- United States

- /

- Diversified Financial

- /

- NYSE:MA

Should Mastercard Incorporated (NYSE:MA) Be Your Next Stock Pick?

Building up an investment case requires looking at a stock holistically. Today I've chosen to put the spotlight on Mastercard Incorporated (NYSE:MA) due to its excellent fundamentals in more than one area. MA is a financially-sound company with a strong track record and a buoyant growth outlook. Below, I've touched on some key aspects you should know on a high level. If you're interested in understanding beyond my broad commentary, read the full report on Mastercard here.

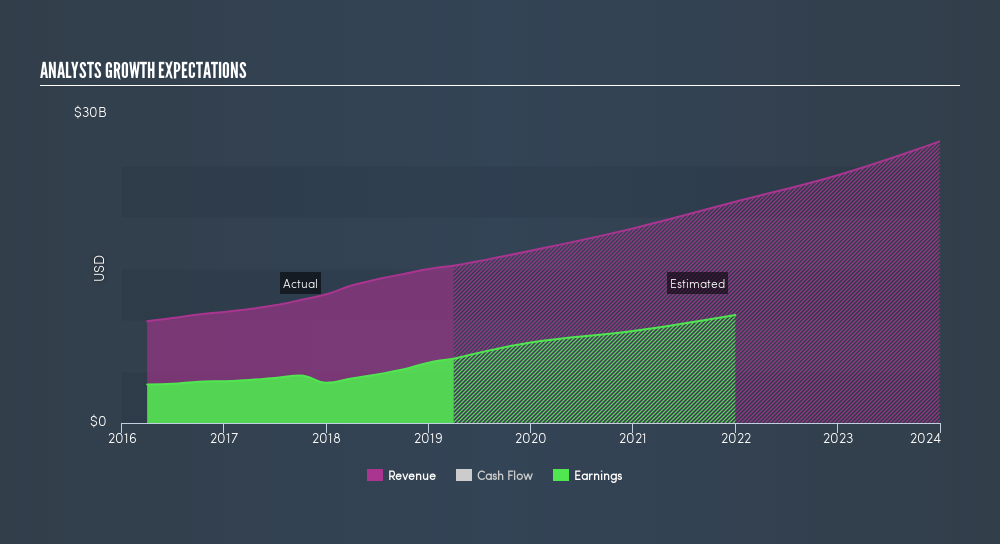

Solid track record with reasonable growth potential

MA’s cash-generating ability is outstanding, with analysts expecting its operating cash flows to flourish by 55% in the upcoming year. This is expected to flow down into an impressive return on equity of 107% over the next couple of years. In the previous year, MA has ramped up its bottom line by 44%, with its latest earnings level surpassing its average level over the last five years. In addition to beating its historical values, MA also outperformed its industry, which delivered a growth of 11%. This paints a buoyant picture for the company.

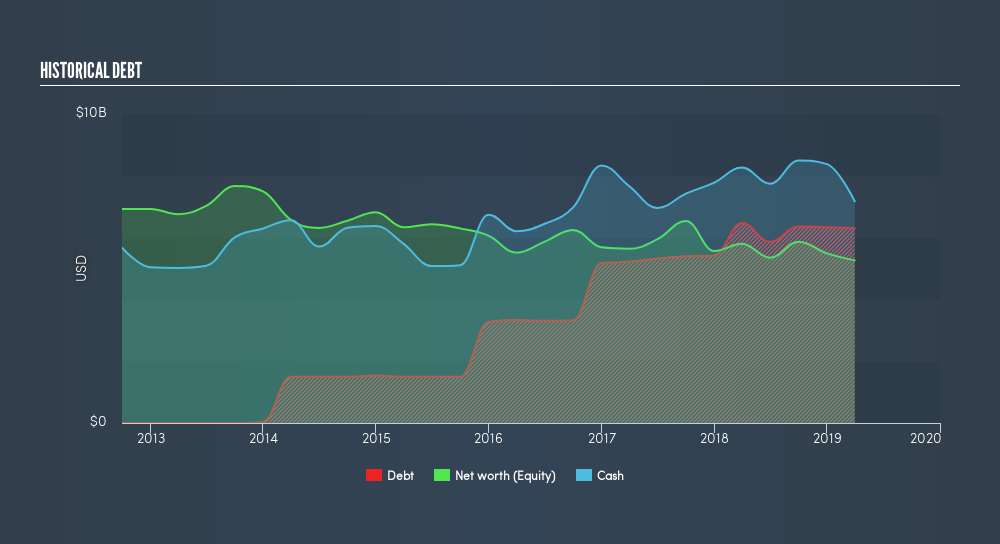

MA's strong financial health means that all of its upcoming liability payments are able to be met by its current cash and short-term investment holdings. This suggests prudent control over cash and cost by management, which is a crucial insight into the health of the company. MA appears to have made good use of debt, producing operating cash levels of 1.03x total debt in the prior year. This is a strong indication that debt is reasonably met with cash generated.

Next Steps:

For Mastercard, there are three relevant factors you should further examine:

- Valuation: What is MA worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether MA is currently mispriced by the market.

- Dividend Income vs Capital Gains: Does MA return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from MA as an investment.

- Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of MA? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:MA

Mastercard

A technology company, provides transaction processing and other payment-related products and services in the United States and internationally.

Solid track record with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion

Thanks for sharing these. They really help when I pick what dividend stocks to invest in