- United States

- /

- Software

- /

- NYSE:RAMP

Shareholders in LiveRamp Holdings (NYSE:RAMP) are in the red if they invested five years ago

In order to justify the effort of selecting individual stocks, it's worth striving to beat the returns from a market index fund. But every investor is virtually certain to have both over-performing and under-performing stocks. At this point some shareholders may be questioning their investment in LiveRamp Holdings, Inc. (NYSE:RAMP), since the last five years saw the share price fall 40%.

So let's have a look and see if the longer term performance of the company has been in line with the underlying business' progress.

Check out our latest analysis for LiveRamp Holdings

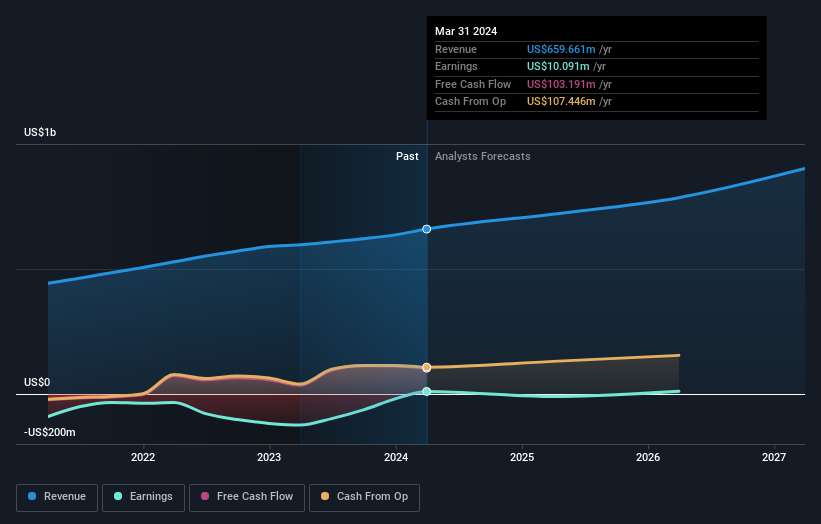

We don't think that LiveRamp Holdings' modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

Over five years, LiveRamp Holdings grew its revenue at 15% per year. That's well above most other pre-profit companies. The share price drop of 7% per year over five years would be considered let down. So you might argue the LiveRamp Holdings should get more credit for its rather impressive revenue growth over the period. If that's the case, now might be the smart time to take a close look at it.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

We know that LiveRamp Holdings has improved its bottom line lately, but what does the future have in store? This free report showing analyst forecasts should help you form a view on LiveRamp Holdings

A Different Perspective

LiveRamp Holdings shareholders gained a total return of 16% during the year. But that return falls short of the market. On the bright side, that's still a gain, and it is certainly better than the yearly loss of about 7% endured over half a decade. It could well be that the business is stabilizing. It's always interesting to track share price performance over the longer term. But to understand LiveRamp Holdings better, we need to consider many other factors. Case in point: We've spotted 2 warning signs for LiveRamp Holdings you should be aware of.

But note: LiveRamp Holdings may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:RAMP

LiveRamp Holdings

A technology company, operates a data collaboration platform in the United States, Europe, the Asia-Pacific, and internationally.

Flawless balance sheet and fair value.