- United States

- /

- Diversified Financial

- /

- NYSE:TOST

Shareholders in Toast (NYSE:TOST) are in the red if they invested a year ago

Most people feel a little frustrated if a stock they own goes down in price. But sometimes broader market conditions have more of an impact on prices than the actual business performance. Over the year the Toast, Inc. (NYSE:TOST) share price fell 13%. But that actually beats the market decline of 13%. Toast may have better days ahead, of course; we've only looked at a one year period. Unfortunately the last month hasn't been any better, with the share price down 34%. Importantly, this could be a market reaction to the recently released financial results. You can check out the latest numbers in our company report.

Now let's have a look at the company's fundamentals, and see if the long term shareholder return has matched the performance of the underlying business.

Check out our latest analysis for Toast

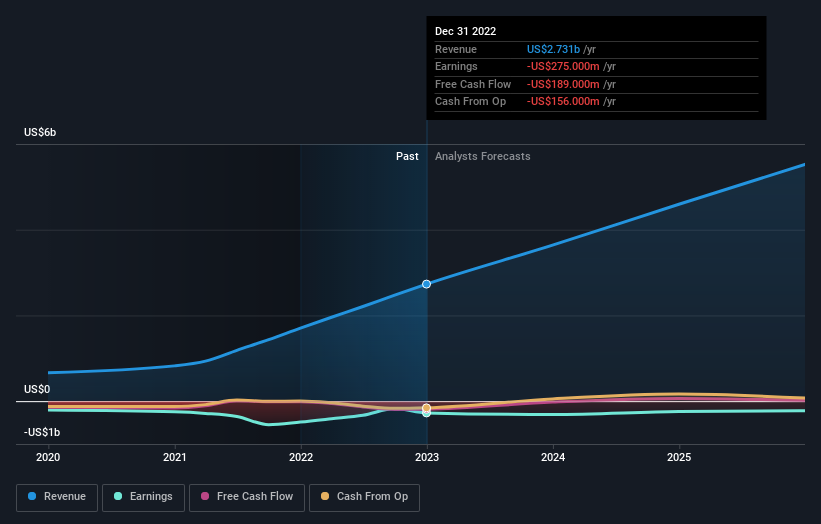

Given that Toast didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. When a company doesn't make profits, we'd generally expect to see good revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

In the last year Toast saw its revenue grow by 60%. That's a strong result which is better than most other loss making companies. Given that the broader market is down the 13% drop last year isn't too bad. Given the strong revenue growth, it may simply be that the stock is suffering from market conditions. For us, this sort of situation smells of opportunity - the share price is down but the revenue is up. Either way, we'd say the mismatch between the revenue growth and the share price justifies a closer look.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We're pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. This free report showing analyst forecasts should help you form a view on Toast

A Different Perspective

Having lost 13% over the year, Toast has generated a return within the same ballpark as the broader market. Unfortunately, last year's performance may indicate unresolved challenges, and the share price has continued to drop, down 8.8% over the last three months. Most people would be understandably disheartened by this sort of performance, given the lack of a long term history. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. To that end, you should be aware of the 3 warning signs we've spotted with Toast .

Of course Toast may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Toast might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:TOST

Toast

Operates a cloud-based digital technology platform for the restaurant industry in the United States, Ireland, India, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)