Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

Is Rising Margin Pressure at Varonis (VRNS) Reframing Its SaaS Investment Narrative and Profit Ambitions?

Reviewed by Sasha Jovanovic

- In recent commentary, Varonis Systems was reported to be facing slower-than-typical software sales growth, rising operating costs, and plans to ramp up investment, all of which occurred before today and have raised questions about near-term profitability and cash generation.

- This combination of moderating growth and mounting margin pressure underscores the tension between funding product and SaaS expansion and preserving financial flexibility in a competitive data security market.

- Next, we’ll examine how this increased margin pressure could reshape Varonis Systems’ investment narrative and its longer-term earnings ambitions.

AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Varonis Systems Investment Narrative Recap

To own Varonis today, you need to believe its data security platform and SaaS shift can eventually translate solid revenue growth into sustainable free cash flow, despite ongoing losses. The latest update on slower sales growth and rising costs appears to intensify, rather than change, the main near term catalyst and risk: can management convert expanding SaaS ARR into better margins before investor patience wears thin on profitability and cash burn?

The launch of Varonis Atlas, an AI security platform announced in March 2026, is especially relevant here. It highlights how Varonis is leaning into AI driven data and application security just as enterprises grapple with Copilot, LLMs, and cloud data risks. For investors, Atlas could either reinforce the growth and product adoption catalyst or deepen the margin squeeze if higher investment is not matched by stronger customer uptake.

Yet beneath the promise of AI and SaaS growth, there is a key risk around margin pressure and cash generation that investors should be aware of...

Read the full narrative on Varonis Systems (it's free!)

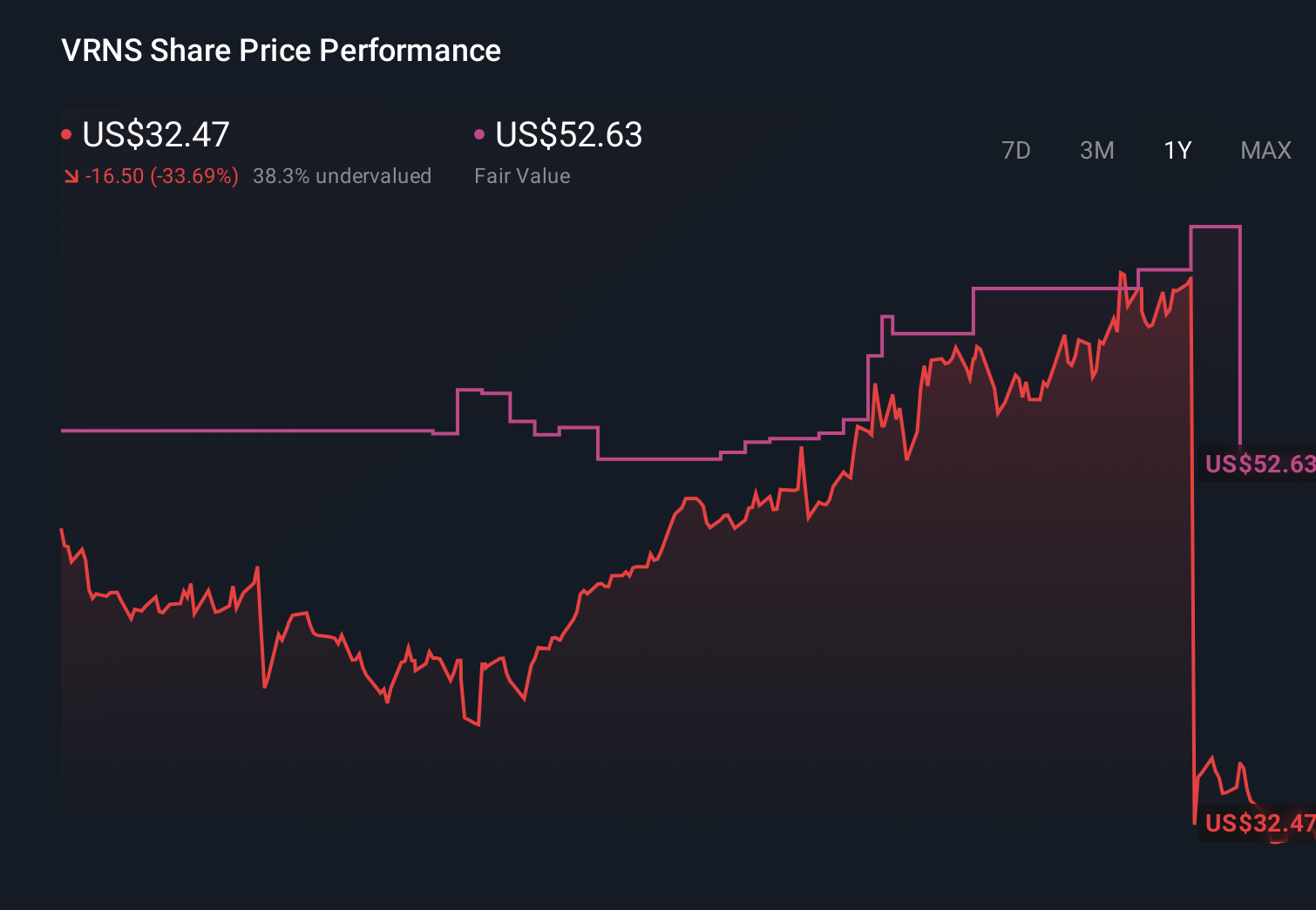

Varonis Systems' narrative projects $992.3 million revenue and $112.7 million earnings by 2029. This requires 16.8% yearly revenue growth and a $242.0 million earnings increase from -$129.3 million today.

Uncover how Varonis Systems' forecasts yield a $33.90 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were assuming roughly 18.5 percent annual revenue growth and US$1.0 billion of revenue by 2028, which sits in sharp contrast to concerns about a choppy SaaS transition and on premises renewal risk, reminding you that views on Varonis can differ widely and that these narratives may need to be revisited as new information comes through.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth over 3x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Varonis Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 61 companies with promising cash flow potential yet trading below their fair value.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

70 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

18 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on Cisco Systems ·

Defensive AI infrastructure

Fair Value:US$110.563.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Kaspi.kz ·

Kaspi.kz represents a high-quality, high-growth fintech/e-commerce platform

Fair Value:US$99.027.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on FTAI Aviation ·

Attractive if you believe in prolonged engine shortages and slow fleet renewal

Fair Value:US$225.056.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1186 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative