Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

Does Varonis Systems (NASDAQ:VRNS) Have A Healthy Balance Sheet?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Varonis Systems, Inc. (NASDAQ:VRNS) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out the opportunities and risks within the US Software industry.

What Is Varonis Systems's Net Debt?

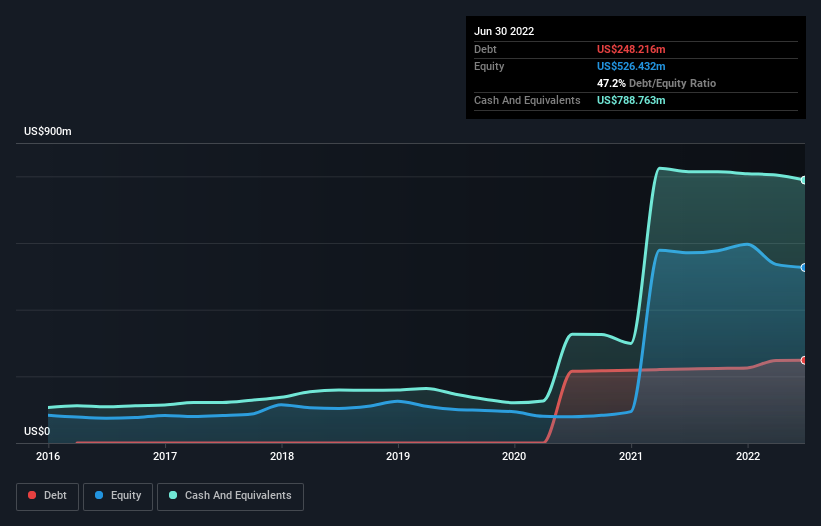

The image below, which you can click on for greater detail, shows that at June 2022 Varonis Systems had debt of US$248.2m, up from US$221.9m in one year. But it also has US$788.8m in cash to offset that, meaning it has US$540.5m net cash.

How Healthy Is Varonis Systems' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Varonis Systems had liabilities of US$208.9m due within 12 months and liabilities of US$316.9m due beyond that. On the other hand, it had cash of US$788.8m and US$83.9m worth of receivables due within a year. So it can boast US$346.8m more liquid assets than total liabilities.

This short term liquidity is a sign that Varonis Systems could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Varonis Systems has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Varonis Systems's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Varonis Systems wasn't profitable at an EBIT level, but managed to grow its revenue by 30%, to US$435m. With any luck the company will be able to grow its way to profitability.

So How Risky Is Varonis Systems?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Varonis Systems had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$8.4m and booked a US$133m accounting loss. While this does make the company a bit risky, it's important to remember it has net cash of US$540.5m. That kitty means the company can keep spending for growth for at least two years, at current rates. Varonis Systems's revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. By investing before those profits, shareholders take on more risk in the hope of bigger rewards. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Varonis Systems you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5368.6% undervalued

97 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k9.6% overvalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

23 likesusers have liked this narrative

SU

superbullll on Cheniere Energy ·

Cheniere Energy (LNG) — The Toll Road That Geopolitics Just Made More Valuable

Fair Value:US$320.9410.5% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

SA

Salman2415 on GNG Electronics ·

Strong execution in a growing category, but long‑term value hinges on cash‑flow discipline

Fair Value:₹135.87175.4% overvalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on McDonald's ·

McDonald’s (MCD): The "Digital Golden Arches" and the Pivot to Value

Fair Value:US$343.2810.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Lam Research ·

Lam Research (LRCX): The "AI Foundry" Backbone and the Memory Supercycle

Fair Value:US$274.915.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on SolarEdge Technologies ·

SolarEdge Technologies (SEDG): The "Solar Resurrection" and the AI Pivot

Fair Value:US$3437.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

56 followersusers have followed this narrative

3 commentsusers have commented on this narrative

30 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9825.5% undervalued

47 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0