Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

The Bull Case For InterDigital (IDCC) Could Change Following New Amazon License And Arbitration Deal - Learn Why

Reviewed by Sasha Jovanovic

- InterDigital, Inc. recently entered into a patent license agreement with Amazon covering its services and devices, including Amazon Prime Video, while both parties agreed to resolve all pending litigation and move to binding arbitration to finalize the agreement terms.

- At the same time, shareholders approved bylaw changes to add officer exculpation and the Board reaffirmed a US$0.70 quarterly dividend, underscoring the company’s focus on legal risk management and ongoing cash returns to investors.

- Next, we’ll examine how the Amazon licensing deal and dispute resolution could reshape InterDigital’s investment narrative and perceived earnings resilience.

Explore 30 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

InterDigital Investment Narrative Recap

To own InterDigital, you need to believe its patent portfolio can keep converting global device and service usage into durable, high margin licensing revenue. The Amazon agreement, with litigation moving into binding arbitration, directly affects that core earnings engine in the near term, while the largest present risk remains how legal outcomes and regulatory shifts could alter the profitability and predictability of those licensing streams.

Among the recent announcements, the patent license deal with Amazon is most closely tied to near term catalysts. It reinforces InterDigital’s push beyond smartphones into services and consumer electronics, an area analysts already highlight as a key growth driver. At the same time, resolving disputes through arbitration instead of protracted court battles intersects with concerns about legal costs and the reliability of one off catch up payments as a recurring earnings pillar.

Yet behind the Amazon headlines, investors should also be aware of how rising legal and regulatory scrutiny could eventually reshape InterDigital’s ability to…

Read the full narrative on InterDigital (it's free!)

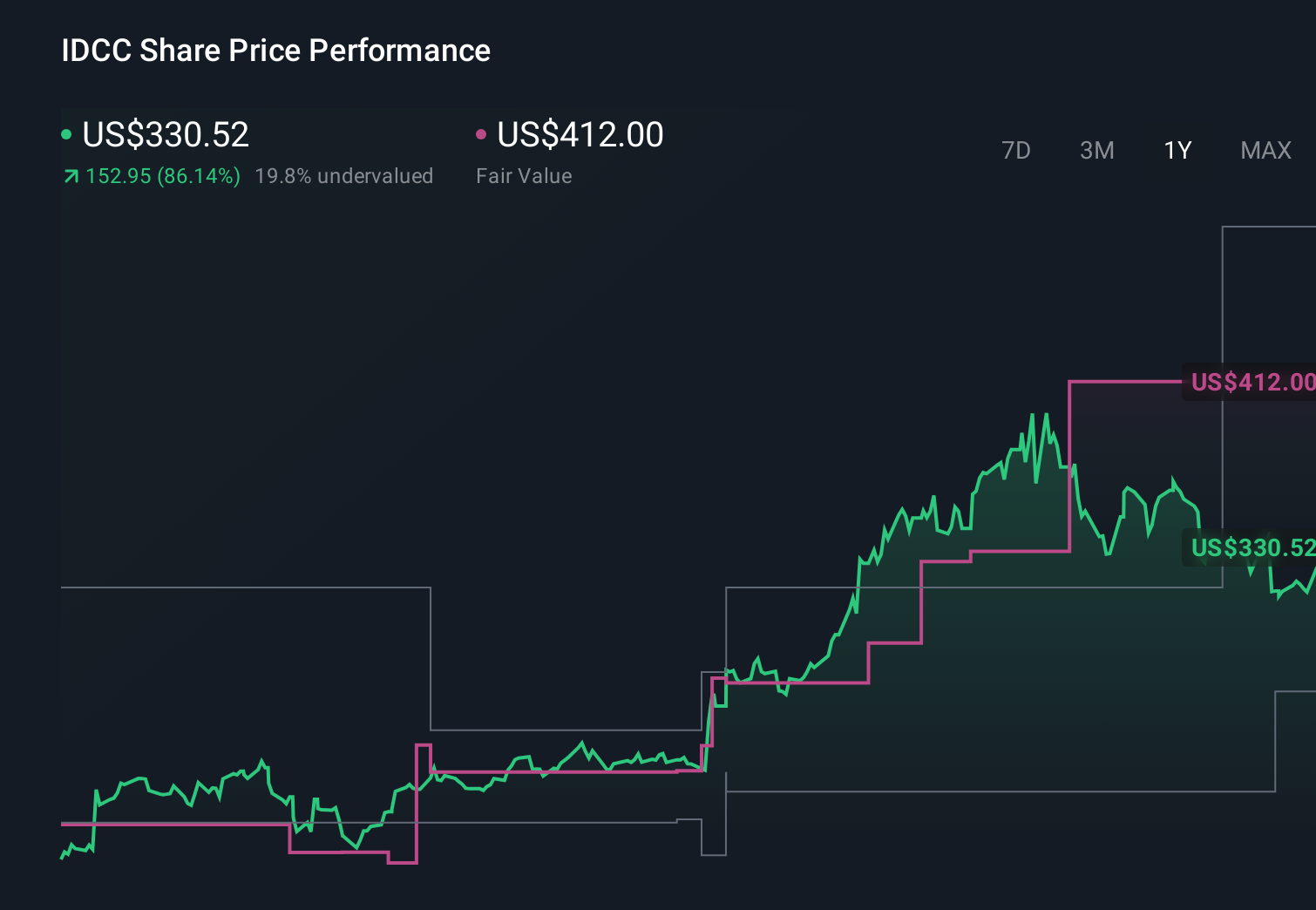

InterDigital's narrative projects $824.6 million revenue and $350.8 million earnings by 2029.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 66% upside to its current price.

Exploring Other Perspectives

Compared with consensus, the most cautious analysts already flagged rising legal costs as a core risk, even while assuming revenues of about US$1.0 billion and earnings of roughly US$505 million by 2029, so you should expect that this Amazon development could push some of those views to evolve in very different directions.

Explore 5 other fair value estimates on InterDigital - why the stock might be worth less than half the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Contemplating Other Strategies?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 38 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3458.4% undervalued

53 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.9% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.9% undervalued

44 followersusers have followed this narrative

1 commentusers have commented on this narrative

26 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2782.0% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0336.2% undervalued

2 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

DE

Delphic on NuScale Power ·

NuScale is Postioned For Long-Term Growth

Fair Value:US$10089.1% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

Treasury_Raccoon_w0gg on Walmart ·

Walmart's 'Other' Segment Will Power New Growth Beyond Retail

Fair Value:US$154.5822.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.6% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.3% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17057.1% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative