Advertisement

- United States

- /

- Software

- /

- NYSE:TDC

Is Teradata’s Cloud Pivot Creating a 2025 Value Opportunity After Recent Share Price Pullback?

Reviewed by Bailey Pemberton

- Wondering if Teradata is quietly turning into a value opportunity, or if the market is rightly cautious at around $29.68? This breakdown will help you decide whether the current price really makes sense.

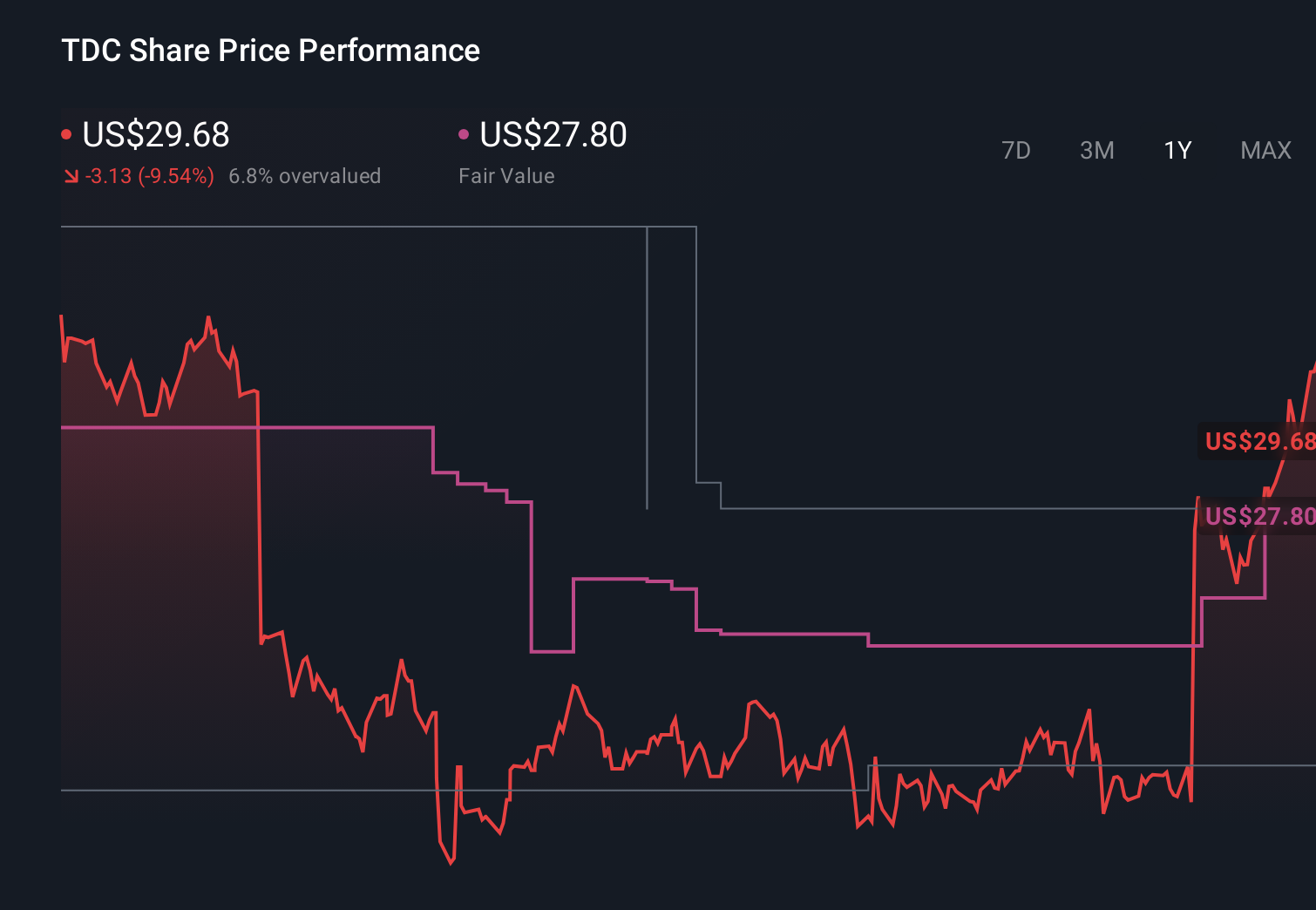

- The stock has slipped about 5.5% over the last week but is still up roughly 9.0% over the past month, leaving shares down 3.2% year to date and about 9.5% lower over the last year. This pattern hints at shifting sentiment rather than a clear trend.

- Recently, the market has been reacting to Teradata's ongoing push into cloud based analytics platforms and partnerships that aim to make its data tools more integral to large enterprise workflows. At the same time, investors are weighing competitive pressure from hyperscalers and other analytics vendors, which helps explain why the share price has been choppy rather than on a straight path higher.

- Despite that mixed performance, Teradata scores a solid 5 out of 6 on our valuation checks. This suggests it screens as undervalued on most metrics, and next we will unpack those methods in detail before looking at an even better way to think about what the stock is really worth.

Find out why Teradata's -9.5% return over the last year is lagging behind its peers.

Approach 1: Teradata Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in dollar terms.

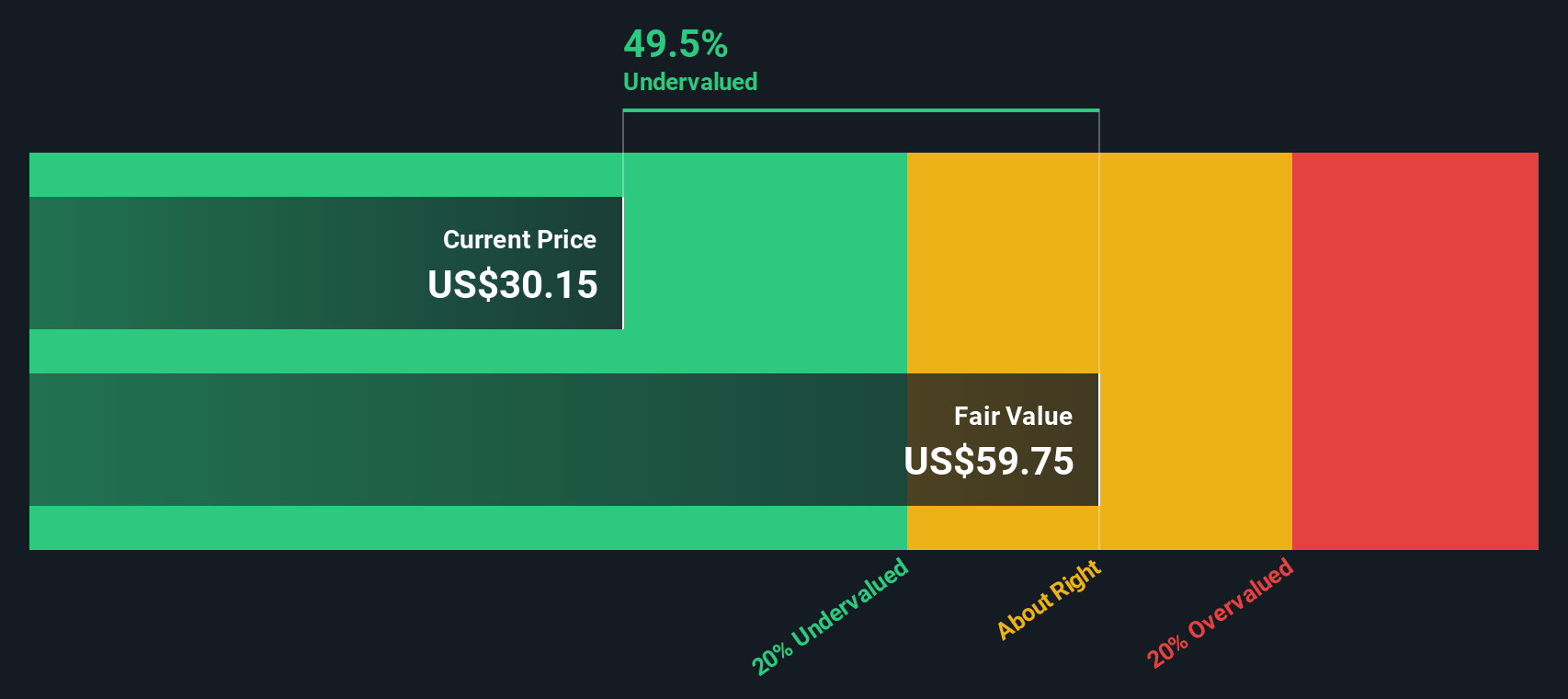

For Teradata, the 2 Stage Free Cash Flow to Equity model starts with last twelve months Free Cash Flow of about $280 million and uses analyst forecasts, followed by Simply Wall St extrapolations, to project how that cash flow could grow. Free Cash Flow is expected to rise to roughly $433 million by 2035, with mid single digit annual growth embedded in the later years of the forecast.

When all those projected cash flows are discounted back, the model arrives at an intrinsic value of about $59.75 per share. Compared to a market price around $29.68, this suggests the stock is trading at roughly a 50.3% discount to its estimated fair value, indicating the market may be heavily discounting Teradata's future cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Teradata is undervalued by 50.3%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

