Advertisement

- United States

- /

- Healthtech

- /

- NYSE:DOCS

3 Growth Companies With High Insider Ownership And Up To 17% Revenue Growth

Simply Wall St

Reviewed by Simply Wall St

As the U.S. stock market navigates a challenging period marked by mixed performances and economic uncertainties, investors are keenly observing growth companies with solid fundamentals to weather the storm. In this context, stocks with high insider ownership often stand out as they can indicate strong confidence from those closest to the company's operations, potentially offering resilience and opportunities for revenue growth even amidst broader market volatility.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 25.7% |

| Duolingo (NasdaqGS:DUOL) | 14.4% | 37.1% |

| Hims & Hers Health (NYSE:HIMS) | 13.2% | 21.9% |

| Corcept Therapeutics (NasdaqCM:CORT) | 11.7% | 36.7% |

| Astera Labs (NasdaqGS:ALAB) | 15.9% | 61.3% |

| BBB Foods (NYSE:TBBB) | 16.5% | 41.1% |

| Clene (NasdaqCM:CLNN) | 20.7% | 59.1% |

| Upstart Holdings (NasdaqGS:UPST) | 12.7% | 100.1% |

| Enovix (NasdaqGS:ENVX) | 12.2% | 56.5% |

| Credit Acceptance (NasdaqGS:CACC) | 14.4% | 33.6% |

We're going to check out a few of the best picks from our screener tool.

AvePoint (NasdaqGS:AVPT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: AvePoint, Inc. offers a cloud-native data management software platform across various regions including North America, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of approximately $2.96 billion.

Operations: The company's revenue segment is primarily derived from its Software & Programming division, which generated $330.48 million.

Insider Ownership: 34.7%

Revenue Growth Forecast: 17.6% p.a.

AvePoint is actively seeking acquisitions to broaden its market presence and strengthen its SaaS business, aligning with recent revenue guidance for 2025 projecting US$380 million to US$388 million. Despite a net loss of US$29.09 million in 2024, the company anticipates becoming profitable within three years, with earnings expected to grow nearly 96% annually. Recent product enhancements focus on data security across multi-cloud environments, supporting growth and operational efficiency for managed service providers.

- Dive into the specifics of AvePoint here with our thorough growth forecast report.

- Insights from our recent valuation report point to the potential overvaluation of AvePoint shares in the market.

Workday (NasdaqGS:WDAY)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Workday, Inc. offers enterprise cloud applications globally and has a market cap of approximately $65.04 billion.

Operations: The company generates revenue primarily from its cloud applications segment, which accounts for $8.45 billion.

Insider Ownership: 19.7%

Revenue Growth Forecast: 11.5% p.a.

Workday's growth trajectory is supported by strong revenue forecasts, with expected annual growth of 11.5%, outpacing the US market average. Despite a decline in profit margins from last year, analysts agree on a potential stock price increase of 28.5%. Recent strategic partnerships with firms like Randstad and Prudential Financial enhance its AI-driven solutions, aiming to streamline talent acquisition and employee benefits management. These initiatives underline Workday's commitment to innovation amidst evolving market demands.

- Click here to discover the nuances of Workday with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential undervaluation of Workday shares in the market.

Doximity (NYSE:DOCS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Doximity, Inc. operates a cloud-based digital platform for medical professionals in the United States and has a market cap of approximately $11.89 billion.

Operations: The company's revenue primarily comes from its healthcare software segment, generating $550.17 million.

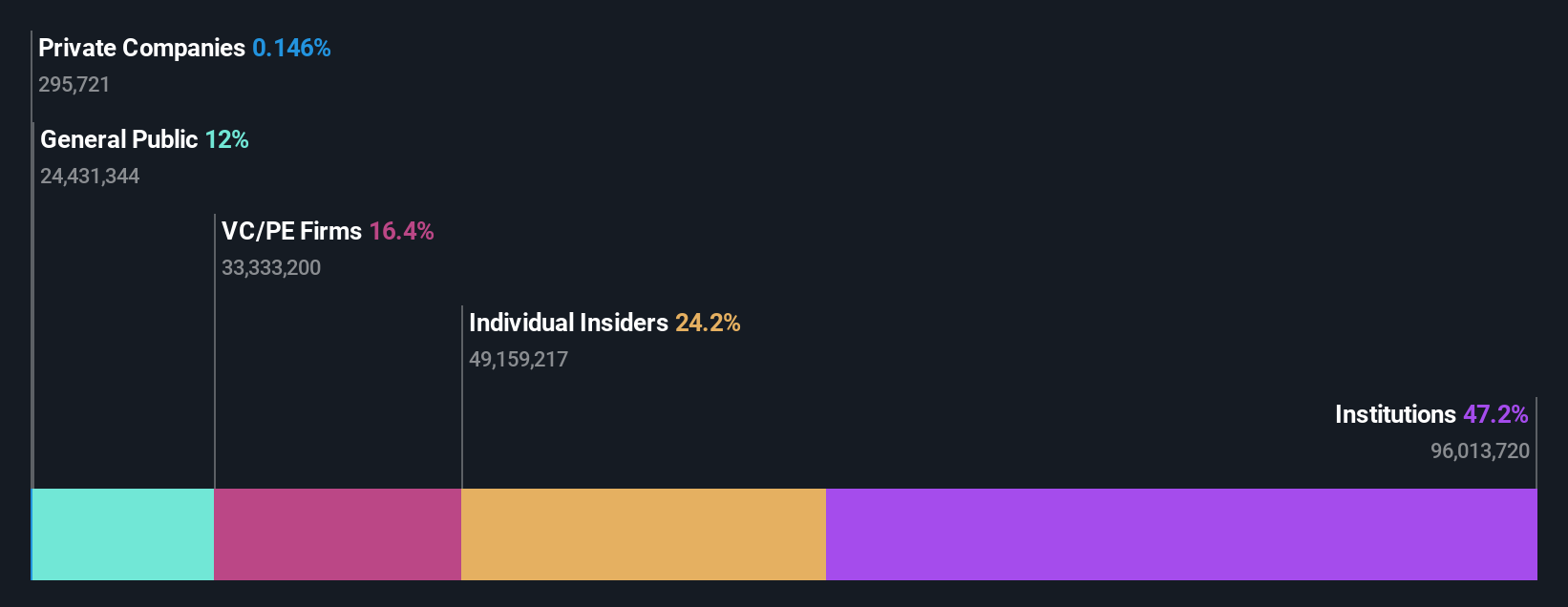

Insider Ownership: 27.2%

Revenue Growth Forecast: 11.2% p.a.

Doximity's insider ownership is complemented by solid financial performance, with recent earnings showing significant growth. The company reported a net income increase to US$75.2 million in Q3 2024 from US$47.96 million the previous year, alongside revenue growth to US$168.6 million. Despite high share price volatility and some insider selling, Doximity's earnings are forecasted to grow at 14.1% annually, outpacing the broader US market expectations of 13.9%.

- Navigate through the intricacies of Doximity with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Doximity's shares may be trading at a premium.

Make It Happen

- Investigate our full lineup of 206 Fast Growing US Companies With High Insider Ownership right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DOCS

Doximity

Operates as a digital platform for medical professionals in the United States.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor