Advertisement

- United States

- /

- Software

- /

- NasdaqGS:RDWR

Radware (RDWR) Valuation Check After Launch Of New API Security Service

Radware’s New API Security Service and Why It Matters for RDWR Stock

Radware (RDWR) has launched its Radware API Security Service, an end to end offering that uses real time production traffic to help protect APIs throughout their lifecycle and address OWASP Top 10 API risks.

See our latest analysis for Radware.

At a share price of $24.66, Radware has seen a 1 day share price return of 1.02% and a year to date share price return of 3.70%. Its 1 year total shareholder return of 12.04% and 3 year total shareholder return of 15.99% suggest moderate momentum over a longer horizon, despite a weaker 90 day share price return of a 5.70% decline and a 5 year total shareholder return of a 13.02% decline.

If this kind of cybersecurity product launch has your attention, it could be a good moment to scan other tech names using our high growth tech and AI stocks.

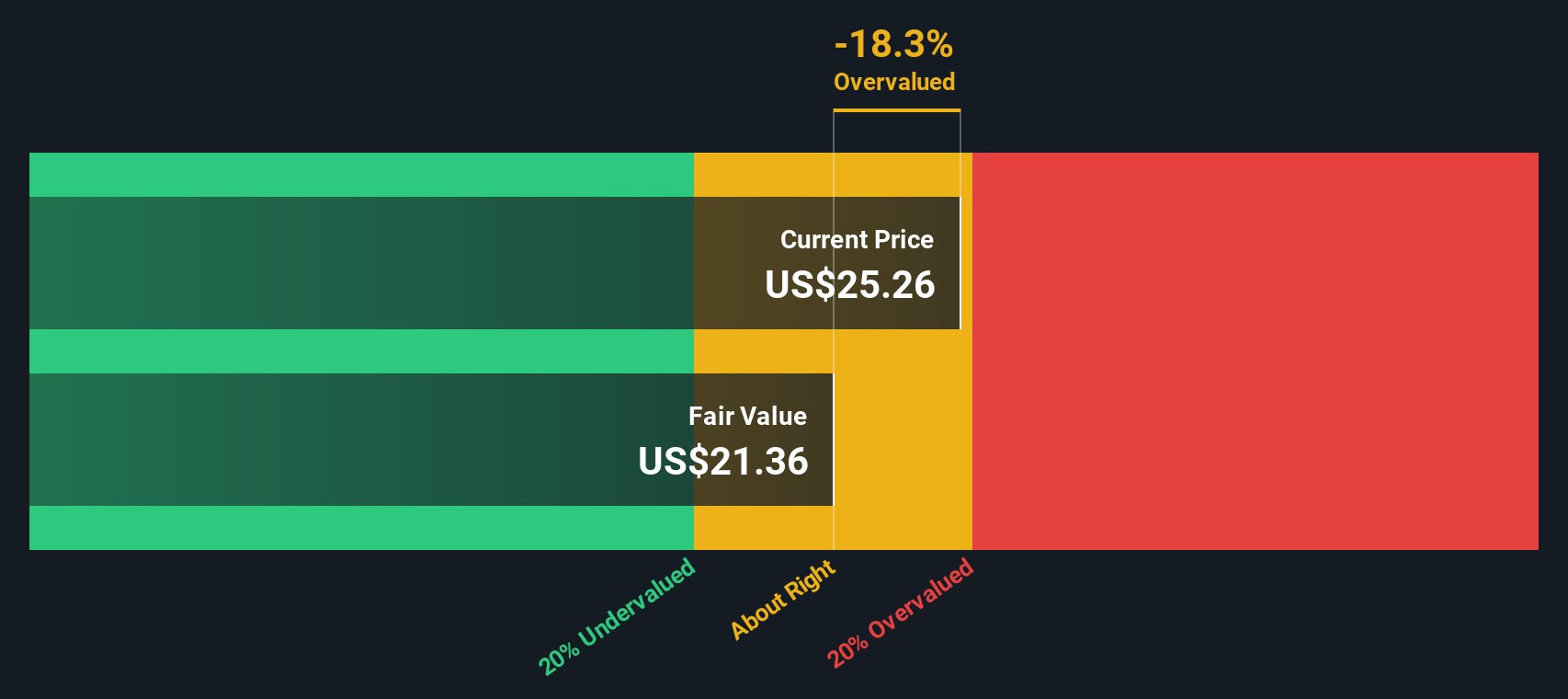

With Radware trading at $24.66 and sitting about 24% below the average analyst price target of $30.67, you have to ask yourself: is this a genuine mispricing, or is the market already factoring in future growth?

Price to Earnings of 64.3x: Is It Justified?

On a P/E of 64.3x at a last close of $24.66, Radware looks expensive compared to both its software peers and the broader US software sector.

The P/E multiple compares the current share price with earnings per share, so a higher ratio usually means investors are paying more for each dollar of profit. For a cybersecurity and application delivery business like Radware, a rich multiple can sometimes signal that the market is pricing in stronger profit growth or a higher quality earnings stream, but here the picture is mixed.

Radware has only recently moved into profitability, helped by a one off gain of $5.8m in the last twelve months. Earnings have declined by 20.6% per year over the past five years and Return on Equity sits at a low 4.3%. Against that backdrop, a 64.3x P/E suggests the market is paying a premium relative to the company’s historical earnings profile.

Compared with the US Software industry average P/E of 30.8x and a peer average of 28.8x, Radware’s 64.3x multiple is more than double those reference points. This is a wide gap for investors to weigh. See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 64.3x (OVERVALUED)

However, you still have to weigh risks such as earnings pressure if the one off gain fades, and the possibility that the high P/E leaves little margin for disappointment.

Find out about the key risks to this Radware narrative.

Another View: Our DCF Model Points Lower

If you set the P/E aside and look at our DCF model, the story shifts. Radware at $24.66 is trading above our future cash flow value estimate of $17.38. This suggests the shares screen as overvalued on this approach as well. So which signal do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Radware for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 872 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Radware Narrative

If you see the numbers differently, or prefer to test your own assumptions against the data, you can build a tailored thesis in just a few minutes, starting with Do it your way.

A great starting point for your Radware research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready to find your next idea?

If Radware has you thinking more broadly about opportunities, do not stop here. Widen your search now or you could miss something that fits you better.

- Spot potential value pockets by checking out these 872 undervalued stocks based on cash flows that may offer more attractive prices relative to their cash flows.

- Tap into growth themes by scanning these 23 AI penny stocks that sit at the intersection of technology and artificial intelligence.

- Hunt for income ideas by reviewing these 13 dividend stocks with yields > 3% that provide yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:RDWR

Radware

Develops, manufactures, and markets cyber security and application delivery solutions for cloud, on-premises, and software defined data centers.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2550.7% undervalued

113 followersusers have followed this narrative

0 commentsusers have commented on this narrative

25 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4846.5% undervalued

216 followersusers have followed this narrative

8 commentsusers have commented on this narrative

33 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43043.8% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9954.9% undervalued

28 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

TR

TripleS on Dong A Eltek ·

Dong-A Eltek (088130 on the KOSDAQ) trades at ₩4,325 and owns about ₩17,780 per share of assets

Fair Value:₩6.31k31.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_6nroa on Charter Communications ·

Charter is undervalued - Here's why.

Fair Value:US$28049.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$1.8828.2% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28030.3% undervalued

216 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.917.4% overvalued

99 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6511.3% undervalued

74 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

1

|0

BL

Blegells on Terra Balcanica Resources ·

⏫42X THE AVERAGE DAILY TRADING VOLUME TODAY, JULY 28 🐂🐂🐂 FORTY-TWO!

1

|0