Approach 2: Teradata Price vs Earnings

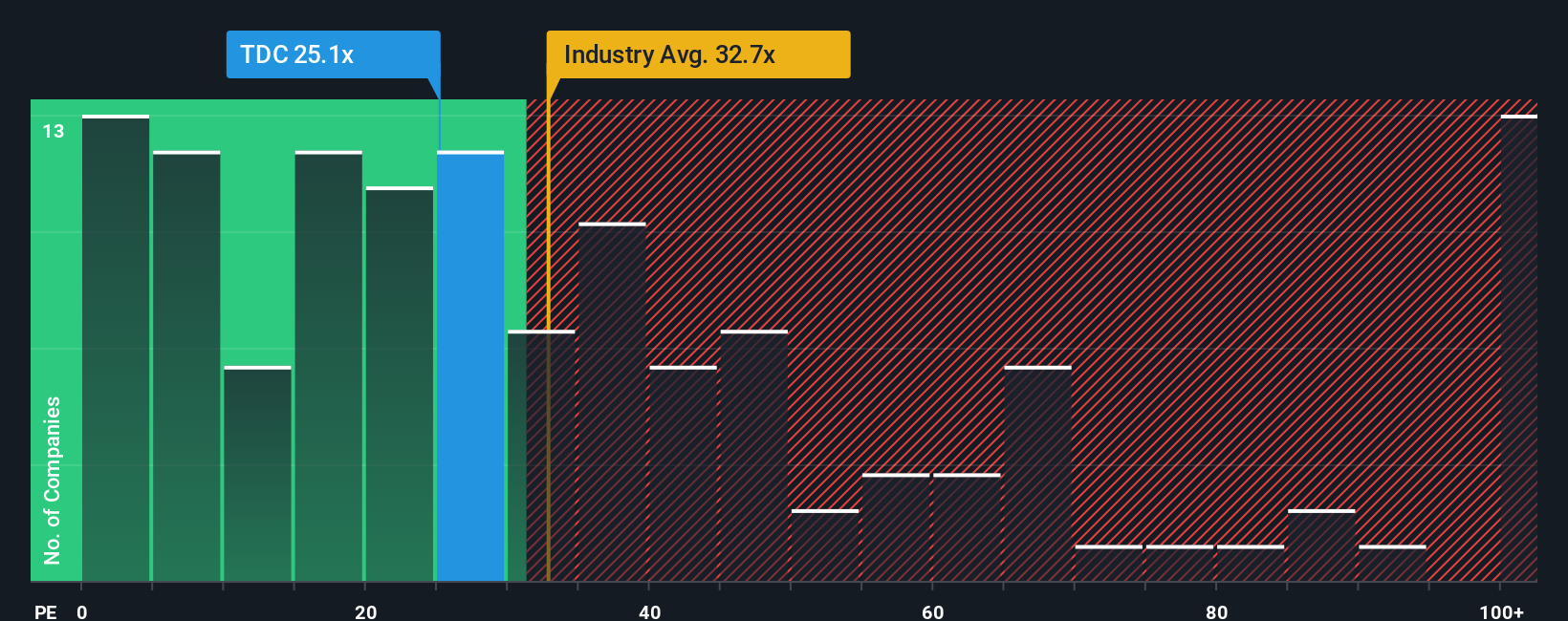

For a profitable company like Teradata, the price to earnings ratio is a useful way to gauge how much investors are willing to pay for each dollar of current earnings. A higher PE can be justified when a business has strong, visible growth prospects and relatively low risk, while slower growth or higher uncertainty usually calls for a lower, more conservative PE.

Teradata currently trades at about 23.44x earnings, which is below both the broader Software industry average of roughly 32.36x and the 29.05x multiple seen across close peers. On the surface, that discount suggests the market is more cautious about Teradata than about many other software names. However, simple comparisons like this do not fully capture company specific factors such as growth trajectory, profitability profile, balance sheet strength, and business risk.

This is where Simply Wall St's Fair Ratio comes in. Our Fair PE Ratio for Teradata is 24.89x, which reflects expectations for its earnings growth, margins, industry positioning, market cap and risk characteristics. Because it is tailored to the company, this Fair Ratio is more informative than a straight industry or peer comparison. With the current PE of 23.44x sitting moderately below the Fair Ratio, the shares screen as modestly undervalued on this metric.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1457 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Teradata Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Teradata’s story with a concrete forecast for its future revenue, earnings and margins, and then translate that into a Fair Value you can compare against today’s share price. On Simply Wall St’s Community page, millions of investors use Narratives to write down what they believe is driving a company, plug in their expectations, and instantly see whether their Fair Value suggests Teradata is a buy, hold, or sell at the current price, with those valuations automatically updating as new news or earnings arrive. For Teradata, a bullish Narrative might assume its AI partnerships, hybrid cloud strength and margin expansion justify a Fair Value well above the recent analyst high of around $42, while a more cautious Narrative that focuses on revenue headwinds, competitive pressure and slower cloud migration might anchor closer to or even below the $22 bear case. Comparing these perspectives helps you decide which story and price you actually believe.

Do you think there's more to the story for Teradata? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Teradata might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TDC

Teradata

Provides an AI and knowledge platforms in the United States and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$36.8311.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on MM Computer Systems Berhad ·

MM Computer Systems' Latest Contract Wins Reinforce Growth Momentum After Listing

Fair Value:RM 0.3313.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative