- United States

- /

- Software

- /

- NYSE:ORCL

Oracle (NYSE:ORCL) Expands Cloud Options with Oracle Database@AWS Launch

Recent events have highlighted Oracle's (NYSE:ORCL) collaboration with Amazon Web Services, launching Oracle Database@AWS to enhance cloud database offerings. This development aligns with Oracle's ongoing commitment to innovation and cloud market expansion. Over the past quarter, Oracle's stock price surged by 87%, a movement that aligns with its strong earnings growth and strategic updates. The company's reported revenue increase and new AI offerings complemented these gains. Although the broader market saw modest fluctuations during this period, Oracle's initiatives notably contributed to its significant share price escalation. This reflects a robust response to its active role in cloud and AI advancements.

The recent collaboration between Oracle and Amazon Web Services in launching Oracle Database@AWS could have a meaningful impact on Oracle's future growth narrative. This partnership enhances Oracle's cloud services and supports its cloud market expansion, potentially increasing its revenue and earnings forecasts, particularly in the realms of AI demand and database migration. With Oracle's multi-cloud strategy, tapping into partnerships with leading cloud providers like AWS, Google, and Azure may fuel accelerated revenue growth and drive sustained demand for Oracle's cloud capabilities.

Over the last five years, Oracle's total shareholder return was 338.70%, reflecting a substantial increase in value. This contrasts with the one-year performance, where Oracle outperformed the US Software industry, showing greater growth than the industry's 17.9% return. This past performance underscores Oracle's capacity to generate shareholder value over both short and long-term periods.

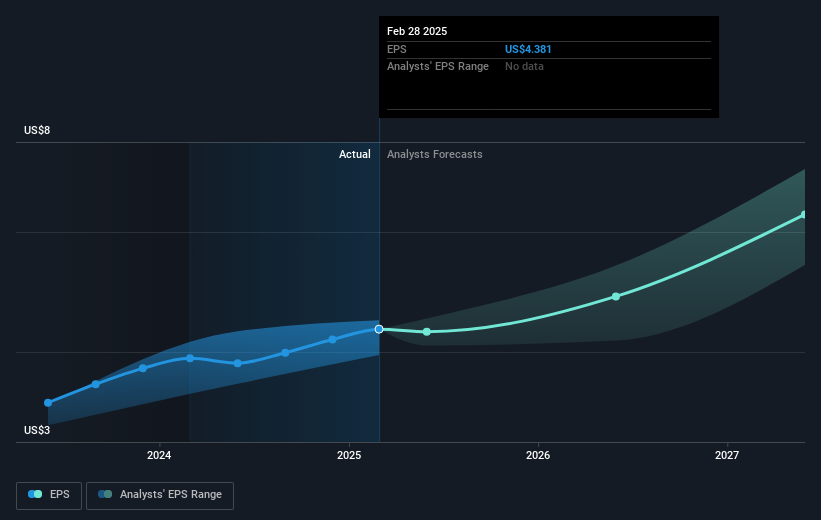

In terms of revenue and earnings, Oracle's strengthened cloud offerings could favorably impact analysts' projections, which assume a revenue growth of 17.6% annually over the next three years and increasing profit margins. Currently, at a share price of US$218.96, Oracle trades close to the consensus analyst price target of US$215.22. This proximity suggests relative alignment in views on Oracle's fair valuation, with the current price reflecting a marginal premium over the target. Investors should consider these dynamics as they analyze Oracle's position in a competitive and evolving tech landscape.

Evaluate Oracle's historical performance by accessing our past performance report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ORCL

Oracle

Offers products and services that address enterprise information technology environments worldwide.

Exceptional growth potential and good value.

Similar Companies

Market Insights

Weekly Picks

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Investment Analysis (May 2026)

Recently Updated Narratives

3REN Berhad Is Powering the Semiconductor Ecosystem and Smart Manufacturing

Cheeding: The Hidden Beneficiary of Malaysia’s Power Grid Expansion

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Popular Narratives

Investment Analysis (May 2026)

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Honeywell - The Demand-Side of the AI Infrastructure

Trending Discussion

It's wonderful. It has greatly helped me take informed decisions.