Advertisement

- United States

- /

- Software

- /

- NasdaqGS:TEAM

Is It Time To Revisit Atlassian After Its Volatile 2025 Share Price Reset?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether Atlassian is finally trading at a price that makes sense, or if the market is still overreacting, you are not alone. That is exactly what we are going to unpack here.

- After a choppy run where the stock is up 5.9% over the last week but still down 5.0% over the past month and 35.3% year to date, many investors are asking whether this reset is a potential buying opportunity or a warning sign.

- Recent headlines have focused on Atlassian doubling down on cloud migration, rolling out new AI driven features across Jira and Confluence, and tightening its ecosystem through deeper integrations with partners like Slack and Microsoft Teams. These strategic moves help explain why sentiment has been volatile, as the market weighs long term growth potential against execution risk and competitive pressure.

- Right now, Atlassian scores a 4/6 valuation check score. This suggests it looks undervalued on several metrics but not across the board. Next, we will walk through those different valuation approaches while hinting at an even more useful way to think about value by the end of the article.

Find out why Atlassian's -43.4% return over the last year is lagging behind its peers.

Approach 1: Atlassian Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and discounting those cash flows back to today, using an appropriate required rate of return.

For Atlassian, the latest twelve month Free Cash Flow is about $1.47 billion, and analysts expect this to rise steadily over time. Based on analyst estimates and then longer term extrapolations, Free Cash Flow is projected to reach roughly $4.52 billion by 2035, with most of the growth front loaded into the next decade before it gradually slows.

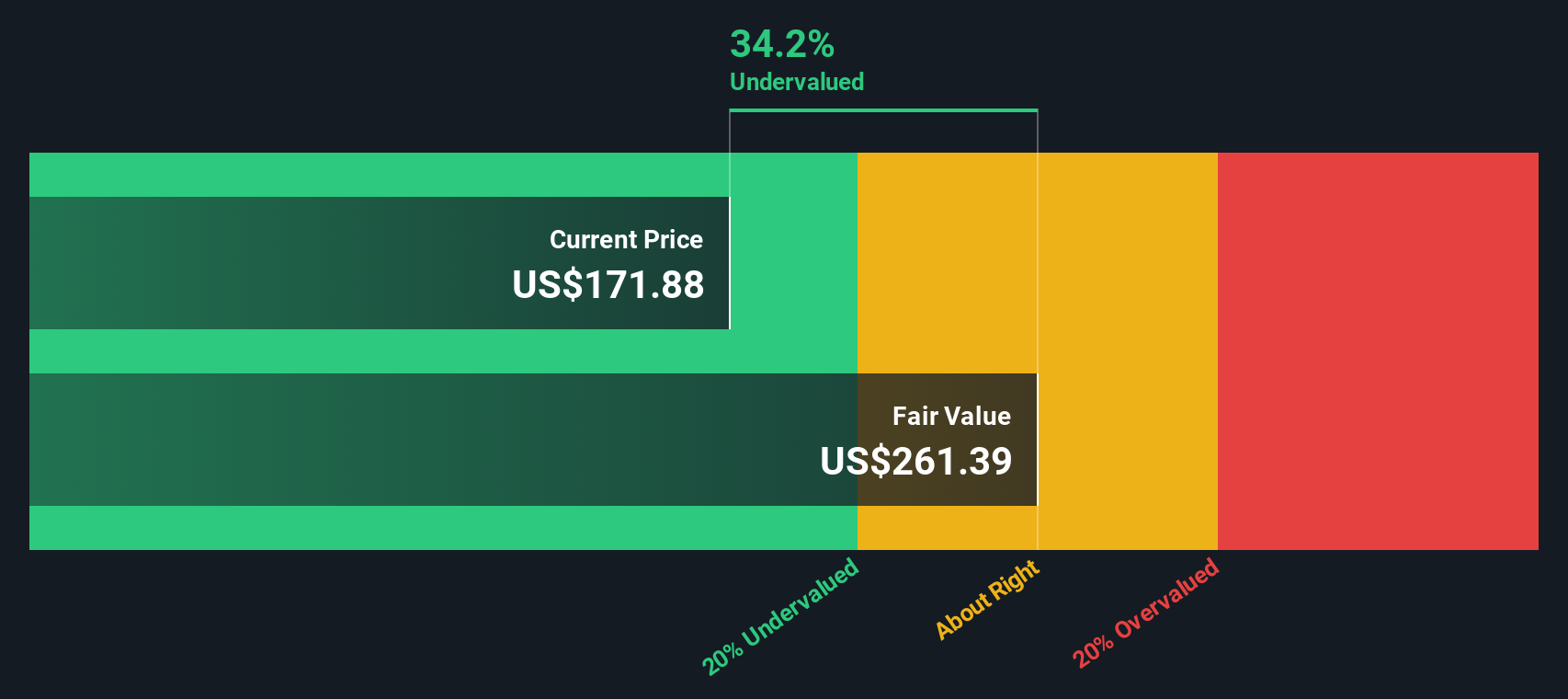

Using these cash flow projections in a 2 Stage Free Cash Flow to Equity model, the intrinsic value for Atlassian is estimated at about $248.95 per share. With the DCF indicating the stock trades at roughly a 37.0% discount to this fair value, the model suggests the market is pricing Atlassian well below its long term cash generation potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Atlassian is undervalued by 37.0%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

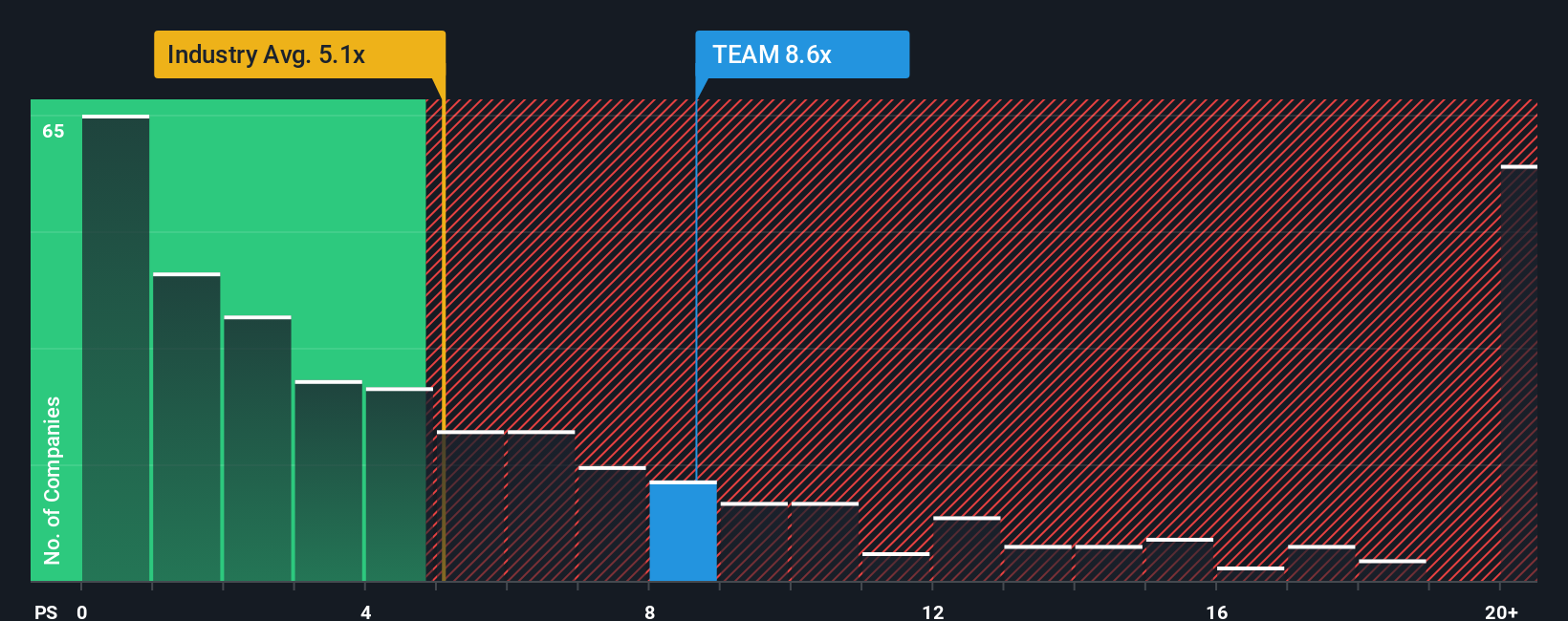

Approach 2: Atlassian Price vs Sales

For a fast growing software business like Atlassian that is still reinvesting heavily, the Price to Sales ratio is a useful way to compare valuation because it focuses on revenue rather than current accounting profits, which can be noisy.

In general, investors are willing to pay a higher sales multiple for companies with stronger growth prospects and lower perceived risk, while slower or riskier businesses usually warrant a lower, more conservative multiple. So a “normal” or “fair” Price to Sales ratio should reflect both how quickly the top line is expanding and how dependable that growth looks.

Atlassian currently trades on a Price to Sales multiple of about 7.55x. This is above the broader Software industry average of 4.91x but below the peer group average of 12.58x. Simply Wall St’s proprietary Fair Ratio for Atlassian is 12.43x, which estimates the multiple the stock should trade on given its specific growth outlook, margins, scale, industry and risk profile. This can be more informative than a simple peer or industry comparison because it adjusts for Atlassian’s own fundamentals rather than assuming all software names deserve the same multiple. With the current 7.55x well below the 12.43x Fair Ratio, the shares appear attractively priced on a sales basis.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Atlassian Narrative

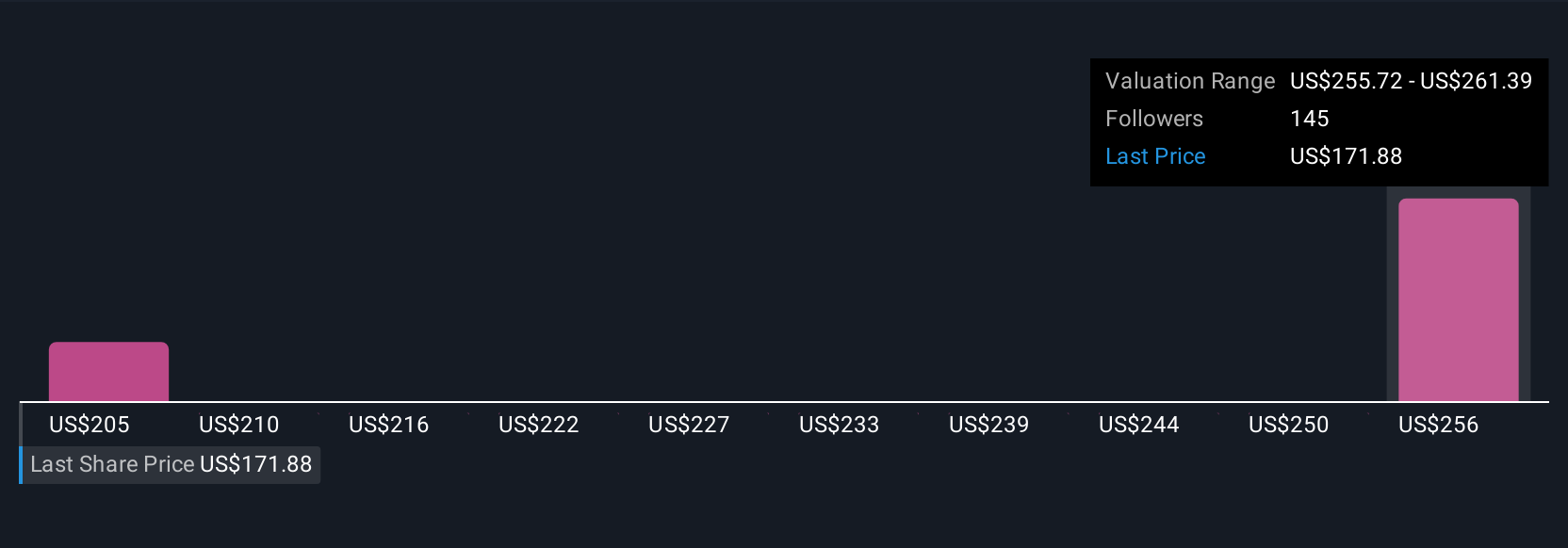

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Atlassian’s story with the numbers by turning your assumptions about its future revenue, earnings, and margins into a forecast and then into a Fair Value that you can easily compare to the current share price.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors to do exactly this. They help you decide whether to buy, hold, or sell by showing in real time whether your Fair Value sits above or below today’s price, and they automatically update that view when fresh information such as earnings, guidance, or major news hits the market.

For example, one Atlassian Narrative on the platform might assume a Fair Value near $200 per share with mid teens growth and healthy margins. Another, more optimistic Narrative could see Fair Value closer to $245 per share with faster growth and richer profitability. This clearly illustrates how different but reasonable perspectives on the same company can lead to very different conclusions about whether the current price looks attractive or stretched.

Do you think there's more to the story for Atlassian? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TEAM

Atlassian

Provides a collaboration software that enables organizations to connect all teams through a system of work that unlocks productivity at scale worldwide.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

42 followersusers have followed this narrative

6 commentsusers have commented on this narrative

14 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative