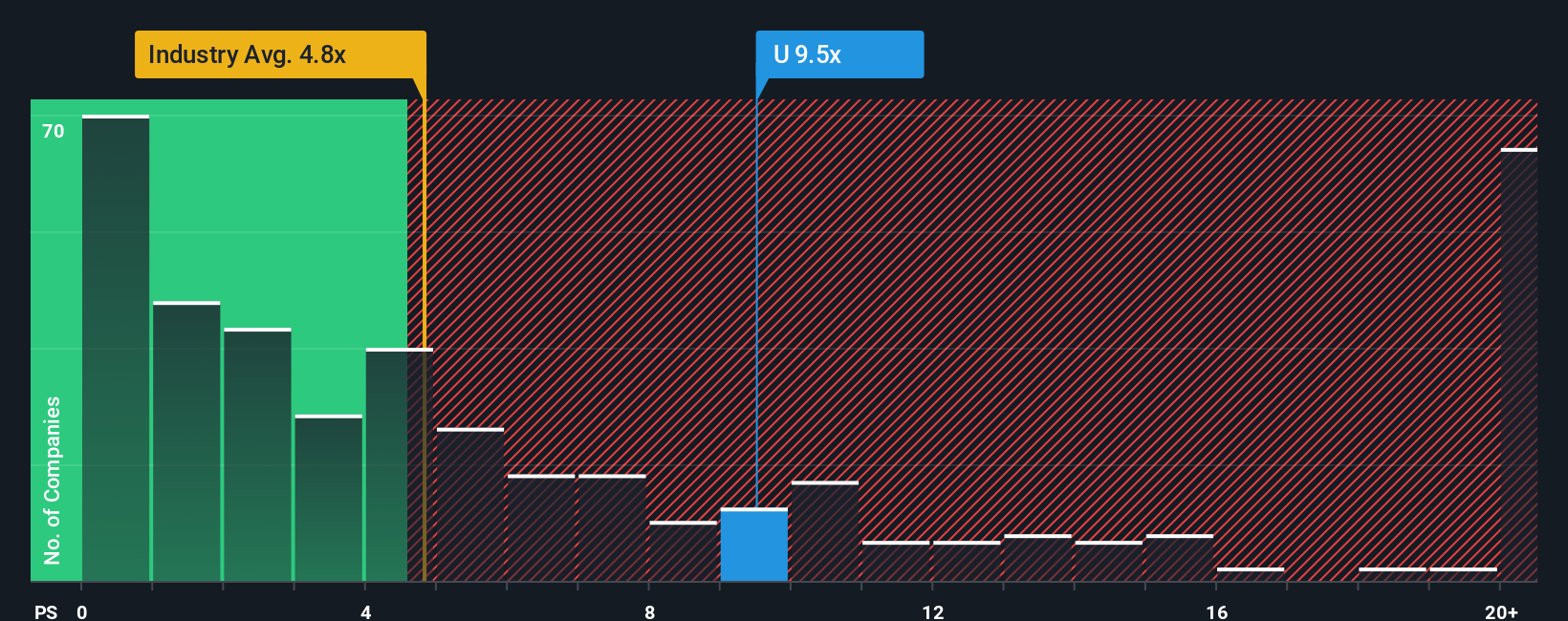

Another View: Price To Sales Sends A Different Signal

While our model points to good value compared with an estimated fair value of $54.09, Unity’s P/S ratio of 5.9x is higher than both the US Software industry average of 3.9x and the peer average of 5.4x, with a fair ratio of 7.3x suggesting the market could still shift. Does that premium P/S hint at extra risk if growth stalls, or reflect investors already paying up for Unity’s potential?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Unity Software Narrative

If you see the numbers differently or would rather test your own assumptions, you can build a fresh Unity view in just a few minutes by starting with Do it your way.

A great starting point for your Unity Software research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Unity has sharpened your thinking, do not stop here. Widen your search with a few focused stock ideas that match the way you like to invest.

- Spot potential value opportunities early by scanning these 867 undervalued stocks based on cash flows and compare businesses where cash flows and prices tell very different stories.

- Explore companies associated with artificial intelligence by checking out these 27 AI penny stocks that are directly tied to machine learning, automation, and data driven products.

- Access exposure to digital assets through companies instead of tokens by reviewing these 19 cryptocurrency and blockchain stocks that are building infrastructure for blockchain and cryptocurrency adoption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:U

Unity Software

Operates a platform to develop, deploy, and grow games and interactive experiences for mobile phones, PCs, consoles, and extended reality devices in the United States, China, Hong Kong, Taiwan, Europe, the Middle East, Africa, the Asia Pacific, Canada, and Latin America.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7057.9% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17044.9% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38033.4% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

TI

TimLee on 3REN Berhad ·

3REN Berhad Is Powering the Semiconductor Ecosystem and Smart Manufacturing

Fair Value:RM 0.6841.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

Anthony_Lee on Cheeding Holdings Berhad ·

Cheeding: The Hidden Beneficiary of Malaysia’s Power Grid Expansion

Fair Value:RM 1.242.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.653.2% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.6% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.2% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

0

|0

CO

composite32 on Ronesans Gayrimenkul Yatirim ·

Selamlar Teşekkürler.. Radarımda olan bir şirket değil, Halka açıklık oranı %40'ın üzerinde olan şir...

0

|0