Advertisement

- United States

- /

- IT

- /

- NasdaqGS:RXT

Rackspace Technology (RXT) Recasts Its AI Focus, Is Future Growth Already Priced In?

Rackspace Technology (RXT) is in the spotlight after approving a workforce realignment that affects about 15% of staff and signing a definitive AI compute deployment agreement with Advanced Micro Devices, Inc. This signals a clear shift toward governed enterprise AI.

See our latest analysis for Rackspace Technology.

Those workforce cuts and the long term AI compute buildout with AMD arrive after a very large year to date share price return and a similarly strong 1 year total shareholder return. However, the 5 year total shareholder return, which is down sharply, shows how quickly sentiment around Rackspace Technology has shifted.

If you are tracking how enterprise AI stories are reshaping opportunities, it can be helpful to see what else is moving in this space through our curated list of 49 AI infrastructure stocks

Rackspace Technology now trades at $6.82 after a very large recent move, yet analysts see the stock below their $4.90 price target and the company is still reporting losses. Is there a genuine opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 215% Overvalued

The most widely followed narrative puts Rackspace Technology's fair value at $2.17 a share, far below the recent $6.82 close, which creates a wide gap between market price and modeled value.

Ongoing digital transformation and increasing complexity of hybrid/multi-cloud environments are driving strong demand for Rackspace's managed cloud services, as evidenced by double-digit year-over-year bookings growth and a shift toward larger, longer-term enterprise contracts; this is likely to support a sustained rebound in revenue and enhance revenue visibility.

Want to see what sits behind that fair value call? The narrative leans heavily on modest top line growth, improving margins, and a low implied future earnings multiple. Curious how those moving parts combine into one number.

Result: Fair Value of $2.17 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, Rackspace Technology still faces pressure from declining Public and Private Cloud revenues and ongoing losses of about US$146.0 million, which could challenge this fair value narrative.

Find out about the key risks to this Rackspace Technology narrative.

Another View on Rackspace Technology's Valuation

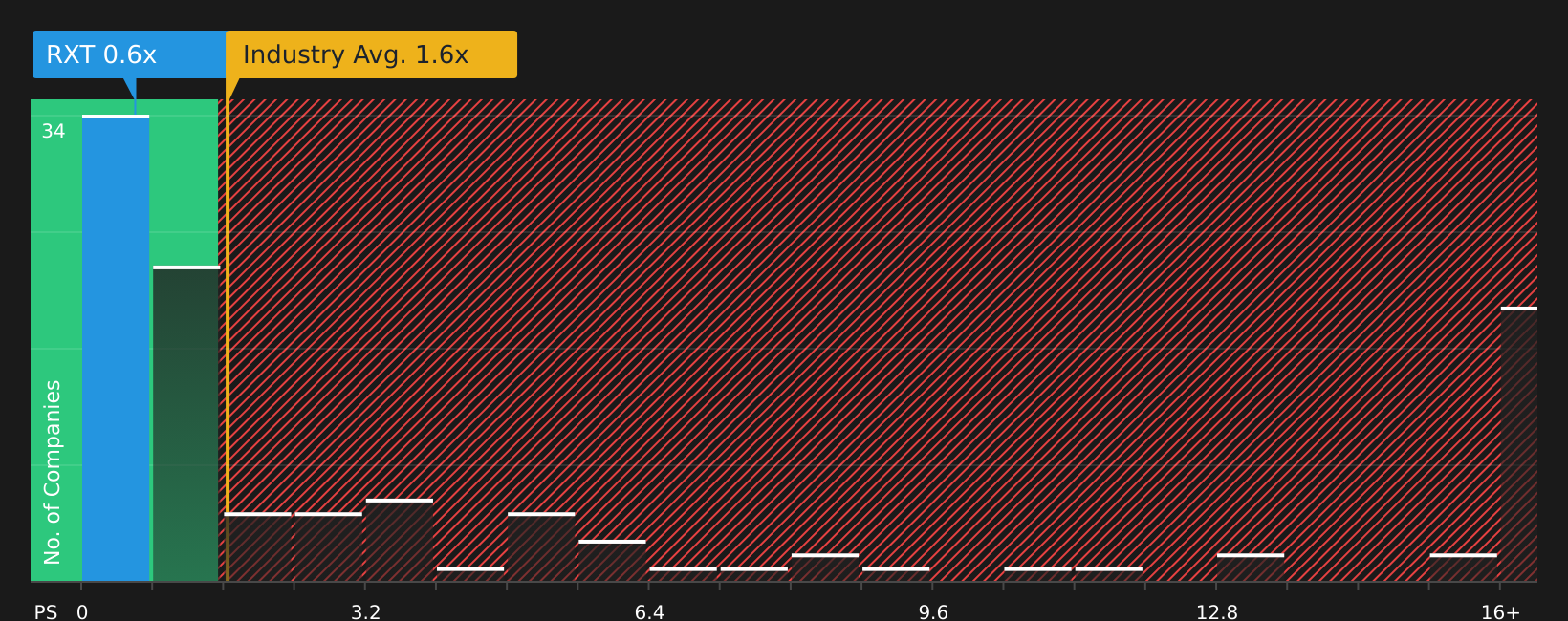

The narrative around Rackspace Technology leans heavily on a fair value of $2.17 per share based on future earnings assumptions, yet current trading implies a very different story. On a simple P/S basis of 0.6x, the stock sits well below the estimated fair ratio of 1.3x, the US IT industry average of 1.7x and a peer average of 14.6x, which points to a wide gap between sentiment and sales based valuation. Is the discount reflecting real balance sheet and profitability risks, or could it be overshooting?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Seeing mixed sentiment around Rackspace Technology's valuation and outlook? Take a closer look at the detail, weigh the concerns and potential upside, and review the 1 key reward and 4 important warning signs

Looking for more investment ideas beyond Rackspace Technology?

If Rackspace Technology has your attention, do not stop here. Fresh ideas across quality, income, and stability could sharpen your next move.

- Target potential mispriced opportunities by scanning a curated set of 44 high quality undervalued stocks that pair solid business profiles with compressed valuations.

- Strengthen the income side of your portfolio by reviewing 7 dividend fortresses that focus on higher yields with an emphasis on resilience.

- Prioritize capital preservation and steadier compounding by examining 69 resilient stocks with low risk scores designed to highlight companies with lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:RXT

Rackspace Technology

Operates as a hybrid cloud and artificial intelligence solutions company in the United States, the United Kingdom, and internationally.

Slight risk and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.558.3% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.1% undervalued

57 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.2% undervalued

61 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.3% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$1.315.1k% overvalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.885.3% undervalued

89 followersusers have followed this narrative

7 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

RockeTeller on Montage Gold ·

Montage Gold, Building West Africa’s Next 300Koz Producer, First Pour Late 2026, 5.88Moz Resource

Fair Value:CA$23.538.3% undervalued

18 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17060.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative