Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ZM

Zoom (NASDAQ:ZM) Managed to Perform Within Expectations, but Investors May Fear Some Significant Risk Factors

Zoom Video Communications, Inc. (NASDAQ:ZM) just released the latest quarterly report, and some analysts have been promoting this as a validation of the business model of zoom. Today we will take a look at the performance of Zoom and check what this may mean for the value of the stock.

Quarterly Highlights

- Q1 Revenue reached US$1.074b, largely in-line with analysts' expectations of US$1.07b

- This puts the last 12 months revenue at US$4.217b as quarterly revenue grew 12%

- Adjusted EPS was US$1.03 vs US$0.87 expected

- Non-Gaap operating income was US$400m, about the same as a year ago

- Net Cash from operations was US$526.2m vs US$533.3 in the prior year

In order to better understand what is happening with the business, we can look at key customer metrics.

Zoom finished the first quarter with about 200k enterprise customers, up some 24% from a year ago. The company had 2.916 customers contributing more than US$100k in revenue for the last 12 months.

This shows that the company has a diversified customer base and is not relying on a few major customers to deliver revenues.

Considering the outlook, the company estimates a decline in non-Gaap operating income for the second quarter of about 9.3%, to an estimated US$362.5m Q2 operating income.

For the full year, revenue is expected to come around US$4.54b, a projected increase of 10.7% from 2021.

It is clear that the company is losing the 2021 tailwind, and now has to focus on retaining customers in a different landscape, as well as attracting new customers.

In order to get a better sense of what this means for investors, we can pair the results with what our DCF valuation model.

View our latest analysis for Zoom Video Communications

Value Estimate

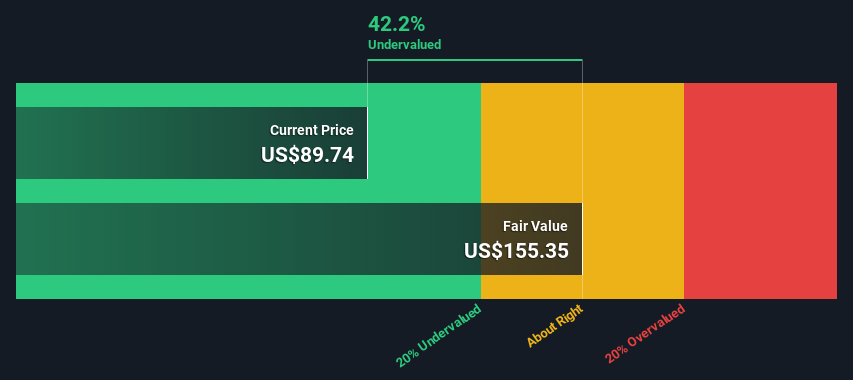

Our 2-stage discounted cash flow model yielded an intrinsic value of the company of US$46b or US$155 per share. Relative to the last close price, the stock is trading at an estimated 42% discount.

Zoom already has positive free cash flows, giving us the following valuation results:

Present Value of 10-year Cash Flow (PVCF) = US$13b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= US$60b÷ (1 + 6.2%)10= US$33b

If you want to get into the details, you can see how we did our Zoom valuation HERE.

Risk Factors

It seems that the company is significantly undervalued, even accounting for a 20% margin of error. Investors should also ask themselves what may be keeping the price down. In order to address this, we need to discuss some risk factors.

The first and most important risk factor is the current competition, with Microsoft Teams being the obvious example. It may be hard for Zoom to retain customers who are using Microsoft 365, since their Teams tools fits easily in the ecosystem. Zoom will need to build up significant advantages in order to convince customers to switch. Microsoft is currently holding a large portion of enterprise customers, and it will be hard for Zoom to take away that share based solely on price competition.

The second competitor is Google Meet, which is a relatively cheap and fast alternative to both teams and zoom. Meet caters mostly to individuals and small businesses that have a Gmail account or utilize the G-suite app family in their lives. The benefit of meet, is that it is quite easy to launch, but lacks some advanced features.

Another risk factor is future innovation. CRM companies, large enterprises, and even small developers are constantly constructing their own video conferencing tools that may bring down the profit margins of Zoom and/or take portions of their market share. Zoom may address this by catering to and being a market leader in a specific customer segment, but this has yet to be established.

As we can see, the company has some risk factors, which may explain why investors are still not at ease with investing in the business.

Conclusion & Looking Ahead:

Zoom managed to perform largely in-line with expectations, which may bring a sigh of relief to investors who expected lower results. The company seems to be undervalued on an intrinsic basis, but investors are not yet convinced that they can account for a significant portion of the risks.

Non-Gaap operating earnings are expected to slightly decline in the future, and management has to provide a strong path to growth and profitability in order to keep the interest of investors.

In order to get a better understanding of Zoom Video Communications, we've put together three additional items you should consider:

- Fundamental Risks: We've identified 2 warning signs with Zoom Video Communications (at least 1 which doesn't sit too well with us) , and understanding these should be part of your investment process.

- Future Earnings: How does ZM's growth rate compare to its peers and the wider market? Dig deeper into the analyst consensus number for the upcoming years by interacting with our free analyst growth expectation chart.

- Other High Quality Alternatives: Do you like a good all-rounder? Explore our interactive list of high quality stocks to get an idea of what else is out there you may be missing!

Valuation is complex, but we're here to simplify it.

Discover if Zoom Communications might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:ZM

Zoom Communications

Provides an Artificial Intelligence-first work platform for human connection in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

56 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

56 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative