- United States

- /

- IT

- /

- NasdaqGS:KC

When Will Kingsoft Cloud Holdings Limited (NASDAQ:KC) Become Profitable?

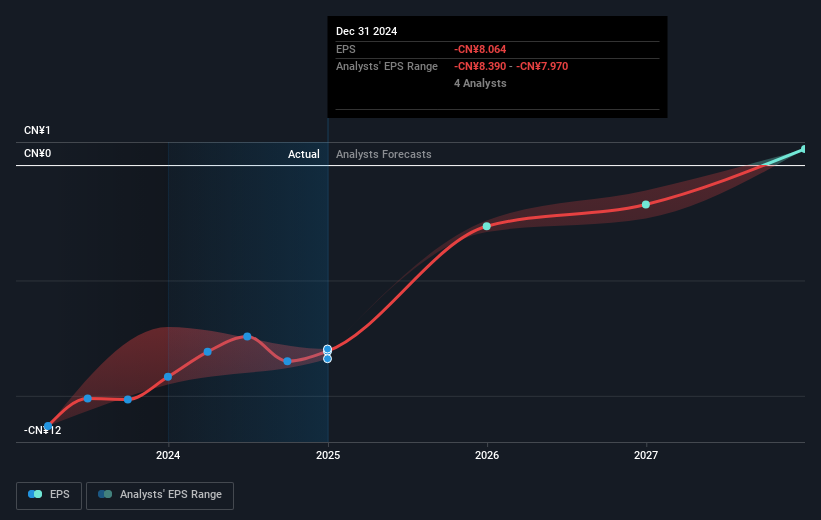

Kingsoft Cloud Holdings Limited (NASDAQ:KC) is possibly approaching a major achievement in its business, so we would like to shine some light on the company. Kingsoft Cloud Holdings Limited provides cloud services to businesses and organizations primarily in China. The US$3.6b market-cap company announced a latest loss of CN¥2.0b on 31 December 2024 for its most recent financial year result. As path to profitability is the topic on Kingsoft Cloud Holdings' investors mind, we've decided to gauge market sentiment. In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

Consensus from 13 of the American IT analysts is that Kingsoft Cloud Holdings is on the verge of breakeven. They expect the company to post a final loss in 2026, before turning a profit of CN¥523m in 2027. Therefore, the company is expected to breakeven roughly 2 years from today. How fast will the company have to grow each year in order to reach the breakeven point by 2027? Working backwards from analyst estimates, it turns out that they expect the company to grow 95% year-on-year, on average, which is extremely buoyant. If this rate turns out to be too aggressive, the company may become profitable much later than analysts predict.

Underlying developments driving Kingsoft Cloud Holdings' growth isn’t the focus of this broad overview, however, take into account that by and large a high forecast growth rate is not unusual for a company that is currently undergoing an investment period.

Check out our latest analysis for Kingsoft Cloud Holdings

Before we wrap up, there’s one issue worth mentioning. Kingsoft Cloud Holdings currently has a debt-to-equity ratio of 105%. Generally, the rule of thumb is debt shouldn’t exceed 40% of your equity, which in this case, the company has significantly overshot. A higher level of debt requires more stringent capital management which increases the risk in investing in the loss-making company.

Next Steps:

There are key fundamentals of Kingsoft Cloud Holdings which are not covered in this article, but we must stress again that this is merely a basic overview. For a more comprehensive look at Kingsoft Cloud Holdings, take a look at Kingsoft Cloud Holdings' company page on Simply Wall St. We've also put together a list of pertinent factors you should further examine:

- Valuation: What is Kingsoft Cloud Holdings worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Kingsoft Cloud Holdings is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Kingsoft Cloud Holdings’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you're looking to trade Kingsoft Cloud Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kingsoft Cloud Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:KC

Kingsoft Cloud Holdings

Provides cloud services to businesses and organizations primarily in China.

Reasonable growth potential with mediocre balance sheet.

Market Insights

Community Narratives