Advertisement

- United States

- /

- Software

- /

- NasdaqGS:SNPS

Is It Too Late To Consider Synopsys (SNPS) After Recent Share Price Pullback?

Reviewed by Bailey Pemberton

- Wondering if Synopsys at around US$475 a share still offers value, or if the easy money has already been made? This article focuses squarely on what the current price might imply.

- The stock has been choppy recently, with the share price down 9.4% over the past week, 1.2% over the past month, and 1.0% year to date, while the 1 year return sits at 2.5% and the 5 year return at 85.9%.

- Recent coverage of Synopsys has centered on its role in software for chip design and automation tools, along with broader interest in companies connected to semiconductors and AI related workflows. This attention helps explain why the stock has been on many investors' watchlists even as short term returns have cooled.

- Despite that interest, Synopsys currently records a valuation score of 0 out of 6. The next sections will compare what different valuation methods suggest about the current price and then finish with a way to put those numbers in a broader context.

Synopsys scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Synopsys Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates what a stock might be worth by projecting the company’s future cash flows and then discounting those back to today’s value using a required rate of return.

For Synopsys, the 2 Stage Free Cash Flow to Equity model starts with last twelve months free cash flow of about $2.59b. Analyst inputs and extended projections suggest free cash flow reaching $4.93b by 2030, with interim years between 2026 and 2035 ranging from roughly $2.00b to $7.26b before discounting. Simply Wall St only uses direct analyst estimates where they are available and extrapolates further years based on the model’s assumptions.

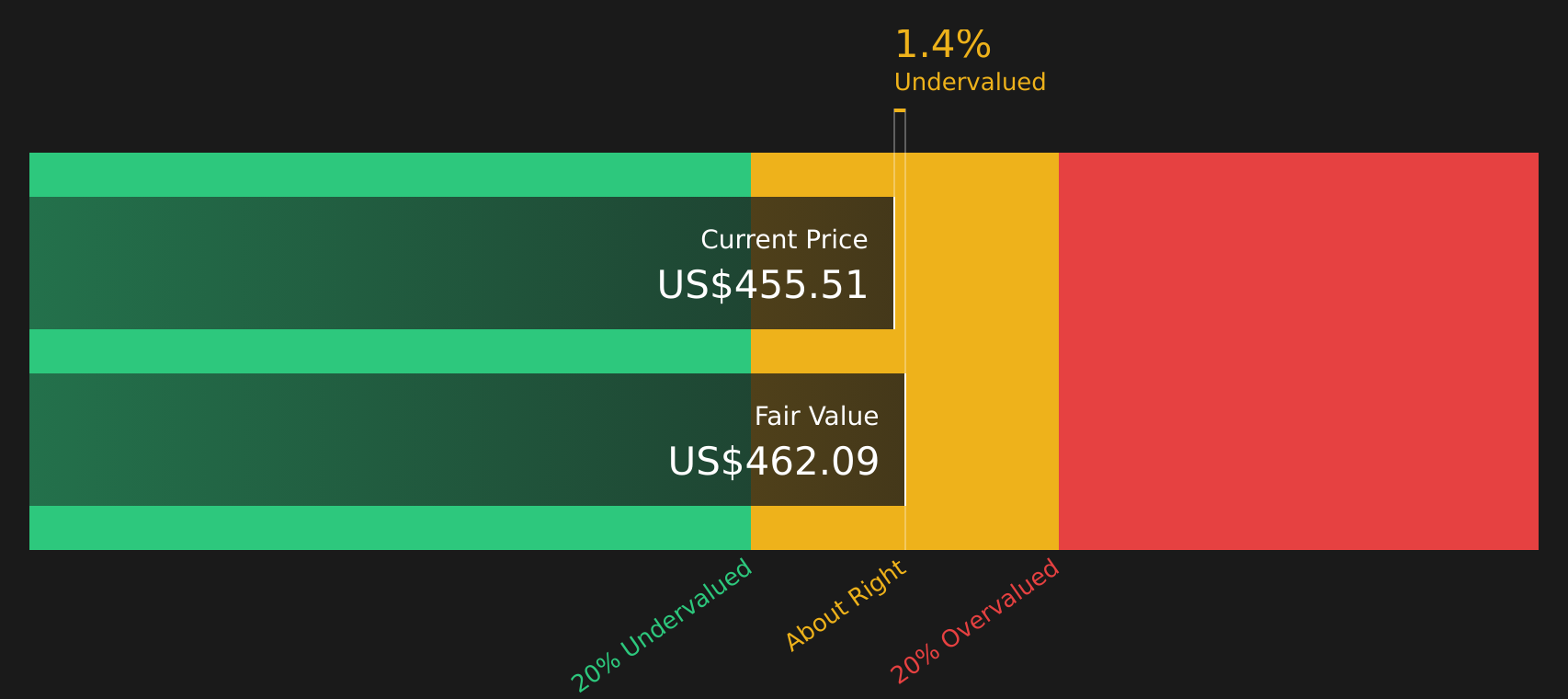

After discounting these projected cash flows back to today, the model arrives at an estimated intrinsic value of about $469.73 per share. With the current share price around $475, the DCF implies the stock is roughly 1.3% above this estimate, which is a very small gap and well within the sort of margin where reasonable assumptions can differ.

Result: ABOUT RIGHT

Synopsys is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Synopsys Price vs Earnings

For profitable companies, the P/E ratio is a useful way to think about what you are paying for each dollar of current earnings. It rolls expectations about growth and risk into a single number, since investors are usually willing to pay a higher multiple for companies where they expect stronger earnings growth or see less risk, and a lower multiple where the outlook is more uncertain.

Synopsys currently trades on a P/E of about 117.8x. That compares with an average of about 29.3x for the broader Software industry and a peer group average of about 35.5x, so the stock is on a much higher multiple than these simple benchmarks.

Simply Wall St’s Fair Ratio metric estimates what a more tailored P/E might look like once factors such as earnings growth, profit margins, industry, market cap and risk profile are considered together. This is more specific than just lining Synopsys up against industry or peer averages, because it tries to adjust for the company’s own characteristics rather than assuming all software stocks should trade on similar multiples. For Synopsys, the Fair Ratio is 51.7x, which is well below the current P/E of 117.8x. This suggests the shares are pricing in more than this framework would typically support.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Synopsys Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so on Simply Wall St’s Community page you can use Narratives, which are clear stories that link your view of Synopsys’ business to a forecast for revenue, earnings and margins, then to a Fair Value that you can compare with the current price to help decide whether to buy, hold or sell. Each Narrative updates as fresh news or earnings arrive, and different investors sometimes land far apart. For example, some see Synopsys closer to the higher analyst fair value area around US$650 because they focus on integration of Ansys, SaaS and AI driven tools. Others are more cautious and anchor closer to the lower end around US$403.85 because they emphasise China exposure, execution risks and IP segment uncertainty.

Do you think there's more to the story for Synopsys? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SNPS

Synopsys

Provides design IP solutions in the semiconductor and electronics industries.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.563.5% undervalued

49 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.826.3% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23055.3% overvalued

53 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

LI

Lijo on Accenture ·

A value stock that's undervalued.

Fair Value:US$18326.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Rox Resources ·

Developer to Producer: Debt-Free Path, A$965M Post-Tax NPV, and Massive Gold Leverage

Fair Value:AU$6.1693.3% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

JO

John_Eric on MercadoLibre ·

MercadoLibre and the Spreadsheet Trick That Decides Everything

Fair Value:US$4.72k60.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.8% undervalued

86 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5448.2% undervalued

60 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7107.2% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative