Advertisement

- United States

- /

- Software

- /

- NasdaqGS:VRNS

A Look At Varonis Systems (VRNS) Valuation As Weaker Fundamentals Draw Fresh Attention

Why Varonis Systems Stock Is Back in Focus

Varonis Systems (VRNS) is back on investors’ radar after recent commentary highlighted weaker fundamentals, including revenue growth lagging software peers and operating margins coming under pressure as expenses took a larger share of sales.

See our latest analysis for Varonis Systems.

The recent commentary on weaker fundamentals comes after a sharp 44.2% 90 day share price decline and a 21.4% 1 year total shareholder return loss, even as the year to date share price return of 8.6% suggests some early rebuilding of momentum.

If this kind of rebound after a pullback has your attention, it could be a good moment to widen your search and check out high growth tech and AI stocks.

With the share price under pressure, revenue growth trailing software peers and a US$114.5 million loss, yet a 45% gap to one intrinsic value estimate, are you looking at a mispriced rebound story, or a market already discounting future growth?

Most Popular Narrative: 29.9% Undervalued

With Varonis Systems last closing at $34.79 versus a narrative fair value of $49.60, the most widely followed view frames the stock as materially mispriced, anchored on a long term SaaS and data security thesis.

Investments in R&D and expansion of platform capabilities (e.g., next-gen database security, MDDR, AI-driven integrations with Microsoft Copilot and OpenAI, cross-platform coverage for AWS, Azure, Snowflake, Databricks, etc.) are increasing customer wallet share and accelerating new logo acquisition, strongly supporting consistent top-line and free cash flow growth.

Want to see what kind of revenue trajectory, margin shift, and future earnings multiple are baked into that valuation gap? The full narrative spells out the growth runway, the profitability bridge, and the expectations behind those long term cash flow assumptions.

Result: Fair Value of $49.60 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to weigh weaker on-premises renewals and rising competitive pressure in data security, which could challenge the SaaS transition story.

Find out about the key risks to this Varonis Systems narrative.

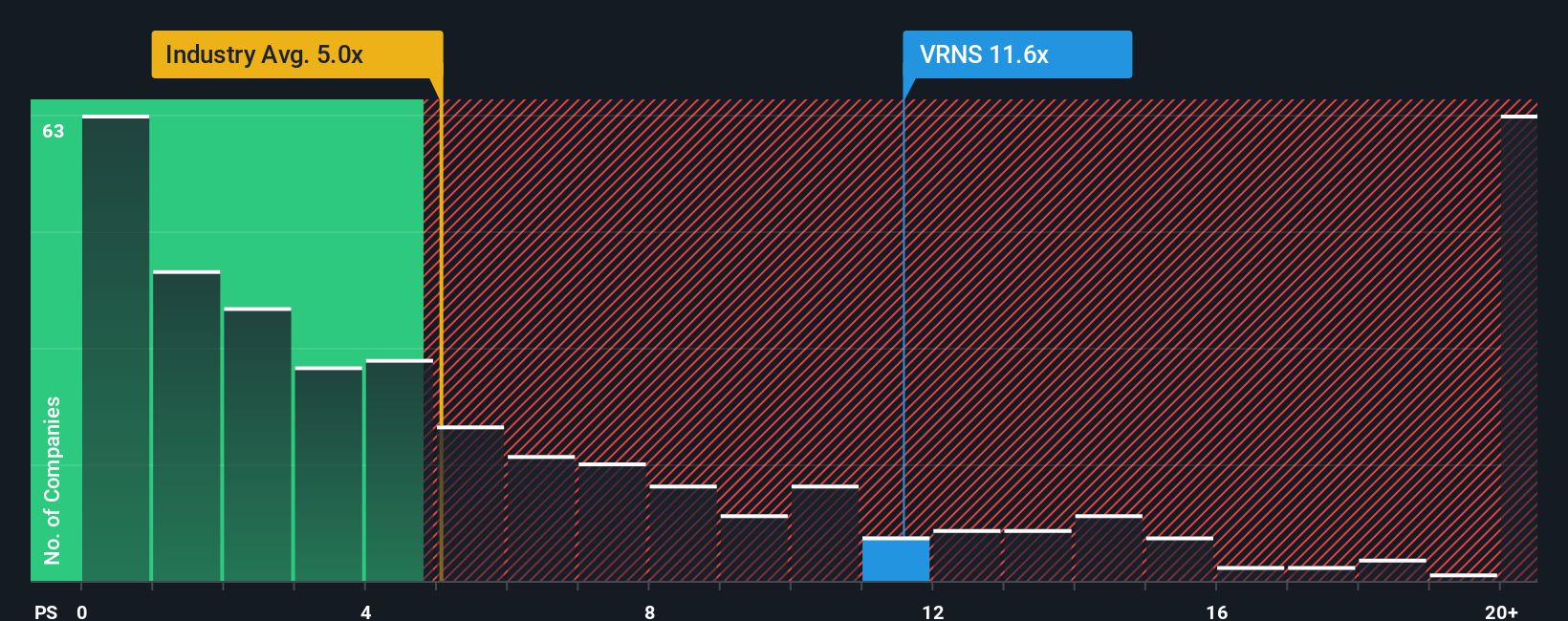

Another View: Multiples Paint A Tougher Picture

The narrative fair value and our cash flow work point to upside, but the current P/S ratio of 6.7x tells a different story. It sits above the US Software industry at 4.5x, above peers at 4.8x, and above a fair ratio of 5.9x. This signals valuation risk if sentiment cools.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Varonis Systems Narrative

If you see the numbers differently or would rather test your own assumptions directly in the model, you can build a personalised view in minutes with Do it your way.

A great starting point for your Varonis Systems research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Varonis has you thinking more broadly about opportunities, do not stop here. Use the screener to quickly surface other ideas that fit what you are looking for.

- Spot potential value opportunities early by scanning these 873 undervalued stocks based on cash flows that currently trade at prices below their estimated cash flow worth.

- Zero in on future tech themes by checking out these 24 AI penny stocks that are directly connected to artificial intelligence growth stories.

- Add some income ideas to your watchlist with these 12 dividend stocks with yields > 3% offering yields above 3% and a focus on shareholder payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VRNS

Varonis Systems

Provides software products and services that continuously discover and classify critical data, remediate exposures, and detect advanced threats with AI-powered technology in North America, Europe, APAC, and rest of worlds.

Excellent balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AN

Anthony_Lee on Geohan Corporation Berhad ·

Geohan's Growth Outlook Brightens on Expanding Order Book and Easing Cost Pressures

Fair Value:RM 0.7461.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on CSL ·

Strong buy. World-leading healthcare company with steady growth

Fair Value:AU$143.1519.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

13 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative