Advertisement

- United States

- /

- Software

- /

- NYSE:CRM

What Salesforce (CRM)'s Expanded Agentforce Adoption and Google Cloud Partnership Means For Shareholders

Reviewed by Sasha Jovanovic

- In April 2026, Unisys and Engine each announced expanded use of Salesforce’s Agentforce 360 platform, while Salesforce and Google Cloud agreed to deepen integrations that connect AI agents across Slack, Google Workspace, and core enterprise data without moving it.

- Together, these moves highlight how Salesforce is embedding “agentic” AI into large-scale field services, travel operations, and productivity tools, positioning its platform at the center of AI-driven enterprise workflows.

- Next, we’ll examine how this expanded Agentforce usage and the Google Cloud partnership influence Salesforce’s existing investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

Salesforce Investment Narrative Recap

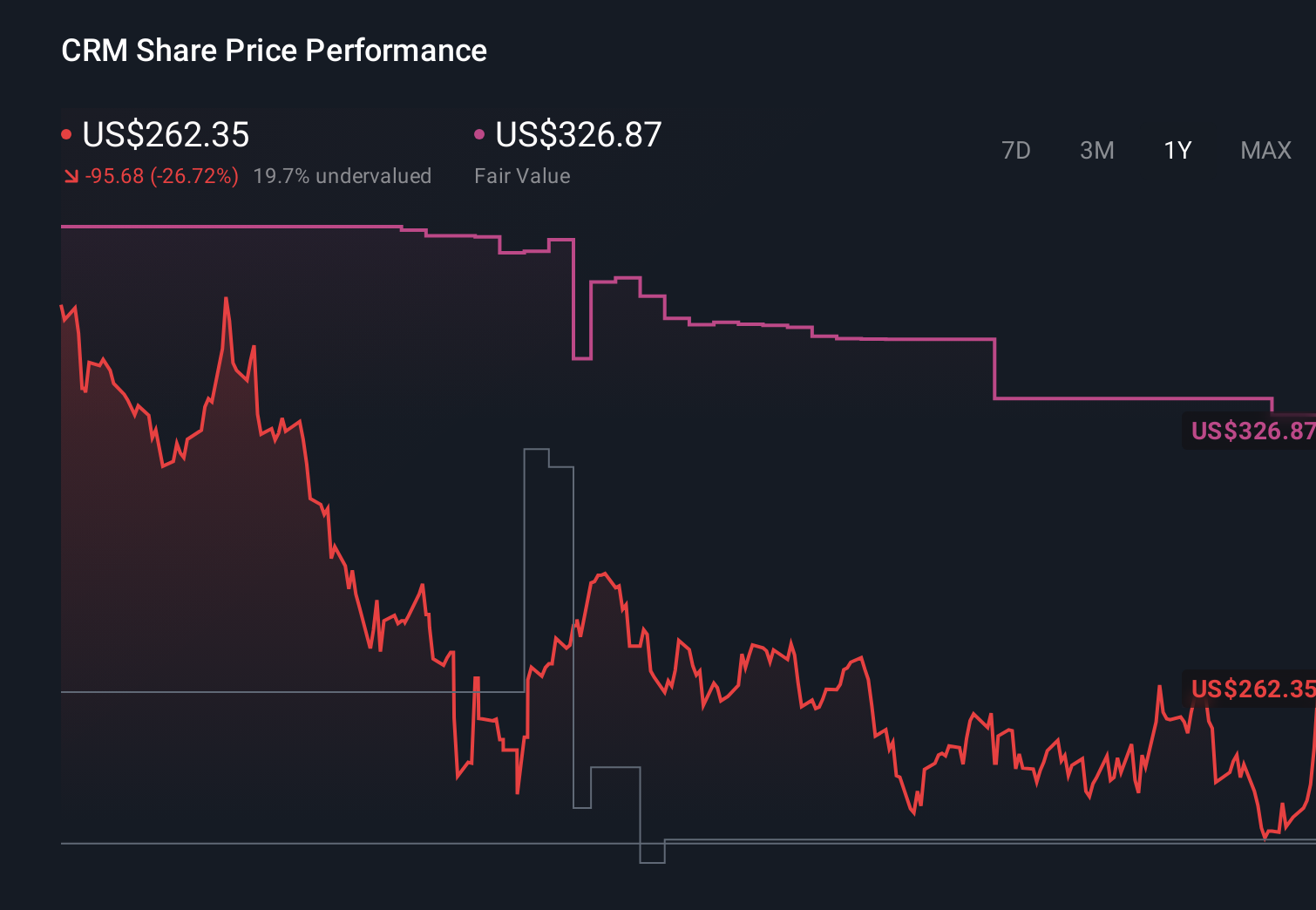

To own Salesforce today, you have to believe its pivot from traditional CRM to AI agents and Data Cloud can still support profitable growth, even as software valuations reset and AI competition intensifies. The latest Agentforce wins and the deeper Google Cloud tie up reinforce the near term catalyst of AI driven expansion within the existing customer base. They do not meaningfully reduce the key risk that AI native and bundled rivals could compress pricing power and slow growth.

Among the recent news, the expanded Salesforce and Google Cloud partnership looks most relevant. By letting AI agents work across Slack, Google Workspace and enterprise data in place, it directly supports the catalyst that Agentforce and Data 360 can increase contract sizes and stickiness. At the same time, it highlights the competitive risk: hyperscalers like Google are also central to the workflow, which could constrain Salesforce’s long term bargaining power if customer preferences shift.

Yet beneath this AI momentum, investors should stay alert to how growing AI native competition could still pressure Salesforce’s pricing power and long term margins...

Read the full narrative on Salesforce (it's free!)

Salesforce’s narrative projects $51.9 billion revenue and $10.3 billion earnings by 2028. This requires 9.6% yearly revenue growth and about a $3.6 billion earnings increase from $6.7 billion today.

Uncover how Salesforce's forecasts yield a $317.21 fair value, a 78% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were far more cautious, assuming Salesforce revenue of about US$52.5 billion and earnings of roughly US$9.7 billion by 2029, and seeing AI native rivals as a real threat, so it is worth weighing these more pessimistic views against the recent Agentforce and Google Cloud news before you decide which story you believe.

Explore 37 other fair value estimates on Salesforce - why the stock might be worth as much as 93% more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Salesforce research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Salesforce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Salesforce's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Find 54 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CRM

Salesforce

Provides customer relationship management technology services that connect companies and customers together in the United States, Europe, and the Asia Pacific.

Undervalued with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

61 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3219.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$273.4525.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative