Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

Is It Time To Reconsider Varonis Systems (VRNS) After Prolonged Share Price Weakness

Reviewed by Bailey Pemberton

- If you are looking at Varonis Systems and wondering whether the current share price reflects its true worth, this article will walk through what the numbers are saying about value today.

- The stock last closed at US$24.18, with returns of 1.5% over 7 days, a 7.9% decline over 30 days, a 24.5% decline year to date, and a 38.3% decline over 1 year, alongside a 6.3% decline over 3 years and a 54.6% decline over 5 years.

- Recent attention on Varonis has been shaped by ongoing interest in cybersecurity and data protection, as investors reassess how these themes fit into their portfolios. This backdrop helps frame the recent share price moves and sets up an important question around what is already priced in.

- On our valuation checklist, Varonis scores 3 out of 6 for potential undervaluation, as shown in its valuation score of 3. We will walk through how traditional valuation approaches assess the stock and then finish with a broader way to think about its value beyond a single score.

Find out why Varonis Systems's -38.3% return over the last year is lagging behind its peers.

Approach 1: Varonis Systems Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model looks at the cash Varonis Systems is expected to generate in the future and then discounts those projected cash flows back to today to estimate what the business might be worth per share.

For Varonis, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $138.3 million. Analyst estimates and extrapolated figures suggest projected Free Cash Flow of $304.4 million by 2030, with a series of annual projections between 2026 and 2035 that are discounted back to the present using Simply Wall St’s assumptions.

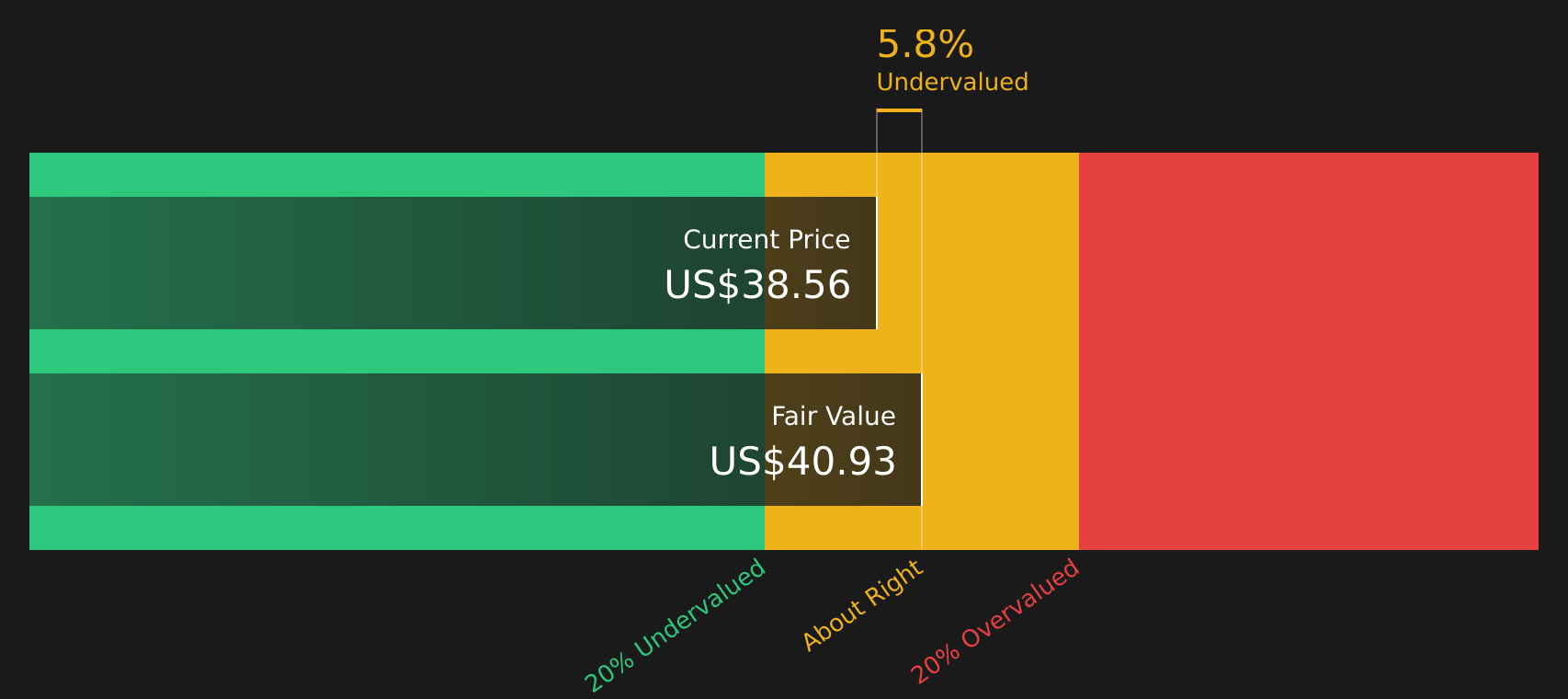

Putting all those discounted cash flows together, the model arrives at an estimated intrinsic value of about $46.62 per share. Compared with the recent share price of $24.18, this implies the stock is trading at a 48.1% discount to that DCF estimate. This points to potential undervaluation based on this method alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Varonis Systems is undervalued by 48.1%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Approach 2: Varonis Systems Price vs Sales

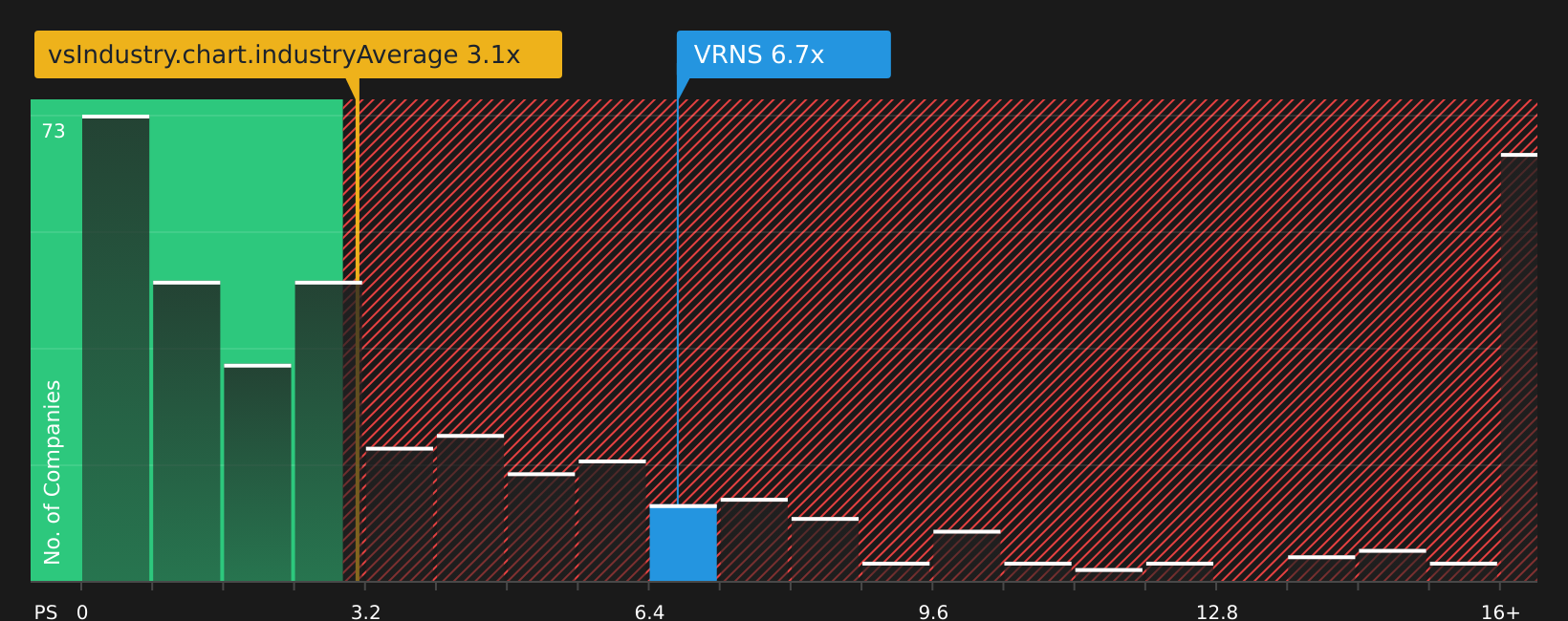

The Price to Sales, or P/S, ratio is often a useful way to look at software businesses, especially when earnings are limited or volatile, because it compares the value the market places on the company to the revenue it generates.

In general, higher growth expectations and lower perceived risk can support a higher P/S ratio, while slower growth or higher risk usually point to a lower, more conservative multiple. So what counts as “normal” depends on what investors believe about a company’s revenue potential and stability.

Varonis Systems currently trades on a P/S ratio of about 4.55x. This sits above the Software industry average of 3.57x and also above the peer average of 3.02x. Simply Wall St’s proprietary “Fair Ratio” for Varonis, which estimates an appropriate P/S multiple given factors such as earnings growth, profit margin, industry, market cap and risk profile, is 4.60x. Because the Fair Ratio is tailored to the company’s specific characteristics, it can be more informative than a simple comparison with broad industry or peer averages.

With an actual P/S of 4.55x versus a Fair Ratio of 4.60x, Varonis Systems looks priced at roughly the level Simply Wall St’s model would expect.

Result: ABOUT RIGHT

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 19 top founder-led companies.

Upgrade Your Decision Making: Choose your Varonis Systems Narrative

Earlier we mentioned that there is an even better way to think about valuation. On Simply Wall St’s Community page you can use Narratives, where you set your own story for Varonis Systems, link that story to specific forecasts for revenue, earnings and margins, and instantly see a Fair Value to compare with the current price. All of this then updates automatically when fresh data like news or earnings arrives. For example, one investor might build a bullish Varonis Narrative aligned with a Fair Value near US$62.0 that assumes faster revenue growth, higher profit margins and a P/E around 86.1x. Another might create a more cautious Narrative closer to US$40.0 with lower margin assumptions and a P/E around 216.3x. The platform keeps both views visible so you can decide which story, and which Fair Value, best fits your own expectations.

Do you think there's more to the story for Varonis Systems? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Excellent balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.167.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Lagenda Properties Berhad ·

Lagenda Continues To Offer Earnings Visibility Backed By Strong Sales Pipeline

Fair Value:RM 2.0330.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3223.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative