Advertisement

- United States

- /

- Software

- /

- NYSE:MODN

This Is Why Shareholders Will Hold Back On A Pay Rise For Model N, Inc.'s (NYSE:MODN) CEO This Year

The anaemic share price growth at Model N, Inc. (NYSE:MODN) over the past few years has probably not impressed shareholders and may be due to earnings not growing over that period. These concerns will be at the front of shareholders' minds as they go into the AGM coming up on 16 February 2023. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

See our latest analysis for Model N

Comparing Model N, Inc.'s CEO Compensation With The Industry

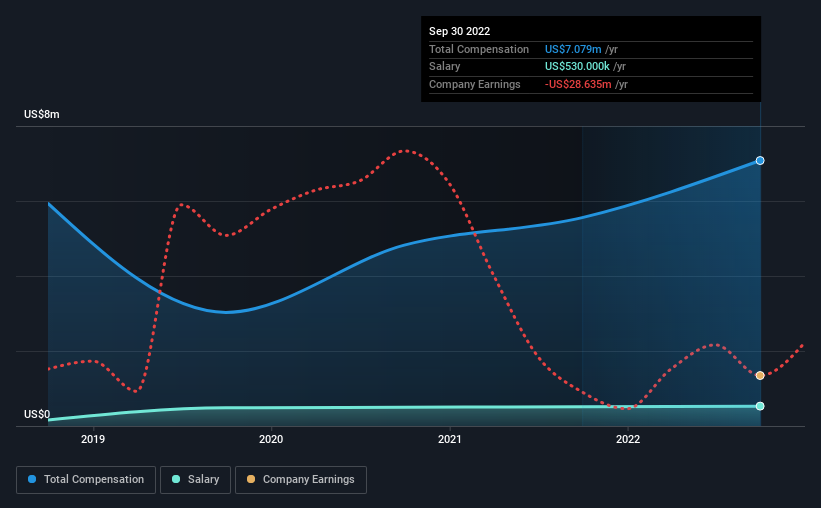

According to our data, Model N, Inc. has a market capitalization of US$1.3b, and paid its CEO total annual compensation worth US$7.1m over the year to September 2022. We note that's an increase of 27% above last year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$530k.

For comparison, other companies in the American Software industry with market capitalizations ranging between US$1.0b and US$3.2b had a median total CEO compensation of US$7.5m. So it looks like Model N compensates Jason Blessing in line with the median for the industry. Furthermore, Jason Blessing directly owns US$11m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | US$530k | US$515k | 7% |

| Other | US$6.5m | US$5.0m | 93% |

| Total Compensation | US$7.1m | US$5.6m | 100% |

On an industry level, around 9% of total compensation represents salary and 91% is other remuneration. Model N sets aside a smaller share of compensation for salary, in comparison to the overall industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Model N, Inc.'s Growth Numbers

Over the last three years, Model N, Inc. has shrunk its earnings per share by 19% per year. It achieved revenue growth of 12% over the last year.

Few shareholders would be pleased to read that EPS have declined. And while it's good to see some good revenue growth recently, the growth isn't really fast enough for us to put aside my concerns around EPS. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Model N, Inc. Been A Good Investment?

Model N, Inc. has not done too badly by shareholders, with a total return of 1.6%, over three years. It would be nice to see that metric improve in the future. As a result, investors in the company might be reluctant about agreeing to increase CEO pay in the future, before seeing an improvement on their returns.

In Summary...

The lacklustre share price returns along with the lack of earnings growth makes us think that a strong rebound in the share price may be difficult. Shareholders should make the most of the coming opportunity to question the board on key concerns they may have and revisit their investment thesis with regards to the company.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 3 warning signs for Model N that you should be aware of before investing.

Important note: Model N is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:MODN

Model N

Provides cloud revenue management solutions for life sciences and high-tech companies in the United States and internationally.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1941.1% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

44 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.5% undervalued

15 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30154.5% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

DA

danmad on Cobram Estate Olives ·

More than just olive oil on the shelf

Fair Value:AU$3.64.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Verisk Analytics ·

VRSK 05-2026

Fair Value:US$76.85149.8% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

44 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.6% undervalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5455.7% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3455.9% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative