Advertisement

- United States

- /

- Professional Services

- /

- NYSE:PAYC

We Think Paycom Software (NYSE:PAYC) Can Manage Its Debt With Ease

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Paycom Software, Inc. (NYSE:PAYC) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Paycom Software

What Is Paycom Software's Net Debt?

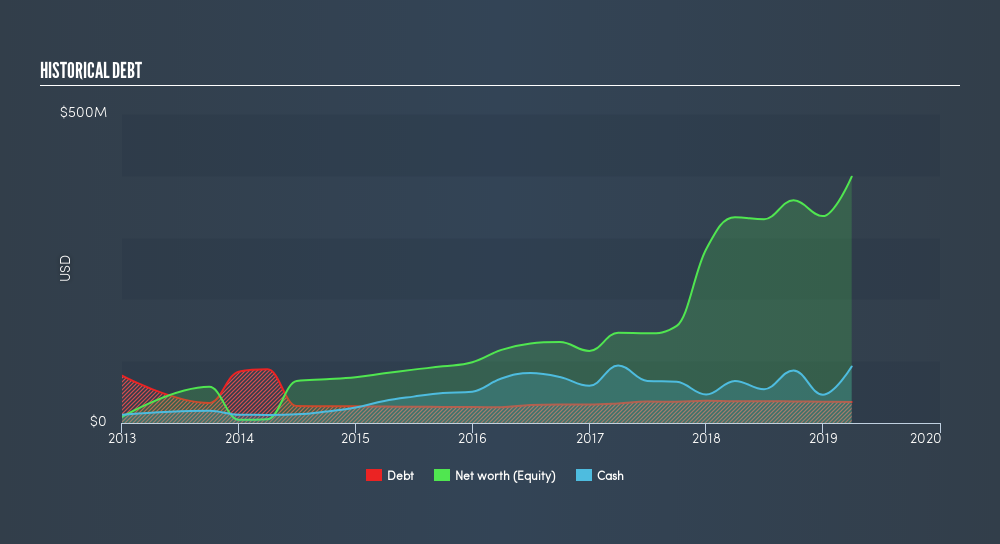

As you can see below, Paycom Software had US$34.0m of debt, at March 2019, which is about the same the year before. You can click the chart for greater detail. However, its balance sheet shows it holds US$91.3m in cash, so it actually has US$57.4m net cash.

A Look At Paycom Software's Liabilities

We can see from the most recent balance sheet that Paycom Software had liabilities of US$1.48b falling due within a year, and liabilities of US$180.6m due beyond that. Offsetting these obligations, it had cash of US$91.3m as well as receivables valued at US$3.84m due within 12 months. So it has liabilities totalling US$1.57b more than its cash and near-term receivables, combined.

Given Paycom Software has a humongous market capitalization of US$13.4b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Given that Paycom Software has more cash than debt, we're pretty confident it can manage its debt safely.

On top of that, Paycom Software grew its EBIT by 44% over the last twelve months, and that growth will make it easier to handle its debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Paycom Software's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Paycom Software has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Paycom Software produced sturdy free cash flow equating to 75% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While Paycom Software does have more liabilities than liquid assets, it also has net cash of US$57m. And it impressed us with its EBIT growth of 44% over the last year. So is Paycom Software's debt a risk? It doesn't seem so to us. Another factor that would give us confidence in Paycom Software would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:PAYC

Paycom Software

Provides cloud-based human capital management (HCM) solution delivered as software-as-a-service for small to mid-sized companies in the United States.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

72 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

23 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.1% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NE

newsfinder11221 on Tanco Holdings Berhad ·

Tanco Holdings Expands Growth Pipeline With Smart Port, ECRL And Property Projects

Fair Value:RM 8.1279.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on PSP Energy Berhad ·

PSP Energy Bhd Posts Strong Q3 Growth on Higher Fuel Orders

Fair Value:RM 0.237.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1190 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative