Advertisement

- United States

- /

- Software

- /

- NYSE:PATH

Earnings Update: UiPath Inc. (NYSE:PATH) Just Reported And Analysts Are Trimming Their Forecasts

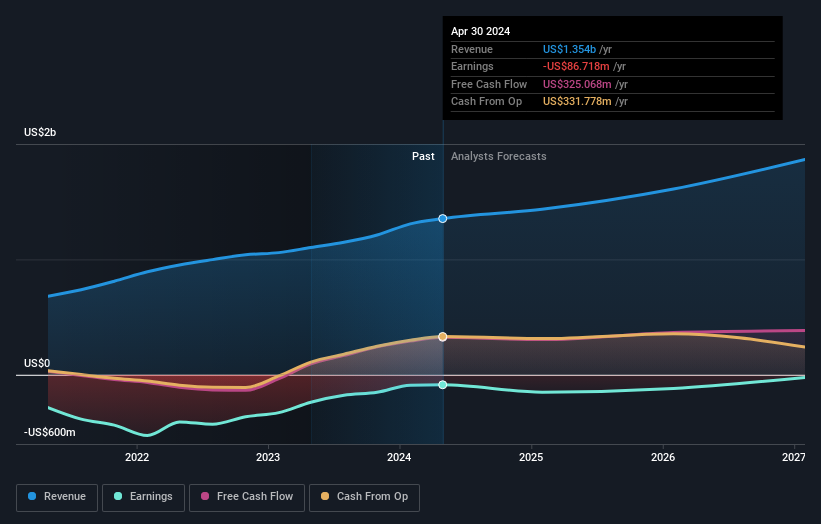

Shareholders in UiPath Inc. (NYSE:PATH) had a terrible week, as shares crashed 35% to US$12.26 in the week since its latest quarterly results. Revenues were in line with expectations, at US$335m, while statutory losses ballooned to US$0.05 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

View our latest analysis for UiPath

Following the latest results, UiPath's 22 analysts are now forecasting revenues of US$1.43b in 2025. This would be a credible 6.0% improvement in revenue compared to the last 12 months. Per-share losses are expected to explode, reaching US$0.26 per share. Yet prior to the latest earnings, the analysts had been forecasting revenues of US$1.56b and losses of US$0.083 per share in 2025. So it's pretty clear the analysts have mixed opinions on UiPath after this update; revenues were downgraded and per-share losses expected to increase.

The average price target fell 36% to US$17.82, implicitly signalling that lower earnings per share are a leading indicator for UiPath's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values UiPath at US$29.00 per share, while the most bearish prices it at US$13.00. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that UiPath's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 8.1% growth on an annualised basis. This is compared to a historical growth rate of 21% over the past three years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 13% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than UiPath.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at UiPath. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of UiPath's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on UiPath. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple UiPath analysts - going out to 2027, and you can see them free on our platform here.

You still need to take note of risks, for example - UiPath has 3 warning signs we think you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:PATH

UiPath

Provides an automation platform that offers a range of robotic process automation (RPA) solutions primarily in the United States, Romania, the United Kingdom, the Netherlands, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1156.8% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7720.5% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1909.9% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

ST

StoxEurope on KBC Group ·

KBC Group (ENXTBR:KBC) Valuation Deep-Dive: Why Dividend and Book Value Models Point in Opposite Directions.

Fair Value:€116.944.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentalFlow on Samsung Electronics ·

Samsung electronics, the DRAM bottleneck, leading the memory shortage wave?

Fair Value:₩500k47.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DI

divine_4y1uv on PRG Holdings Berhad ·

Dato’ Ng Yan Cheng Perjelaskan Pendahuluan RM89.55 Juta Bagi Menyokong Kewangan Syarikat

Fair Value:RM 0.361.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.2% undervalued

99 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.1% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.8% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0