- United States

- /

- Software

- /

- NYSE:CCRD

While institutions invested in CoreCard Corporation (NYSE:CCRD) benefited from last week's 15% gain, individual investors stood to gain the most

Key Insights

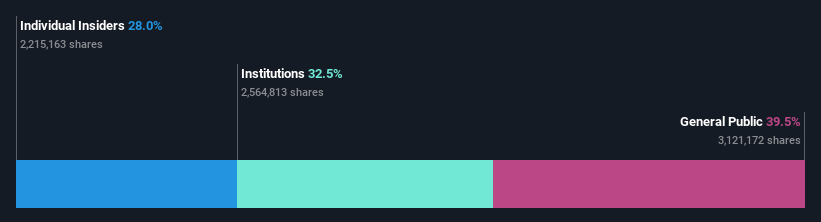

- Significant control over CoreCard by individual investors implies that the general public has more power to influence management and governance-related decisions

- A total of 9 investors have a majority stake in the company with 50% ownership

- Insiders own 28% of CoreCard

Every investor in CoreCard Corporation (NYSE:CCRD) should be aware of the most powerful shareholder groups. We can see that individual investors own the lion's share in the company with 40% ownership. That is, the group stands to benefit the most if the stock rises (or lose the most if there is a downturn).

Individual investors gained the most after market cap touched US$182m last week, while institutions who own 32% also benefitted.

Let's take a closer look to see what the different types of shareholders can tell us about CoreCard.

Check out our latest analysis for CoreCard

What Does The Institutional Ownership Tell Us About CoreCard?

Institutions typically measure themselves against a benchmark when reporting to their own investors, so they often become more enthusiastic about a stock once it's included in a major index. We would expect most companies to have some institutions on the register, especially if they are growing.

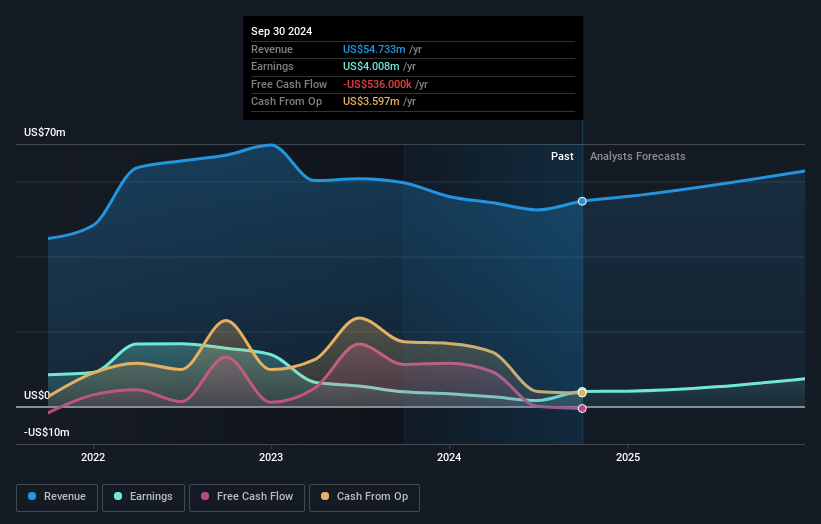

As you can see, institutional investors have a fair amount of stake in CoreCard. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. It is not uncommon to see a big share price drop if two large institutional investors try to sell out of a stock at the same time. So it is worth checking the past earnings trajectory of CoreCard, (below). Of course, keep in mind that there are other factors to consider, too.

CoreCard is not owned by hedge funds. Looking at our data, we can see that the largest shareholder is the CEO James Strange with 17% of shares outstanding. Clifford Burnstein is the second largest shareholder owning 11% of common stock, and Weitz Investment Management, Inc. holds about 6.5% of the company stock.

We also observed that the top 9 shareholders account for more than half of the share register, with a few smaller shareholders to balance the interests of the larger ones to a certain extent.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock's expected performance. There is some analyst coverage of the stock, but it could still become more well known, with time.

Insider Ownership Of CoreCard

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

It seems insiders own a significant proportion of CoreCard Corporation. Insiders own US$51m worth of shares in the US$182m company. It is great to see insiders so invested in the business. It might be worth checking if those insiders have been buying recently.

General Public Ownership

The general public, who are usually individual investors, hold a 40% stake in CoreCard. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. To that end, you should be aware of the 1 warning sign we've spotted with CoreCard .

Ultimately the future is most important. You can access this free report on analyst forecasts for the company.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CCRD

CoreCard

Provides technology solutions and processing services to the financial technology and services market in the United States, Europe, and the Middle East.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives