- United States

- /

- Software

- /

- NYSE:BB

BlackBerry Limited (NYSE:BB) is Showing a Lot of Potential but no Real Indications of Growth

BlackBerry Limited (NYSE:BB) is a US$6.5b Market Cap CyberSecurity company, which lately garnered a lot of attention in the retail investment space. With the earnings report coming out on the 22nd September, we thought to examine BB's growth potential, financial performance and stability.

There seems to be a large opportunity for BB to expand sales in the new Cyber Era, and EV industry. We will see just how much the company can grow within their main segments.

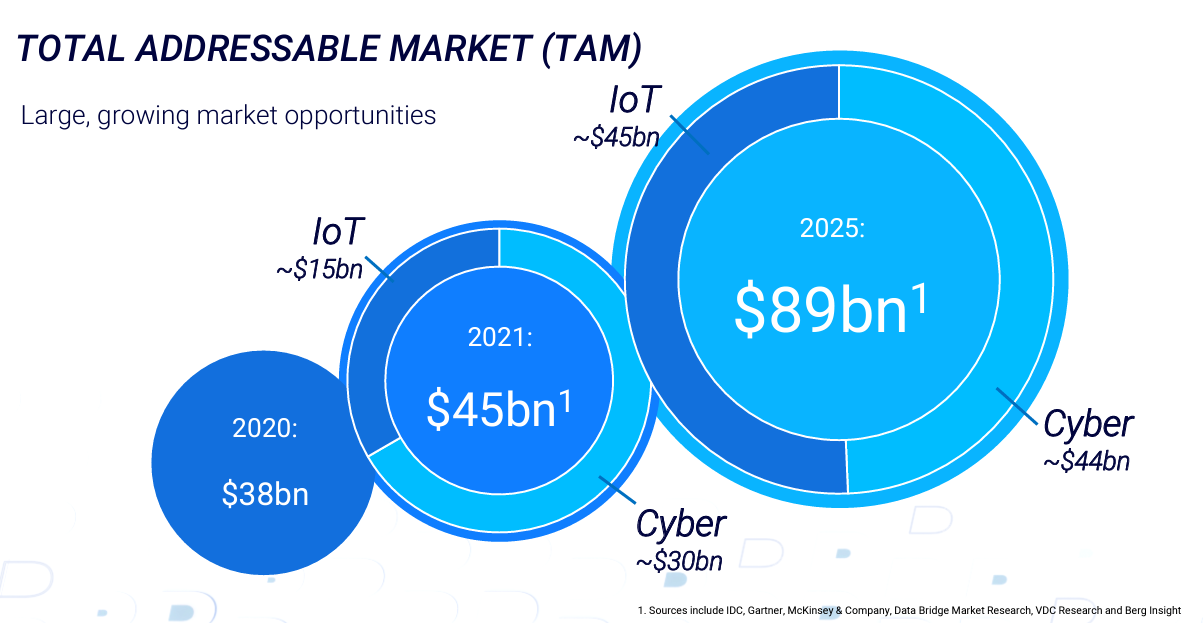

Total Addressable Market

The Company is now organized and managed as three operating segments: CyberSecurity, IoT, and Licensing and Other.

BlackBerry's largest segment is cybersecurity and comprises some 61.5% of last quarter's revenue. The company is also focused on the smaller IoT segment, which brought in 24.7%. This is important in the context of the total addressable market - which is simply the max dollar amount of revenues for the whole industry. The TAM for BB consists of both IoT and CyberSecurity, and in 2021 it totaled an estimated US$45b - of which BB only had around a 1% share.

Looking at the current numbers, it is great to see that BB is well positioned to grow within the TAM, and it also seems that their services will be even more in-demand in the future as the TAM is expected to grow around a 100% to US$89b.

View our latest analysis for BlackBerry

This leaves BB in a great position to prove its business model and scale income.

This is apparent in their vast portfolio of clients, especially in the electrical vehicle industry. BlackBerry also provides an operating system, collects sensor data, and provides platform services for most of the largest auto manufacturers. This gives investors a sense of where the company can expand, but should also be mindful that they are not there yet, and competition and in-house solutions can decrease the real opportunities for expansion.

In the picture below, we can see which services and clients is BB catering to:

With that being said, we can get a good sense of what analysts are expecting to see in the short term - which can help us get a better feeling before BlackBerry's Q2 Earnings Release on Sept. 22.

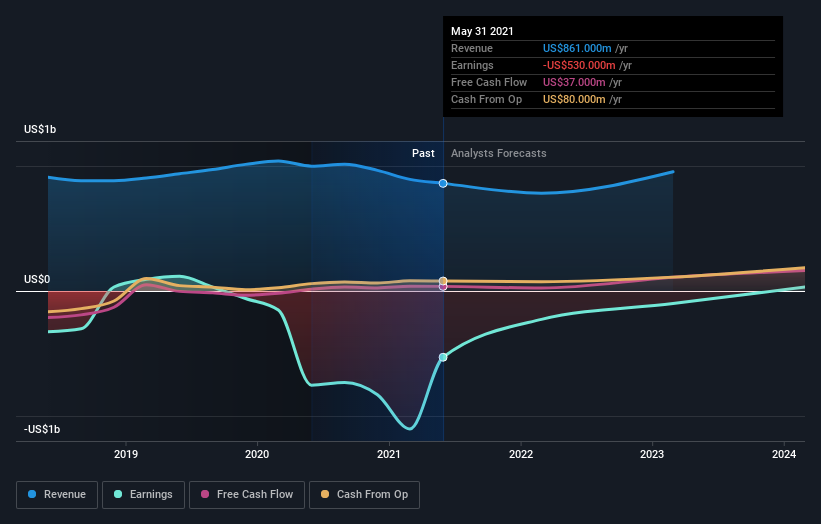

As we can see in the forecasts below, revenue is not expected to jump up anytime soon, but the company still has a fighting chance to secure new clients and slowly scale sales per client.

Investors should be aware that the company is not in any immediate financial distress. In fact, at current loss levels, BlackBerry has the cash capacity to finance operations for up to 3 more years. That should give the company plenty of time to iron out rough edges, develop winning services for clients, and if needed, pivot and consolidate. This calculation is made before interest and principal payments for BB's US$715m of debt - and while the company has been successfully reducing the debt load, it does increase the risk of solvency.

Additionally, our most recent data indicates that insiders own some shares in BlackBerry Limited. The insiders have a meaningful stake worth US$85m. Most would see this as a real positive. It is good to see this level of investment by insiders. You can check here to see if those insiders have been buying recently.

Key Takeaways

BlackBerry is not expected to deliver a huge surprise on growth this quarter, as the management has not shown signs of any product picking up sales momentum. With that being said, it is true that the sheer expected growth of the industry can deliver revenue growth. The total addressable market for BB is expected to increase by close to 100% in 2025, but that might be quite a risk for investors, and currently there are no particular developments of note for investors.

The company is financially stable, and has enough cash flows to finance up to 3 years of operation with the current expense structure. Keep in mind that this is rarely static and also that the company has a high level of debt, which you can further analyze HERE.

You should also be aware of the 2 warning signs we've spotted with BlackBerry .

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Valuation is complex, but we're here to simplify it.

Discover if BlackBerry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:BB

BlackBerry

Provides intelligent security software and services to enterprises and governments worldwide.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Community Narratives